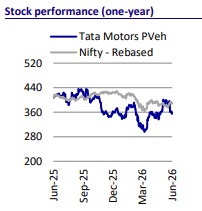

Sell Tata Motors Passenger Vehicles Ltd for the Target Rs 312 by Motilal Oswal Financial Services Ltd

India business to drive strong FCF over the next five years Aims to increase PV share by 5-6% to over 20% by FY31

We attended the Tata Motors Passenger Vehicles’ (TMPV) Analyst Meet today. Management has laid out a five-year roadmap till FY31, which includes:

1) 15% volume CAGR (half of the same achieved in FY21-26) that will drive a 5-6% rise in market share to 20%,

2) structural cost reduction, with an aim to reduce costs by 5-6%. These goals are expected to help the company drive standalone business EBIT margin to 5% without PLI from 1.4% (with PLI) and deliver cumulative FCF of INR100b over this period. Its volume growth is expected to be driven by six new nameplate launches and over 20 refreshes. The company would continue to adopt a multi-powertrain approach, with the bulk of its incremental volumes coming from EV+CNG powertrains.

Other critical enablers include:

1) Ramping up its dealer network to 3,200 outlets from 1,669 currently

2) Increasing the count of service centers to 3k+ from 1,211 now

3) Ramping up annual production capacity to 1.3m units from 900k currently. However, while the Indian PV demand outlook remains positive, the company is expected to experience margin pressure in the near term, given the material surge in input costs. Further, JLR continues to face multiple headwinds, both on the demand and cost front. Given significant challenges at JLR and the continued geopolitical uncertainty, we reiterate our Sell rating on the stock with an SoTP-based TP of INR 312 per share (based on FY28E).

Management outlines a five-year roadmap for the India PV business

Management’s five-year guidance for the India PV business includes: 1) revenue target of INR1,400b, 2) EBITDA margin of 10% and EBIT of 5%+ (ex PLI), 3) PBT >5x, and 4) Cumulative FCF of INR100b, largely back-ended, given the expected higher capex during initial years.

TMPV targets to gain a substantial share in PVs

Management expects the industry to post 6-7% volume CAGR over the next five years. However, TMPV targets to clock 15% volume CAGR over this period, which is half of that achieved in the prior five-year period. This would, in turn, drive a healthy 5-6% market share improvement in PVs to about 20%. To achieve this, it plans to launch six new nameplates and over 20 product refreshes.

Stringent cost-cutting to help drive improved performance

Management targets to achieve a 360bp EBIT margin expansion over the next five years despite the expected cessation of PLI benefit from FY29 onwards.

This would largely be driven by:

1) Operating leverage

2) Cost reduction of 5-6% over this period.

Valuation and view

While the Indian PV demand outlook remains positive, the company is expected to experience margin pressure in the near term, given the material surge in input costs. Further, JLR continues to face multiple headwinds, both on the demand and cost front. Given significant challenges at JLR and the continued geopolitical uncertainty, we reiterate our Sell rating on the stock with an SoTP-based TP of INR 312 per share (based on FY28E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412