Buy ACME Solar Holdings Ltd for the Target Rs. 410 by Motilal Oswal Financial Services Ltd

Earnings outlook remains positive

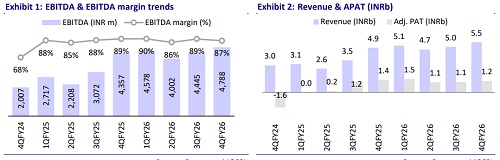

* In-line 4Q: ACME Solar Holdings (ACME) reported an in-line performance in 4QFY26, with revenue of INR5.4b and EBITDA of INR4.8b. APAT of INR1.3b was 14% above our estimate, driven by higher-than-expected other income. For FY26, revenue/EBITDA/APAT stood at INR20b/INR18b/INR5b, reflecting YoY growth of 44%/44%/82%.

* Key things we liked about the result:

1) Capacity commissioning remains on track, with guided 450MW operationalized during FY26

2) PPA secured for 65% of total pipeline of 5GW, providing capacity addition visibility up to FY28

3) the company targets commissioning 10GWh battery energy storage system (BESS) capacity by FY27 end, of which 8.5GWh is planned to operate under merchant/short-term contracts, offering potential earnings upside.

* Key monitorables include:

1) Pace of commissioning against FY27 guidance of 1.5GW RE capacity addition

2) progress of targeted 10GWh BESS capacity by end-FY27

3) merchant spreads from BESS and their contribution to earnings in FY27.

* Valuation and view: We have incorporated the merchant BESS capacity additions for FY27/FY28, resulting in a 6%/4% increase in our EBITDA estimates. We value the stock at 10x FY28E EBITDA, leading to a TP of INR410.

In-line revenue and EBITDA; higher other income drives PAT beat

* Financial highlights

* ACME’s consol. revenue and EBITDA came in line at INR5.5b (+13% YoY, +10% QoQ) and INR4.8b (+10% YoY, +8% QoQ), respectively.

* Adj. PAT beat our est. by 14% to INR1.3b (-9%% YoY, +10% QoQ), driven by higher-than-expected other income on account of high hedging gains.

* In 4QFY26, generation stood at 1,720MUs (+14%YoY, +10%QoQ).

* Other highlights

* Commissioned BESS capacity of 2.3GWh till date, which has begun generating revenue under merchant/short-term peak power contracts.

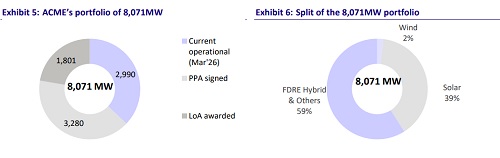

* Total portfolio now stands at 8,071MW – operational capacity at 2,990MW, under-construction portfolio of 5,081MW (of which PPA is signed for 3,280MW), and 550MWh standalone BESS (PPA signed).

* There was an exceptional gain of INR143m pertaining to contingent considerations received with respect to investments disposed of in earlier year and prepayment of borrowings by subsidiaries.

* 4Q CUF stood at 26.9% (vs. 27.9%/24.3% in 4QFY25/3QFY26), while plant availability stood at 99.3%.

* Connectivity inventory of ~9.6GW (secured/applied) available for upcoming bids. 15,000+ acres stand acquired for under-construction portfolio.

* Mr. Rajat Kumar Singh has resigned as Group CFO, effective 8th May’26, citing personal reasons. The board has appointed Mr. Arun Chopra (currently EVP, Finance & Accounts) as CFO, effective the same date.

Valuation and view

* We reiterate our BUY rating on ACME with a TP of INR410. We assign an EV/EBITDA multiple of 10x to FY28E EBITDA. Adjusting for net debt, we derive our TP of INR410, implying a 45% potential upside.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412