Buy Aditya Birla Real Estate Ltd for Target Rs. 1,880 by Choice Institutional Equities

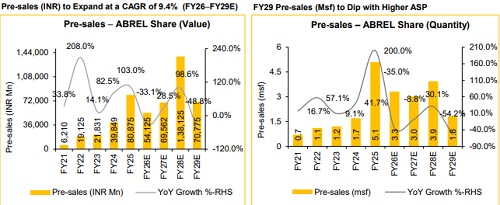

Sustainable Growth with Strong Pre-sales & Launch Pipeline

ABREL has materially strengthened its development pipeline to over INR 700 Bn GDV (35.1 msf), spanning INR 262 Bn (16.1 msf) of ongoing and INR 441 Bn (19.0 msf) of upcoming projects. The company has a welldiversified presence across high-growth markets, led by MMR (~61%), followed by NCR (~19%), then Bengaluru (~12%) and Pune (~8%). A key value driver is its 30-acre, zero-cost, freehold Worli landholding in one of Mumbai’s most supply-constrained premium micro-markets, offering multidecade value. The company is also scaling up its Grade-A commercial portfolio, which is anchored by operational assets: Birla Centurion (0.32 msf) and Birla Aurora (0.26 msf), alongside ~2 msf of upcoming commercial tower on Niyaara land and the Century Bhavan redevelopment. The portfolio, from ~INR 1.3 Bn in FY26E, is targeting a sharp ramp-up in annuity income to ~INR 10 Bn in the next 3–4 years.

Positioning in Premium Real Estate Segment with Brand Moat

ABREL benefits from Aditya Birla Group’s strong brand equity and governance standards, thus reinforcing customer trust and premium positioning. It stands out as the only real estate developer to have received the Golden Peacock National Quality Award 2025, underpinned by bestin-class execution and sustainability credential, including India’s first LEED Platinum pre-certified residential project. Also, most of the projects are being executed through negative capital and negligible construction loan. With a portfolio anchored in prime micro-markets, the company is well-placed to capture incremental market share amid rising demand for organised, branded real estate. ABREL luxury focus offers relative resilience to cyclical slowdowns, given lower sensitivity to interest rates and near-term economic volatility.

Strategic Capital Deployment and Scalable Asset-light Model

CCI’s approval of the slump sale of Century Pulp & Paper business worth INR 34.98 Bn to ITC marks a pivotal balance sheet inflection, with the proceeds earmarked for material deleveraging and growth. This is further reinforced by IFC’s INR-4.2 Bn equity commitment for projects in Pune and Thane, alongside Mitsubishi Estate’s INR-5.6 Bn JV investment in Birla Evara, Bengaluru—its first real estate investment in India–signals global institutional validation. Additionally, ABREL focuses on JVs, JDAs and outright acquisition in all its existing markets to scale rapidly.

Valuation and View

(Bull Bear Case Scenario) We initiate coverage on ABREL with a BUY recommendation and target price of INR 1,880/sh, which is an upside of 21.5%, employing a SOTP valuation framework. We value its residential and commercial ongoing and upcoming projects on the basis of the DCF approach, using a WACC of 11.6%, and its commercial projects on 7.0% cap rate. Our upside scenario (15–20% probability event) fair value is INR 2,365/sh. On the other hand, our downside scenario (5–10% probability event) fair value is INR 1,435/sh.

Key Risks

Any moderation in luxury demand or probable delays in securing key approvals (CC/OC) could adversely impact execution timelines and temper growth momentum. Rising construction cost could lead to margin pressure. Additionally, reliance on JDA structure risks partner alignment.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131