Buy Tata Consultancy Services Ltd For Target Rs.2,500 by Prabhudas Liladhar Capital Ltd

Steady growth, optimistic of recovery from Q2

TCS reported 0.4% QoQ CC revenue growth, marginally ahead of our and consensus estimates; however, international business (excluding India) declined 0.2% QoQ (reported) after growing 1.6% QoQ in Q4FY26, reflecting the geo-political conflicts and continued macro uncertainty. While near-term demand remained soft across selected verticals such as Consumer and Manufacturing. The management sounded constructive and anticipates recovery in verticals except Consumer (non-essentials) from Q2FY27. Deal TCV was modest at USD9.5b, up 1% YoY, the ramp up of NN deal (US$800mn) should support the growth for the rest of FY27. Although the revenue from AI is growing at double-digit (QoQ), we believe the leakages in the traditional bucket are weighing on topline growth. We are keeping our growth rate (CC YoY) unchanged at 3.5% and 4.5% for FY27E/FY28E despite the mega deal awarded in Q1. On the margins front, Q1 margins were impacted by the annual wage hike (~170bps) along with continued investments in AI capabilities, partnerships, and net headcount additions (9k+QoQ). We are factoring in the Q1 miss and revise our margins downward by 40bps each for FY27E/FY28E, resulting in an EPS cut of 0.8% and 1.6%, respectively. We continue to value the stock at 15x FY28E EPS, to arrive at a TP of INR 2,500. Maintain BUY.

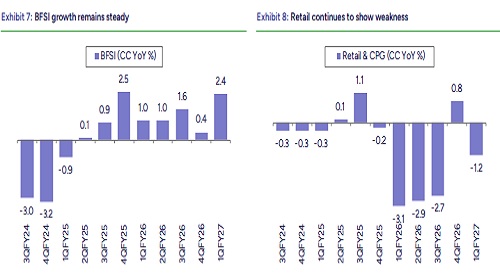

Revenue: TCS’s Q1 performance of 0.4% QoQ CC growth was marginally ahead of our & consensus estimates. Revenue growth was driven by BFSI, Tech & Regional Markets, which grew 1.6%, 1.7% & 4% QoQ CC respectively. Consumer Business, Healthcare, EURS & Manufacturing declined 4%, 1%, 0.7%, & -0.5% sequentially in CC terms respectively, & CMT remained flattish. In Q1 annualized AI revenue grew to USD 2.6 bn from USD 2.3 bn in Q4FY26, up 13.6% QoQ.

Operating Margin: EBIT margin declined by 130 bps QoQ to 24.0% below our estimate of 25% and largely in line of consensus estimate of 24.1%. Margin declined due to the headwinds from wage hikes (-170 bps) & continued investments which were partially offset by tailwinds from currency & operational efficiencies (+40 bps)

Deal Wins: TCS in Q1 won deals of USD 9.5 bn in line of historical Q1 trend. During the quarter it won 1 mega deals and TCV wins of USD 4.7 bn, 2.5 bn & 1.4 bn in North America, BFSI & Consumer respectively. TCS also won a net-new AI-led business transformation deals of US$ 800 mn mega deal from SKF.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271