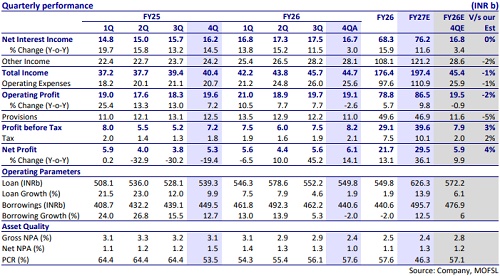

Neutral SBI Cards Ltd for the Target Rs.760 by Motilal Oswal Financial Services Ltd

In-line quarter; credit cost improves further

NIMs expand 10bp QoQ

* SBI Cards (SBICARD) reported 4QFY26 PAT of INR6.09b (up 14% YoY/9% QoQ), amid lower-than-expected provisions.

* NIMs expanded 10bp QoQ to 11.1%, as lower CoF was partly offset by a moderate decline in yields. Management expects margins to remain broadly stable going ahead.

* Opex grew 23.5% YoY/down 1.4% QoQ to INR25.6b. The bank has reversed INR1.1b owing to the PIDF reversal.

* Credit cost improved to 7.7% (vs 8.3% in 3QFY26). Management overlay was increased to INR2.20b for prudence.

* Spends growth was weak at 31% YoY/1% QoQ, led by strong corporate spends (up 195% YoY/12% QoQ). Retail spends rose 13% YoY (down 2% QoQ). Corporate spends contributed ~22% of total spends.

* GNPA ratio improved 45bp QoQ to 2.41%, while NNPA ratio declined 24bp QoQ to 1.04%. ECL declined 30bp QoQ to 3.0%, while PCR improved 154bp QoQ to 57.6%.

* We maintain our earnings and estimate SBICARD to report an RoA/RoE of 4.15%/17.3% by FY27. Reiterate Neutral with a revised TP of INR760 (22x Sep’27E EPS).

Loan growth muted; revolver mix declines to 22%

* 4Q PAT grew 14% YoY/9% QoQ to INR6.09b (4% beat), aided by steady NII growth and lower-than-expected credit cost.

* NII grew 3% YoY/declined 5% QoQ to INR16.7b (largely in line). NIMs expanded 10bp QoQ to 11.1%, supported by lower CoF, partly offset by a moderation in yields. Management expects NIMs to remain broadly stable going forward.

* The transactor mix increased to 46% (vs 44% in 3QFY26), while revolve mix moderated to 22% (vs 23% in 3QFY26). The EMI mix declined to 32% (vs 34% in 3QFY26), reflecting a seasonal run-off of festival tenor balances.

* Other income grew 60% YoY/11.7% QoQ (19% beat on MOFSLe), aided by a one-off GST liability reversal of INR765.7m. C/I ratio increased modestly to 57.2% vs 56.8% in 3QFY26.

* CIF grew 6% YoY/1% QoQ to 22.1m. New card sourcing stood at 917k, within the guided 0.9-1.0m run rate. Around 54% of sourcing came from open market in 4QFY26.

* Spends remained strong with 31% YoY/1% QoQ growth, led by continued traction in corporate spends (up 195% YoY/12% QoQ), while retail spends grew 13% YoY. Despite healthy spends, receivables remained flat QoQ at INR569.3b due to a higher transactor mix and lower revolve balances.

* GNPA ratio improved 45bp QoQ to 2.41%, while NNPA ratio declined 24bp QoQ to 1.04%. ECL declined 30bp QoQ to 3.0%, while PCR improved 154bp QoQ to 57.6%.

Highlights from the management commentary

* Management overlay increased to INR2.2b as of Mar’26 from INR1.21b in Dec’25, reflecting prudence amid geopolitical uncertainty and ECL model refresh.

* Management expects NIMs to remain broadly stable in FY27, though any significant rise in CoF could pose a risk.

* Revolver mix has remained in the 22-24% band over two years and may trend slightly lower as newer vintages show lower revolving behavior.

* Card acquisition guidance remains 0.9-1.0m accounts per quarter.

* Management reiterated a medium-term RoA target of 4-4.5%, with lower credit costs being the key driver.

* Management expects further moderation in credit cost during FY27, though the pace will depend on macro and geopolitical developments.

Valuation and view

SBICARD reported a largely in line but subdued performance in 4Q, with lower provisions and an improving credit cost outlook, even as receivables declined due to a higher share of transactors. Credit cost moderated to 7.7%, despite the bank taking an additional management overlay of INR1b during the quarter. NIMs are expected to remain broadly stable, as the benefit of lower cost of funds is likely to be partly offset by some moderation in yields. Corporate spending has rebounded, leading to a slight uptick in operating expenses, with corporate share expected to remain ~20% of the overall mix. Asset quality is expected to improve going forward, supported by lower forward delinquencies and a favorable macroeconomic environment. We maintain our earnings and estimate SBICARD to report an RoA/RoE of 4.15%/17.3% by FY27. Reiterate Neutral with a revised TP of INR760 (22x Sep’27E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412