Neutral Tata Communications Ltd for the Target Rs. 1,720 by Motilal Oswal Financial Services Ltd

Largely in-line results; digital revenue growth accelerates

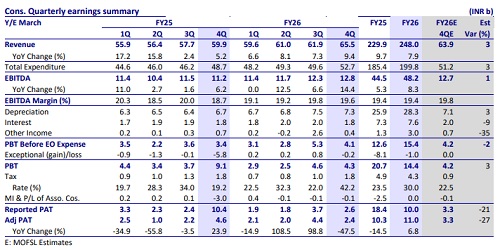

* Tata Communications (TCOM) delivered steady 4Q, with 11.5% YoY (~6% QoQ) data revenue growth driven by acceleration in Digital portfolio growth (+19% YoY, vs. ~15% YoY in 3Q) and ~4.5% YoY core-connectivity growth. However, adjusted for FX, consol. revenue growth was muted at ~3.7% YoY.

* TCOM’s consol. EBITDA grew ~14% YoY (4.5% QoQ) to INR12.8b, as margin expanded ~85bp YoY to 19.8% (though 25bp down QoQ, ~25bp miss).

* The order book remains strong, with healthy double-digit growth YoY, driven by large deal wins in international markets. The funnel remains robust with digital portfolio contribution at ~70%.

* The new leadership team refrained from providing any forward guidance, but indicated the continuation of existing strategy, with focus sharpening on driving absolute EBITDA growth through digital portfolio mix optimization. ? We build in ~9% data revenue CAGR over FY26-28E, with data revenue reaching INR255b by FY28. Acceleration in data revenue growth to midteens remains the key trigger for the stock.

* We raise our FY27-28E revenue and EBITDA by 2-3% each, driven by slightly higher data revenue growth. We build in ~13% EBITDA CAGR over FY26-28, with margin expanding to ~21% by FY28 (vs. 19.4% in FY26).

* We value TCOM’s data business at 9x FY28E EV/EBITDA and the voice and other businesses at 4x EV/EBITDA to arrive at our revised TP of INR1,720. We reiterate our Neutral rating. Acceleration in data revenue growth, along with margin expansion, remains key for re-rating.

Digital revenue growth accelerates, margins broadly steady in FY26

* Consolidated gross revenue grew ~9.4% YoY (~6% QoQ) to INR65.5b (vs. our estimate of INR63.9b). However, adjusted for FX benefits, the growth was relatively modest at ~3.7% YoY (+3.8% QoQ).

* Data revenue at INR56.8b (in line) grew 11.5% YoY (+6% QoQ), driven by ~19.2% YoY (~9% QoQ, 5% above) growth in the digital portfolio and ~4.5% YoY (+2.8% QoQ) growth in core-connectivity revenue.

* Consolidated net revenue (proxy for gross margin) at INR36.2b grew ~8.7% YoY (+4% QoQ), driven by higher growth in core-connectivity (+8% YoY).

* Consolidated adjusted EBITDA grew 4.5% QoQ (+14% YoY) to INR 12.8b (largely in line with our estimate).

* Consolidated adjusted EBITDA margin contracted 25bp QoQ (though up ~85bp YoY) to 19.6% (~25bp miss), driven by ~45bp QoQ decline in data EBITDA margin to 18.4% (though up ~95bp YoY).

* FY26 consol. revenue grew ~8% YoY to INR248b, with data revenue rising ~9.5% YoY to INR233b (core connectivity: ~3% YoY, DPS: ~17.5% YoY).

* FY26 reported EBITDA grew ~8% YoY to INR48.2b, with ~5bp margin contraction to 19.4%. However, pre-IND AS EBITDA grew relatively modest at ~5% YoY to INR42.5b, with margin contracting ~50bp YoY to 17.1%

* 4QFY26 consolidated PAT stood at INR2.4b (-48% YoY, -45% QoQ, ~27% below our estimate), primarily due to higher tax outgo (partly related to prior periods).

* FY26 adjusted PAT grew ~7% YoY to INR11b.

* Net debt declined INR4.8b QoQ to INR96b, with net debt-to-EBITDA moderating to ~2x (vs. 2.1x in Mar’25).

* Committed capex stood at ~INR5.4b in 4Q (vs. INR8b in 3QFY26), while cash capex rose ~25% QoQ to INR7.2b (up ~1.6% YoY).

* Reported FCF declined to INR 8.3b (vs. INR10.5b QoQ, INR0.7b YoY).

* Reported RoCE (annualized) improved to 14.9% vs 14.4% in 3QFY26.

Key takeaways from the management interaction

* CEO designate’s initial impressions: Conversations with enterprises are shifting beyond pure connectivity toward outcome-led discussions, especially around AI use cases. Clients increasingly expect integrated solutions spanning network, cloud, and AI capabilities. While TCOM remains a preferred partner for most of its clients, there is a need to better communicate TCOM’s integrated offerings to the clients.

* Key focus areas: The new leadership’s immediate priority is to improve profitability and the quality of growth. The aim is to achieve digital breakeven quickly while maintaining growth momentum. The focus will remain on sustainable and durable absolute EBITDA growth. Products such as multi-cloud connect and employee interaction platforms are gaining traction and offer higher margins. Scaling these offerings remains a strategic priority, and the portfolio mix shift towards these products will be the key driver of profitability improvement.

* Order book and funnel: The funnel remains robust, with ~70% of the funnel comprising digital services (vs. ~51% revenue contribution). Order bookings showed healthy double-digit growth, particularly in international markets.

* Normalized revenue growth: Adjusted for INR depreciation, revenue growth was modest at ~3.8% YoY (+3.7% QoQ).

* Near to medium term view: The company has transitioned through two phases: first achieving balance sheet discipline, and then investing in digital capabilities both organically and inorganically. It is now entering a third phase focused on profitable growth and capital discipline. Management aims to improve execution while maintaining strategic continuity.

Valuation and view

* We currently model ~15% CAGR in digital revenue over FY26-28 and expect digital to account for ~55% of TCOM’s data revenue by FY28 (vs. ~51% currently). Acceleration in digital revenue remains key for re-rating.

* Overall, we build in ~9% data revenue CAGR over FY26-28E, with data revenue reaching INR255b by FY28 (significantly lower than INR280b ambition by FY28).

* We raise our FY27-28E revenue and EBITDA by 2-3% each, driven by slightly higher data revenue growth. We build in ~13% EBITDA CAGR over FY26-28, with margin expanding to ~21% by FY28 (vs. 19.4% in FY26).

* We value TCOM’s data business at 9x FY28E EV/EBITDA and the voice and other businesses at 4x EV/EBITDA to arrive at our revised TP of INR1,720. We reiterate our Neutral rating. Acceleration in data revenue growth, along with margin expansion, remains key for re-rating.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)