Buy Billionbrains Garage Ventures Ltd for the Target Rs 250 by Motilal Oswal Financial Services Ltd

Robust YoY growth momentum; 12% PAT beat

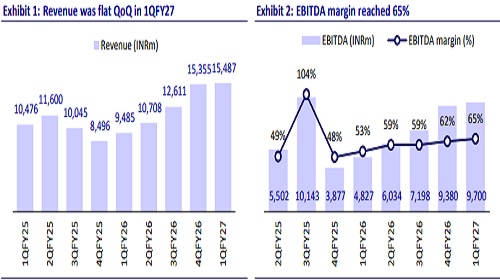

* Billionbrains Garage Ventures (GROWW) reported an operating revenue of INR15b in 1QFY27, reflecting growth of 66% YoY (in line).

* Operating expenses rose 26% YoY to INR5.3b in 1QFY27 (14% below est.), with employee expenses increasing 33% YoY (in line) and other expenses increasing 23% YoY (19% below est.). EBITDA doubled YoY to INR9.7b, reflecting an EBITDA margin of 64.6% (53.4% in 1QFY26 and MOFSLe of 63.1%).

* PAT for the quarter came in at INR7.4b, growing 94% YoY (up 7% QoQ; reflecting a 12% beat on our estimates).

* As established businesses continue to gain operating leverage and new products are largely being built by existing teams, management expects the overall cost structure to remain relatively stable.

* We have largely maintained our top-line estimates, with lower cash and derivatives revenue being offset by higher MTF revenue. We have increased our earnings estimates by 1%/3% for FY27/28, considering the improved operational efficiency. We reiterate our BUY rating with a revised TP of INR250 (premised on 38x FY28E EPS).

Broking revenue/order improves; MTF surge continues

* Broking revenue rose 58% YoY to INR11.4b, driven by 48% YoY growth in orders to 560.2m as well as an increase in revenue per order to INR20.3 (INR19.0 in 1QFY26).

* Derivatives revenue grew 51% YoY but declined 4% QoQ to ~INR8.1b, driven by lower volatility amid an easing geopolitical environment. GROWW’s retail options premium ADTO market share was 11.0%, up from 7.2% in 1QFY26.

* Cash revenue grew 39% YoY/flat QoQ to ~INR2.5b, with ADTO market share at 15.1% (11.8% in 1QFY26). The sequential dip was attributed to risk control measures, such as the tightening of limits across MTF and intraday. Cash orders witnessed ~9% sequential decline due to lower demand for commodity ETFs during the quarter.

* Commodity derivatives benefited from growth in user adoption and industry momentum, with revenue growing 10% QoQ and contributing 5% to GROWW’s total operating revenue. Launched in 3QFY26, commodity derivatives currently have 435,000 active users, implying an attach rate of 2.6% in overall active users.

* MTF revenue grew 17% QoQ to INR1.2b (INR285m in 1QFY26), with MTF book scaling to INR37.7b by the end of 1QFY27 (INR28.1b in 4QFY26), resulting in a stable market share of 2.7%.

* The credit segment’s revenue rose 36% YoY/7% QoQ to INR852m. Disbursement by partners declined sequentially to INR3.7b, while Groww Creditserv’s (GCS) disbursements increased sequentially to INR4.9b. 35% of GCS’ disbursals were from LAS.

* The AMC’s AUM has reached INR55b. It reported an operating loss of INR169m

* The wealth management business (Fisdom) reported an operating loss of INR109m in 1QFY27.

* Customer acquisition cost (CAC) surged to ~INR1,900, with the transacting user base reaching 22.4m by the end of 1QFY27. Branding spends during the IPL prompted a rise in acquisition costs during the quarter.

Valuation and view

* GROWW continues to report strong revenue growth YoY, backed by rising user adoption of products as well as robust user activation. Its brokerage business is gaining market share across segments, with recent product launches, such as MTF and commodities, fueling further growth.

* We expect the overall orders in the broking segment to report over 20% growth over FY27-28, backed by market share expansion and improving revenue per order. The MTF segment, LAS, and wealth management are expected to provide an additional boost to top-line growth.

* We have largely maintained our top-line estimates, with lower cash and derivatives revenue offset by higher MTF revenue. We have increased our earnings estimates by 1%/3% for FY27/28, factoring in improved operational efficiency. We reiterate our BUY rating with a revised TP of INR250 (premised on 38x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)