Neutral L&T Technology Ltd for the Target Rs 3,400 by Motilal Oswal Financial Services Ltd

Turning more stable Sustainability vertical doing the heavy lifting; Europe remains a drag

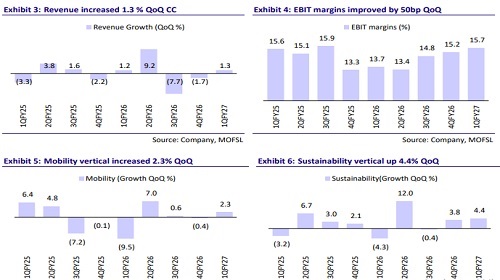

* L&T Technology’s (LTTS) 1QFY27 revenue grew 1.5% QoQ in CC terms, in line with our estimate. Sustainability/Mobility grew 4.3%/2.3% QoQ, while Tech was down 3.1% QoQ.

* EBIT margin stood at 15.7%, up 50bp QoQ and above our est. of 15.4%. Adj. PAT rose 1.5% QoQ/17.4% YoY to INR3.6b, in line with our estimate.

* For 1QFY27, revenue/EBIT/adj. PAT grew 11.5%/28.1%/17.4% YoY in INR terms. In 2QFY27, we expect revenue/EBIT/adj. PAT to grow 0.5%/17.3%/ 11.7% YoY. We reiterate our Neutral rating on the stock with a TP of INR3,400, implying a 3% potential upside

Our view: 2Q likely to be better

* Management expects growth to improve from hereon, though we believe the recovery is still in its early stages: LTTS reported 1.5% QoQ CC revenue growth in 1QFY27, led by Sustainability and an improving Mobility business. A couple of large telecom and MedTech deals slipped into early 2Q, delaying revenue by a quarter, but management expects both to start ramping up immediately after the closure.

* Demand commentary has slightly improved vs. the last few quarters, with better traction in the US and continued strength in Sustainability. However, Europe auto remains weak and clients remain selective on spending. While 2Q is likely to be better, we believe a few quarters of consistent execution will be needed. We now build in organic revenue growth of 3.5% YoY cc and total revenue growth of 5% YoY in USD in FY27.

* Sustainability continues to do the heavy lifting, while Mobility recovery remains gradual: Sustainability division grew 4.3% QoQ, driven by plant engineering, industrial products and data center-related investments, with management reiterating double-digit growth guidance for FY27. Mobility also improved, led by aero, rail and off-highway, though Europe OEMs and Tier-1 demand remained weak. Hi-Tech was soft due to delayed telecom and MedTech deal closures, with management expecting growth to resume from 2Q.

* Margin execution remains key to reaching mid-16%: EBIT margin expanded 50bp QoQ to 15.7%, helped by a richer business mix, operational discipline and AI-led productivity. Management reiterated its target of reaching a mid-16% EBIT margin by 4QFY27. We believe further margin improvement will depend on Hi-Tech recovery, a richer business mix and execution of higher-margin outcome-based deals. We expect FY27E EBIT margin of 15.8%, implying gradual rather than sharp expansion

* AI is supporting client engagement, though productivity pass-through remains a medium-term watch-point: Management noted that AI now features in almost every client discussion, with engagements increasingly moving from consulting to implementation. LTTS also strengthened its AI ecosystem through partnerships with Anthropic (Claude) and Databricks, complementing its engineering intelligence platforms. These initiatives should support market share gains and larger transformation opportunities, though pricing and productivity pass-through are likely to remain an overhang.

Valuation and view

* We model a USD revenue CAGR of 7% over FY26-28E, with 5% YoY USD growth in FY27E, as Sustainability remains the key growth driver, Mobility improves gradually and Hi-Tech recovers as delayed deals ramp up. While management commentary has turned more constructive, we believe a few more quarters of consistent deal conversion and execution will be needed before building in a stronger growth trajectory.

* We expect EBIT margins to improve to ~15.8% by FY27E, led by better mix and execution. We maintain our Neutral rating with a TP of INR3,400, based on 20x FY28E EPS

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)