Buy JSW Energy Ltd for the Target Rs. 640 by Motilal Oswal Financial Services Ltd

Soft 4Q; capacity additions to drive FY27 growth

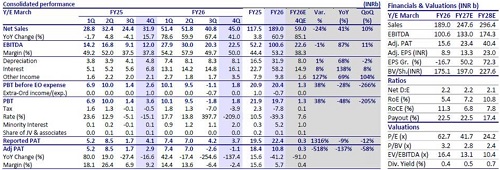

* JSW Energy (JSWE)’s 4QFY26 EBITDA was in line at INR22.5b. Reported PAT was INR3.7b (adjusted for minority interests), aided by a deferred tax asset created of INR3.7b and other income coming in higher than our estimate. JSWE reported an adjusted loss of INR1.1b (vs. our est. of INR0.26b profit) after adjusting for minority interest and excluding the effect of the deferred tax asset. FY26 Revenue/EBITDA/APAT stood at INR189/101/10.7b (+61%/+93%/-41% YoY).

* Key things we liked:

1) power demand rebounded strongly, with FY27 YTD growth of ~4.6% YoY

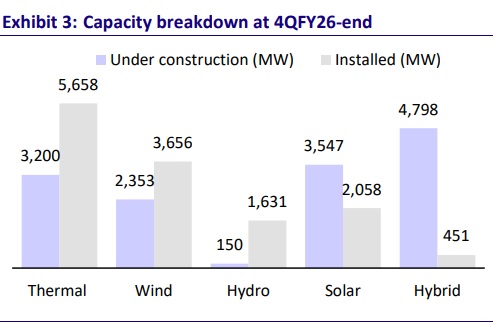

2) management guided a 3GW renewable energy (RE) capacity addition in FY27, evenly split between 1HFY27 and 2HFY27

3) FY27 capex guidance remains robust at INR200b, with INR40-50b guided for thermal and pump storage project (PSP) and the balance toward RE and battery energy storage systems (BESS),

4) acquisition of the remaining 26% stake in KSK Mahanadi is expected by end-2QFY27, which should reduce minority interest outflows

5) despite lower tariffs at KSK in FY27, management guided EBITDA to remain above INR27b, supported by low-cost fuel and logistics costs due to the proximity to coal mines.

* Key monitorables include:

1) RE commissioning, which was below expectations, with only 243MW added in 2HFY26 vs. guidance of 1.5GW

2) standalone revenue, which declined ~32% YoY during the quarter

3) new DSM regulations, which could hit revenue by ~1.5-2.0% (though the impact may reduce if the project grouping is permitted

* Valuation and view: We reiterate our BUY rating with a TP of INR640, valuing the company’s core renewable business at 12x FY28E EBITDA and its thermal business at 9x Dec’27E EBITDA.

EBITDA in line; APAT below expectations

Financial Performance

* JSW Energy reported a revenue of INR45b (+41% YoY, +10% QoQ) in 4QFY26, missing our estimates by 24%.

* EBITDA came in line with our estimate at INR22.5b (+87% YoY, +11% QoQ).

* Reported PAT was INR3.7b (adjusted for minority interests), aided by a deferred tax asset created of INR3.7b during the quarter on account of carryforward losses and unabsorbed depreciation at Utkal and KSK Mahanadi.

* The company reported an adjusted loss of INR1.1b after adjusting for minority interest and excluding the effect of the deferred tax asset.

* The Board declared a dividend of INR2/share.

Operational Performance

* Power sales volume for 4QFY26 increased 48% YoY to 11.7BUs (RE generation rose 68% YoY while thermal generation increased 43%).

* Share of PPA-backed generation in total generation was 73% vs. 87% in 4QFY25.

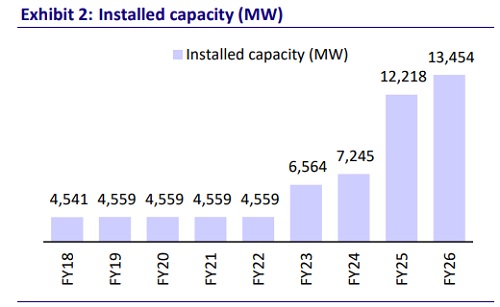

* Capacity addition for FY26 stands at 2.6GW post commissioning of ~118MW of organic renewable capacity during 4QFY26.

* Net Debt/Equity was 2.1x, and operational Net Debt/EBITDA stood at 5.2x.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412