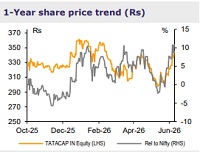

Add Tata Capital Ltd for the Target Rs 390 by Emkay Global Financial Services Ltd

We met Tata Capital’s senior management, including the MD, on 18-Jun, for updates on current developments and the business outlook. Key takeaways: 1) The management reiterated its FY28 guidance of 23-25% AUM CAGR, credit cost of ~1%, and RoA of 2.5-2.7%. 2) Business trends are stable despite the macro uncertainty, though the management remains watchful in select MSME and CV segments. 3) Incremental cost of funds is higher versus Mar-26, but is expected to uphold or moderate ahead. 4) Growth of the new-product and high-yield segments, including gold loans, is expected to gather pace. With FY28 guidance unchanged across key parameters and execution supporting confidence in the earnings trajectory, we maintain ADD with unchanged Mar-27E TP of Rs390, implying FY28E PBV of ~2.6x.

Tata Cap maintains focus on growth while staying vigilant amid uncertainties

The management maintains its FY25-28 guidance of 23-25% AUM growth, while indicating it remains cautious in some segments of MSME and CV financing amid the ongoing uncertainties. It indicated that growth will be focused more toward high-yield segments like Affordable and Micro HL/LAP, Gold loan, PL/BL, and MFI. Also, the growth will be supported by branch expansion, entry into newer/deeper geographies and increasing the product offerings in existing branches. The company reiterated its focus on the middle-income segment and highlighted that it had earlier exited businesses such as consumer durable, tractor, and farm loans due to risk and profitability considerations. It also emphasized that the motor finance book, which had caused some drag on growth and credit cost, will start seeing growth from 2QFY27. It stated that the bounce trend in June is lower compared to that in April, which saw a better trend vs March.

RoA expansion led by broad-based metric improvement

The management expects overall profitability to improve, with RoA expanding to 2.5- 2.7% by FY28 owing to

1) Credit cost moderating to ~1%, which is an improvement of ~20bps from current levels

2) Opex-to-AUM further moderating by 15-20bps on account of improved efficiency and use tech (AI) across departments resulting in better productivity

3) NIM expansion, led by improving yields on the back of increasing share of high-yield products and risk-based pricing deviations in the company’s mass product segment. Further, it indicated it has not yet increased the PLR, but may do so if the scenario changes – it mentioned that none of its assets are repo-linked. It also mentioned that the current incremental COF is higher than in Mar-26, expected to uphold or moderate going ahead. The management expects competitive intensity in housing loans to moderate over time, and its share of prime housing loans to gradually decline.

We maintain ADD and Mar-27E TP of Rs390

We believe Tata Capital’s valuation is well supported by its strong execution, diversified franchise, and rising profitability, with RoA expected to rise to ~2.5% by FY28E, on margin gains, lower credit costs, and operating leverage. We retain ADD, with unchanged TP of Rs390, implying FY28E PBV of 2.6x.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

Tag News

L&T Finance gains on reporting 29% growth in Q1 consolidated net profit