Sell Tata Elxsi Ltd for the Target Rs 3,100 by Motilal Oswal Financial Services Ltd

Vertical recovery remains uneven Transportation vertical remains soft; margins disappoint

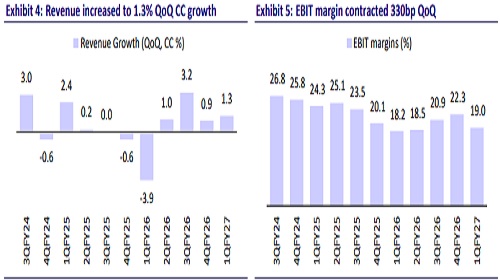

* Tata Elxsi (TELX) reported revenue of USD108m in 1QFY27, up 1.3% QoQ in CC terms, broadly in line with our estimate of 1.2% QoQ CC. Growth was led by Media and Communication/Others, which grew 2.9%/21% QoQ CC, whereas HLS/Transportation declined 0.3%/0.4% QoQ CC. EBIT margin was 19% (down 330bp QoQ), below our estimate of 21.5%. Adj. PAT declined 22.6% QoQ and rose 18.2% YoY to INR1,706m (below our est. of INR2,027m).

* For 1QFY27, revenue/EBIT/adj. PAT grew 14.5%/19.2%/18.2 YoY in INR terms. We expect revenue/EBIT/adj. PAT to grow 12%/18.1%/21.7% YoY in 2QFY27. We value TELX at 21x FY28E EPS (earlier 22x), resulting in a revised TP of INR3,100. We reiterate our Sell rating.

Our view: Current valuation leaves limited room for disappointment

*1Q does little to change the broader growth picture: Revenue grew 1.3% QoQ CC, broadly in line with expectations, but the improvement was largely driven by Media & Communications, while Transportation and Healthcare remained weak. We believe meaningful growth will require a recovery in the larger Transportation business (~55% of revenue), where spending remains cautious, particularly across Europe.

* Margins came in well below expectations: EBIT margin contracted to 19%, below our estimate of 21.5%. Management attributed this to ~150bp of one-off costs (deal transitions, a customer-specific Chapter 11 provision, and retention costs), ~220-230bp of higher onsite delivery and subcontractor costs tied to H-1B visa constraints, and AI infra investments.

* A company-wide wage hike in 2Q will further offset any near-term unwind of these costs. We believe recovery could remain gradual, given the uneven demand environment and the need to continue investing in talent and capabilities.

* Transportation recovery remains the key monitorable: Transportation, the company's largest vertical, declined this quarter, reflecting continued weakness in automotive engineering spends. While Media & Communications can support growth in the near term, we do not believe it will be sufficient to drive a sustained acceleration without a broader improvement in Transportation and Healthcare.

* Valuation continues to discount a stronger recovery than what we see: We believe that revenue recovery remains concentrated in a few pockets, while Transportation demand has yet to turn and margins remain below historical levels. At 28x/24x FY27E/FY28E consensus P/E, we believe the current valuation leaves limited room for disappointment. We would look for broader-based growth across verticals and a more sustained margin recovery before turning more constructive on the stock.

Valuation and view

* We lower our FY27/FY28 EPS estimates by ~5%/~1%, reflecting weaker-thanexpected margin performance in 1Q and a slower recovery in the Transportation business. While some of the margin headwinds are one-off in nature, we expect margin recovery to remain gradual amid continued investments, wage hikes in 2Q, and an uneven demand environment. We continue to model USD revenue CAGR of ~5.5% over FY26–28. We value TELX at 21x FY28E EPS (earlier 22x), resulting in a revised TP of INR3,100. We reiterate our Sell rating.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412