Neutral ACC Ltd for the Target Rs.1,310 by Motilal Oswal Financial Services Ltd

Weak performance; merger with ACEM expected in FY27

Expects soft demand in FY27; geopolitical issue-led fuel price volatility likely to persist

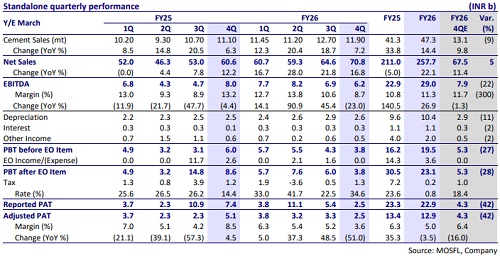

* ACC’s 4QFY26 earnings were below our estimates. EBITDA declined ~23% YoY to INR6.2b (~22% miss). EBITDA/t fell ~28% YoY to INR518 (est. INR605). OPM contracted 4.5pp YoY to ~9% (-3pp vs. our estimate). Adj. PAT declined ~51% YoY to INR2.5b (~42% miss).

* Management indicated that demand growth in FY27 is expected to remain soft at 5% due to a weak monsoon, which could dent agricultural output and housing demand. However, India’s long-term infrastructure growth outlook remains strong. Due to West Asia crises, fuel prices remain volatile. ACC continues to focus on strengthening brand penetration, scaling up trade sales, and driving premiumization across its portfolio.

* We cut our EBITDA estimate for FY27 by ~8% due to cost pressure, though we maintain it for FY28. The stock is trading at 8x/6x FY27E/FY28E EV/EBITDA and USD59/USD53 EV/t. We value the stock at 6x FY28E EV/EBITDA to arrive at our TP of INR1,310. Reiterate Neutral.

Sales volume up ~7% YoY; EBITDA/t at INR518 (est. INR605)

* 4QFY26 revenue/EBITDA/PAT stood at INR70.8b/INR6.2b/INR2.5b (+17%/- 23%/-51% YoY and +5%/-22%/-42% vs. estimates). Sales volume was up ~7% YoY at 11.9mt (-9% vs. est.). Cement realization up ~8% YoY. RMC revenue grew ~37% YoY to INR5.7b.

* Opex/t was up 15% YoY (up ~19% QoQ), led by increase in variable/other expenses/freight cost per ton by ~18%/13%/9%. EBITDA/t declined 28% YoY to INR518. Depreciation increased ~2% YoY and finance cost rose 96%. Other income fell ~15% YoY. Effective tax rate was 34.6% vs. 14.4% in 4QFY25.

* In FY26, revenue/EBITDA grew 20%/22% YoY to INR255.3b/INR29.0b, while adj. PAT declined 4% YoY to INR12.9b. Blended realization/t rose ~5% YoY to INR5,402 and EBITDA/t was up ~6% YoY at INR613. OPM remained flat YoY at ~11%. It posted operating cash outflow of INR11.7b vs. OCF of INR17.1b, mainly due to a surge in working capital during the year. Capex stood at INR13.3b vs. INR15.3b in FY25. Net cash outflow stood at INR25.0b vs. net cash inflow of INR1.8b in FY25.

Key highlights from the management commentary

* Cost pressure from fuel, diesel, packaging bag supply constraints, and INR depreciation impacted the quarter and these challenges are expected to persist in 1HFY27.

* Fuel cost stood at INR1.65 vs. INR1.47/INR1.68 in 4QFY25/3QFY26. It stood at INR1.61 in FY26, similar to FY25. Primary lead distance increased by 3km YoY to 273km in 4Q; however, it declined by 5km YoY to 269km in FY26.

* The Salai Banwa (UP) and Kalamboli (MH) expansions are expected to be completed in 1QFY27, adding 3.4MTPA of cement capacity.

Valuation and view

* ACC’s operating performance in 4QFY26 was below our estimates due to lowerthan-estimated volume growth and higher-than-estimated opex/t. Its net cash balance declined sharply to INR4.8b vs. INR29.8b in FY25 due to a significant increase in working capital. Trade receivables have increased by INR25b during the year. The merger scheme with ACEM has been filed with stock exchanges and SEBI’s NOC is awaited, with completion expected in FY27.

* We estimate a CAGR of 12%/18%/31% in revenue/EBITDA/PAT over FY26-28, albeit on a low base. We estimate a healthy volume CAGR of ~11% over FY26-28, given higher volume through MSA. We estimate its EBITDA/t at INR617/ INR695 in FY27/FY28 vs. INR614 in FY26. The stock has seen significant de-rating in valuations due to continuing weak profitability. We value the stock at 6.0x FY28E EV/EBITDA to arrive at our TP of INR1,310. Reiterate Neutral.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)