India`s BoP to Record a Surplus in FY27 by CareEdge Ratings

The global economic landscape continues to be characterised by uncertainty stemming from the evolving geopolitical dynamics. The US-Iran Memorandum of Understanding (MOU) signed in mid-June brought relief to global markets but was short-lived as recent flare-ups have reignited geopolitical concerns. Brent crude oil prices have declined markedly but remain volatile. Against this backdrop, we evaluate India’s external sector performance and the outlook for FY27.

In FY27 so far, India’s merchandise exports have shown an improving performance. Furthermore, the resilience in services exports and remittances has continued. We are lowering our current account deficit projection for FY27 to 0.8-1.2% of GDP from our previous projection of 2.1%. The lowering of the CAD projection is mainly because of moderation in crude oil prices and resilience in services exports and remittances, coupled with an improvement in merchandise exports. Our revised CAD projection is based on the assumption that crude oil price will average around USD 80-85/bbl in FY27. If global crude oil prices remain lower, the CAD could slip below 1% of GDP. It is worth noting that CAD in FY26 was at 0.6% of GDP, supported by strong growth in services exports and low crude oil prices.

Within the capital account, we expect net FDI to improve from USD 6.9 billion in FY26 to USD 15 billion in FY27, driven by healthy growth in gross FDI inflows and some tapering of growth in repatriation. The recent measures introduced by the government and the RBI to attract foreign capital are expected to aid in FPI and other capital inflows. The concessional swap windows for FCNR(B) deposits, External Commercial Borrowings (ECBs) and Overseas Foreign Currency Borrowings (OFCBs) are collectively likely to generate USD 45-60 billion inflows in FY27. As a result, we expect the capital account surplus to increase from a feeble USD 2 billion in FY26 to approximately USD 73 billion in FY27. Hence, we expect BoP to move to a surplus in FY27 after two consecutive years of deficit.

Merchandise Exports Off to a Strong Start in FY27

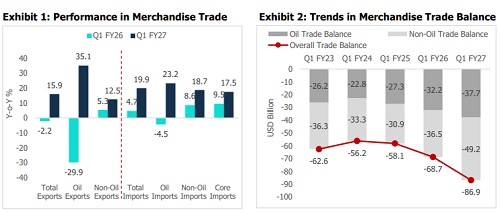

India’s merchandise exports grew by 15.9% during Q1 FY27 (Refer to Exhibit 1). Petroleum exports rose by 35.1%, supported by high global crude oil prices amid the West Asia conflict. However, in volume terms, India’s petroleum exports contracted sharply 20% during 2M FY27. This can be attributed to the curbs on petroleum exports to ensure adequate domestic availability amid disruptions in the global energy supply. A favourable development on the trade front has been the encouraging start to FY27 for non-petroleum exports, which logged an encouraging growth of 12.5% during Q1 FY27. This marks an improvement over the 3.6% growth recorded in full-year FY26. We expect this encouraging momentum in merchandise exports to continue going forward. However, the possibility of a higher 12.5% tariff by the US on Indian exports (compared to 10% for many other economies) remains a monitorable. India’s overall imports increased by 19.9% during Q1 FY27, driven not only by a sharp increase in oil imports (23.2%) but also higher gold and core imports. Core imports (non-oil and non-gold/silver imports) grew by 17.5% (y-o-y) while gold imports increased by a strong 46.7% during the same period. However, gold imports have moderated since May following the hike in import duty on gold and silver. Additionally, import of electronic goods (17.8% share in total imports) have shown a notable growth of 43.8% in Q1 FY27.

Engineering and Electronic Goods Continue to Gain Share in Non-Petroleum Exports in Last Decade

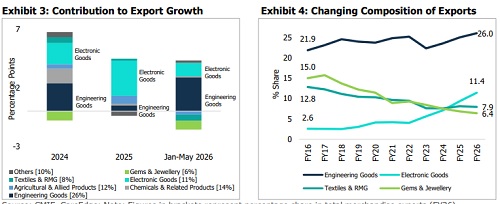

Electronic and engineering goods have emerged as the key drivers of India’s merchandise exports in the last decade. Exports of electronic goods increased by 22.6% (y-o-y) during Q1 FY27 after recording 23.3% growth in full-year FY26. Additionally, exports of engineering goods have continued to show an encouraging trend, rising by 18.2% (y-o-y) during Q1 FY27, following 4.9% growth in FY26. On the downside, labour-intensive segments such ready-made garments (RMG) remained under pressure, contracting by 12.4% in Q1 FY27. RMG exports performed weakly in full-year FY26 amid persistent global economic challenges. Overall, engineering and electronic goods have been the positive contributors to the export growth (Refer to Exhibit 3).

A decadal analysis shows that India's export basket has undergone a notable shift over the past decade, with engineering and electronic sectors gaining prominence. The share of engineering goods in India’s total exports has climbed to 26% in FY26 from close to 22% in FY16. An even more noteworthy trend has been the rapid rise in electronics exports, whose share more than quadrupled to 11.4% from just 2.6% a decade back. On the contrary, the share of labour-intensive exports such as textiles & ready-made garments and gems & jewellery has declined over the last decade (Refer to Exhibit 4).

Share of India’s Merchandise Exports to Asia and Africa Edges Up in the Recent Quarters

India's merchandise exports have faced persistent headwinds since the beginning of last year, initially due to heightened tariff-related uncertainties and, more recently, owing to the conflict in West Asia. Against this backdrop, we evaluated trends in export shares of key regions and export partners over the recent quarters. Amid elevated tariff uncertainty last year, trade front-loading supported India’s exports to the US, with its share in total exports climbing to around 23% in the initial quarters of 2025. Since then, the share of the US in India’s exports has normalised to around 18-19% in the recent quarters. The share of exports to Europe has moderated over the last few quarters, declining to 20.1% in 2M FY27, down from 22.3% in Q1 FY26 (Refer to Exhibit 5). This moderation can be attributed to the Netherlands’ declining share in our exports (Refer to Exhibit 6)

On the contrary, Africa’s share has risen consistently to 12.3% during 2M FY27, up from 9.7% in Q1 FY26. This was aided by the rising share of exports to South Africa and Tanzania. The share of Asia (around 39%) in India's exports, which had been on an upward trajectory until Q3 FY26, moderated slightly thereafter, likely reflecting disruptions arising from the conflict in West Asia (Refer to Exhibit 5). While there has been a notable rise in the share of exports to Singapore, the gains have been somewhat offset by a decline in the share of exports to the UAE..

Above views are of the author and not of the website kindly read disclaimer

.jpg)

Tag News

India's BoP to Record a Surplus in FY27: CareEdge Ratings