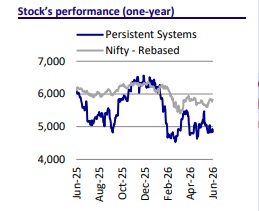

Buy Persistent Systems Ltd for the Target Rs 6,200 by Motilal Oswal Financial Services Ltd

Persistent acquires Nagarro Geographical mix improves; margin delivery to be watched

* Persistent Systems announced two strategic developments:

(1) The acquisition of Nagarro for an enterprise value of €1.27b

(2) A new USD650m+ services contract over 6.5 years with an existing US-based technology customer. Nagarro adds ~USD1.1b revenue, taking the combined entity to nearly USD2.9b revenue with ~46,000 employees across 40+ countries, while strengthening Persistent's presence in Europe and broadening its service portfolio. Separately, the large customer deal is entirely incremental (not a renewal), is expected to contribute ~USD125m annually, and begins ramping from 2QFY27.

* Transaction details: Persistent will acquire 100% of Nagarro through an all-cash offer of €81/share, implying an enterprise value of €1.27b (140% premium to the undisturbed share price and 94% premium to the three-month VWAP). The company has already secured a 21% stake, with Nagarro's management also intending to tender its shares.

* As seen in Exhibit 2, the offer requires a minimum acceptance of 50% plus one share and is expected to close in 4QCY26/early 1QCY27, subject to regulatory approvals. The acquisition will be funded through a €1.4b committed bridge facility from Barclays (~4.1-4.8% borrowing cost), with no equity dilution or QIP. Management expects the deal to be cash EPS accretive from Year 1, while reported EPS should also remain accretive, excluding one-time transaction costs.

* We view this acquisition as addressing Persistent's long-standing objective of building scale in Europe, broadening its vertical mix, and creating cross-sell opportunities with limited customer overlap. The acquisition also appears priced at 9.1x EV/EBITDA, which we believe is a reasonable valuation for a business of Nagarro’s scale. However, it remains to be seen how much value Persistent can extract from the acquisition through integration and crossselling. We are relatively more cautious on the addition of ERP, a more mature and competitive service line than Persistent's core digital engineering business. While management expects margins to remain broadly stable, we would await greater clarity on integration, cost synergies, and the path toward margin convergence, given Nagarro's lower profitability. Execution over the next few quarters will remain the key monitorable.

Vertical expansion a positive; the service mix becomes broader

* The acquisition significantly broadens Persistent's industry mix. While Persistent has built strong positions in Technology, BFSI, and Healthcare, Nagarro brings meaningful exposure to Industrials, Consumer, and the Public Sector, particularly across Europe (refer to Exhibit 1).

* The deal also opens access to government and regulated-sector opportunities where Persistent previously had limited presence.

* Nagarro also strengthens Persistent's capabilities across ERP (particularly SAP), consulting, and customer experience (CX), while adding a stronger presence in manufacturing-led engineering.

* However, we are relatively more cautious on the service-line mix. Persistent has historically differentiated itself through digital engineering and cloud-led services, while ERP is a larger, relatively mature, and more competitive market. We believe execution and differentiation in this segment will be important monitorables over the medium term.

Margins remain an area where we await greater clarity

* Management indicated that the combined entity should not operate at notably lower margins than Persistent today and expects the transaction to be EPS accretive from the first year. While cost synergies exist, management indicated that a meaningful portion will be reinvested into future growth initiatives.

* That said, we believe margins remain an important area to watch. Nagarro reported an EBIT margin of ~10.9% in CY25 and 12.1% in 1QCY26, compared with Persistent's 15.6% FY26 EBIT margin and 16.3% in 4QFY26.

* While management expects operational improvements and does not foresee material margin dilution over time, we would await greater clarity on the pace of integration, achievable cost synergies, and the timeline for margin convergence before building these into our assumptions.

Valuation and view

* Strategically, we view this acquisition as addressing Persistent's long-standing objective of building scale in Europe, meaningfully broadening its vertical exposure, and strengthening its positioning for larger global transformation programs.

* The limited customer overlap and complementary geographic presence also create a reasonable cross-sell opportunity.

* Our area of caution is around the services mix and margins. While ERP strengthens Persistent's end-to-end portfolio, it also increases exposure to a relatively mature and competitive services segment where differentiation can be harder than in digital engineering.

* Similarly, although management has guided stable margins and Year-1 EPS accretion, Nagarro currently operates at a lower margin profile. We therefore think integration execution, realization of cost synergies, margin improvement, and leadership retention will remain the key monitorables over the next few quarters. We continue to value the stock at 34x FY28E EPS and reiterate our BUY rating with a TP of INR6,200

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

-96767.jpg)

2.jpg)