Buy Marico Ltd For Target Rs.950 by Motilal Oswal Financial Services Ltd

Consistency intact; FY27 earnings to be an outlier among peers

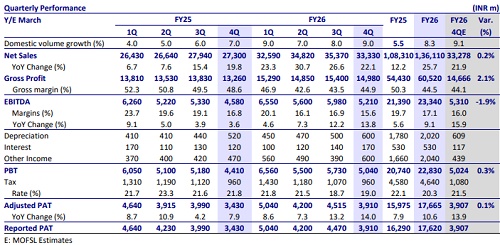

* Marico (MRCO) reported consolidated revenue growth of 22% YoY (in line) in 4QFY26. Domestic revenue grew 21% YoY, with volume growth of 9% YoY (in line). International revenue grew 19% YoY (+25% CC). Demand remained stable in 4Q; however, geopolitical crises in the Middle East pose near-term macro risks.

* Gross margin contracted 360bp YoY to 44.9% (est. 44.1%), while improving 140bp QoQ owing to the recent correction in copra prices. That said, vegetable oils and other crude-linked inputs are expected to remain inflationary given the ongoing geopolitical developments. EBITDA margin contracted 110bp YoY to 15.6% in 4Q (in line), while EBITDA grew 14% (est. 16%). Management expects to deliver high-teens EBITDA growth in FY27.

* MRCO expects to sustain high single-digit volume growth in the India business in FY27, driven by both the core portfolio and new growth engines. International business is expected to deliver mid-teen constant-currency (CC) growth driven by broad-based performance across markets. At a consol. level, the company aims to achieve double-digit revenue growth, surpassing INR150b in FY27. In the medium term, MRCO aspires to cross INR200b by FY30 (10-11% CAGR) along with mid-teens EBITDA CAGR. The management expects GM to expand 350-400bp in FY27, while EBITDA is likely to expand +150bp (with upside risk if the crude basket becomes soft).

* The company aims to deliver double-digit revenue CAGR over FY26-30, aided by strong volume growth and CC growth in the teens in international business with mid-teens EBITDA CAGR. In line with its aspiration, we model a 12% revenue and 19% EBITDA CAGR over FY26-28E. Given its sustained growth trajectory, diversifying revenue streams, and strong focus on TAM expansion, we believe the stock’s premium valuation is likely to be sustained. MRCO remains one of our topics in our coverage universe. We reiterate our BUY rating on the stock with a TP of INR950 (based on 50x Mar’28E EPS).

In-line performance; volume growth at 9%

* Strong revenue growth trajectory continues: Consolidated net sales grew 22% YoY to INR33.3b (est: INR33.3b) in 4QFY26. Domestic sales rose 21% YoY, while domestic volumes grew 9% YoY (est. 9%). The international business delivered 19% CC growth (25% in INR terms), led by Bangladesh/ Vietnam/South Africa, which posted 35%/18%/8% CC growth in 4Q. However, MENA declined 7% in CC as the ongoing geopolitical headwinds weighed on the business in Mar’26.

* Broad-based growth across categories: Parachute Coconut Oil (PCNO) posted a 29% YoY value growth with a 1% volume decline, primarily driven by price hikes. Copra prices have corrected ~35% from the peak levels, and management expects it to remain rangebound in the near term. MRCO has already undertaken ~10% price cuts in non-price point packs following the correction in copra prices and expects volume recovery from 1QFY27. Value-added Hair Oils (VAHO) continued their growth recovery, with revenue rising 26%. Saffola oil clocked 8% revenue growth during the quarter, driven by mid-single-digit volume growth. MRCO will implement necessary pricing action to offset any cost escalations. The Foods portfolio grew 16% YoY and exited the year at INR10b+ in revenue. The digital-first portfolio clocked an exit ARR of ~INR11b.

* Contraction in margins, reversal in FY27E: Consol. gross margin contracted 360bp YoY to 44.9% (est. 44.1%), while improving 140bp QoQ owing to the recent correction in copra prices. Management indicated that copra prices have dropped ~35% from peak levels, and MRCO expects them to remain rangebound in the near term. Employee expenses were up 14% YoY, ad-spending rose 5% YoY, and other expenses were also up 18% YoY. EBITDA margin contracted 110bp YoY to 15.6% in 4QFY26 (est. 16%).

* Double-digit growth in profitability: EBITDA grew 14% YoY (est. 16%). PBT/PAT grew 14% YoY each to INR5b/INR3.9b/ (est. INR5b/INR3.9b).

* In FY26, net sales, EBITDA, and APAT grew 26%/9%/11%.

Highlights from the management commentary

* In PCNO, management expects visible recovery in volume growth from 1QFY27. The company has already undertaken ~10% price cuts in non-price point packs following a correction in copra prices.

* Copra price correction is expected to support margins in FY27. Weighted average input cost inflation for FY27 is currently expected to remain marginal.

* Gross margin is likely to expand 350-400bp in FY27, supported by easing copra costs. Part of the gross margin benefit is expected to be reinvested in A&P.

* Management expects ~150bps operating margin expansion in FY27, considering the uncertain operating environment.

* The VAHO portfolio is expected to sustain double-digit volume-led growth going ahead.

* The Middle East exposure remains relatively limited for the company, reducing overall business risk from the region.

* Premiumization is gaining traction in International business, with premium categories rising from ~20% to ~30% over FY20-FY26 and projected to reach ~40% by FY30, supporting a structurally stronger and more balanced growth profile.

Valuation and view

* We largely maintain our EPS estimates for FY27 and FY28. ? MRCO plans to surpass INR150b in revenue in FY27 and INR200b by FY30. The company aims to deliver a double-digit revenue CAGR over FY26-30, backed by strong volume growth and international business growth in the teens (CC) with mid-teens EBITDA CAGR.

* Diversification is steadily improving the resilience of the international portfolio, with Bangladesh’s revenue share declining from ~50% in FY20 to ~45% in FY26 and expected to reduce further to ~35% by FY30.

* To improve its domestic distribution reach, MRCO has also started Project SETU, which helps drive growth in GT through a transformative expansion of its direct reach.

* In line with its aspiration, we model a 12% revenue and 19% EBITDA CAGR over FY26-28E. Given its sustained growth trajectory, diversifying revenue streams, and strong focus on TAM expansion, we believe the stock’s premium valuation is likely to be sustained. MRCO remains one of our topics in our coverage universe. We reiterate our BUY rating on the stock with a TP of INR950 (based on 50x Mar’28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412