Neutral Oberoi Realty Ltd for the Target Rs. 1,850 by Motilal Oswal Financial Services Ltd

Scaling up well Strong business development improves growth visibility

In FY26, Oberoi Realty (OBER) added multiple new residential projects across various micro-markets of MMR, including redevelopment agreements in Aram Nagar (Versova; 1.7msf), Peddar Road (0.14msf), Malabar Hill (51,000sqft), and Nepean Sea (0.12msf). Moreover, the company emerged as the highest bidder for RLDA’s Bandra East land parcel, which has a development potential of ~2msf and is likely to be a commercial development. This, along with diversification efforts, has improved the company’s medium-term growth visibility

Pre-sales growth expected to improve going forward

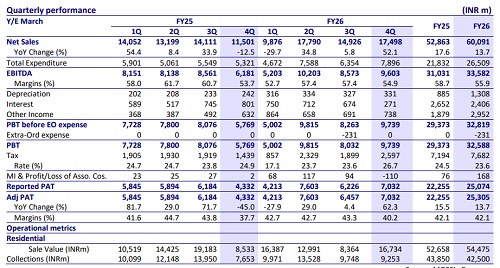

In 4QFY26, OBER’s pre-sales grew 96% YoY to INR17b, driven by strong traction in Elysian, Goregaon, which recorded bookings worth INR8.4b (~50% of the quarterly pre-sales), and Sky City, Borivali, which clocked INR3.2b in pre-sales. However, overall pre-sales growth remained muted at 3% YoY, reaching INR55b. For FY27, the company has a healthy launch pipeline including the NCR project, Oceanic (Carter Road), Fairview (Malabar Hill), and a new tower each at Forestville and Jardin in 1HFY27. Other projects, such as Aadarsh Nagar, Enigma commercial (strate sale), and the Peddar Road redevelopment, are expected to be launched after FY27. We bake in a 16% CAGR in pre-sales to INR73b over FY26-28E

Ramping up the annuity and hospitality portfolios

* Lease rental income increased 18% YoY to INR3.2b in 4QFY26. Occupancy remained healthy across key assets, with Commerz II achieving full occupancy, while Commerz III and Sky City Mall witnessed improvement in occupancy levels during the quarter. Overall, in FY26, revenue from rent grew 37% YoY to INR11.9b, with an EBITDA margin of 91%. Given the higher occupancy at Commerz III, Sky City Mall, and rental escalations, we expect a 9% annuity income CAGR over FY26-28, reaching INR13.5b.

* Hospitality revenue stood at INR548m in 4QFY26, rising 3% YoY, while RevPAR increased 3% YoY to ~INR14,354 despite marginal moderation in occupancy to 77%. In FY26, the hospitality segment revenue increased 3% YoY to ~INR2b. The Ritz Carlton (Three Sixty West) and Marriott Hotel in Borivali are expected to be operational in the next two years. Hence, we expect 56% CAGR in hospitality revenue over FY26-28, reaching INR4.8b.

Valuation and view

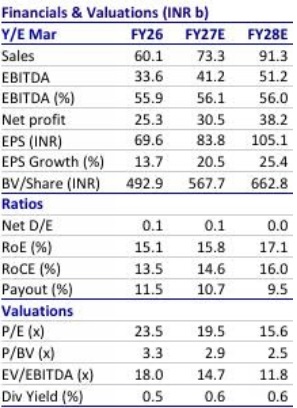

* OBER’s pre-sales are expected to improve in the next two years, supported by a strong launch pipeline and a meaningful ramp-up in BD activities, which have improved medium-term growth visibility. The annuity and hospitality segments are scaling well and, with more additions already planned, we expect profitability to record strong growth in the coming years. Further, the company maintains one of the strongest balance sheets among peers, lending significant financial comfort.

* We value the residential business on a NAV basis and assign a 25% premium to capture the increased focus on BD (our calculations suggest that the company can command 50% NAV premium). Further, we value the annuity portfolio at 7.5-8% cap rate and the hospitality business at 18x EV/EBITDA on FY28E.

* We have a Neutral rating with an SoTP-based TP of Rs1,850.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412