Buy Canara Bank Ltd for the Target Rs. 160 by Motilal Oswal Financial Services Ltd

Earnings in line; NIM guidance tepid at 2.5-2.6% ECL transition impact at ~INR100b/up to 100bp impact on CRAR

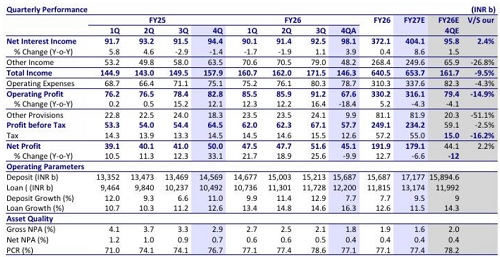

* Canara Bank (CBK) posted a 4QFY26 standalone PAT of INR45b (10% YoY dip, largely in line) amid muted other income, offset by lower provisions.

* NII grew 3.9% YoY/6% QoQ to INR98b (broadly in line). Its margin improved 9bp QoQ to 2.54% vs. our est. of 2.44% (2.45% in 3QFY26). The bank has reduced its NIM guidance to 2.5-2.6%, vs. 2.75–2.8% in FY26.

* The loan book grew 16% YoY/4% QoQ to INR12.2t. The bank has guided advances growth of 11-12%, while remaining confident of outperforming the stated guidance. Deposits grew 7.7% YoY/3% QoQ to INR15.7t.

* Slippages increased to INR28b (INR18.9b in 3QFY26), amid 4Q seasonality. The GNPA/NNPA ratios improved 24bp/2bp QoQ to 1.84%/0.43% respectively, led by higher write-offs. The PCR was down 148bp QoQ and moderated to 77.1%. The bank has stated that its ECL transition impact was INR100b and the impact on CRAR was up to 100bp.

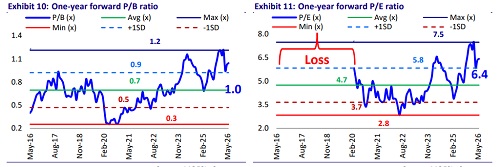

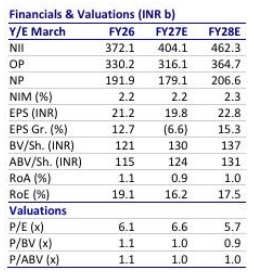

* We cut our earnings by 6%/4% for FY27E/28E and estimate CBK to deliver an FY27E RoA/RoE of 0.91%/16.2%. Reiterate BUY with a revised TP of INR160 (based on 1.2x Sep’27E ABV+ INR12 for subs).

Business growth steady; Asset quality ratio improves

* CBK’s 4Q PAT declined 10% YoY/13% QoQ to INR45b (largely in line) amid tepid other income partly offset by lower provisions. NII grew 4% YoY/ 6% QoQ to INR98b (largely inline).

* Margins improved 9bp QoQ to 2.54% vs. our est. of 2.44%; the bank has reduced its NIMs guidance to 2.5-2.6% in FY27E vs. 2.75-2.85% in FY26.

* Other income declined 24% YoY/39% QoQ to INR48.2b (27% lower than MOFSLe), amid treasure loss in 4Q, while 3Q had one-off gains due to the listing of subsidiaries (Canara HSBC Life and Canara Robeco). Total revenue thus declined 7% YoY/15% QoQ (10% miss).

* Operating expenses declined 2% QoQ (up 5% YoY) to INR78.7b (4% lower), aided by a decline in employee expenses (likely due to reduction in AS-15 provisions). Thus, the C/I ratio increased to 53.8% in 4QFY26 (up 699bp QoQ). PPoP thus declined 18% YoY/ 26% QoQ to INR 67.6b (15% miss). Provisions came in at INR9.9b (51% lower vs. MOFSLe, down 58.9% QoQ).

* The loan book jumped 16.3% YoY/4% QoQ, led by robust growth in the retail segment at ~33% YoY/8.6% QoQ, while the gold portfolio contributed to most of the growth with 33-34% YoY growth and 20% of the portfolio.

* Deposits grew 7.7% YoY/3.1% QoQ to INR15.7t. CASA deposits grew 3.3% YoY/4% QoQ. The CASA ratio stood at 29.8%, while the CD ratio increased to 77.8% (vs. 77.1% in 3QFY26).

* Slippages increased to INR28b (INR18.9b in 3QFY26) amid 4Q seasonality. GNPA/NNPA ratio improved by 24bp/2bp QoQ to 1.84%/0.43% respectively, led by higher write-offs. The PCR was down 148bp QoQ and moderated to 77.1%. The bank has stated that its ECL transition impact was INR100b and the impact on CRAR was up to 100bp.

* Reported credit cost stood at 0.59%. SMA book (INR50m and above) decreased to 0.49% in 4QFY26 from 0.69% in 3QFY26. Management guided one large ticket recovery in 1QFY27.

Valuation and view

CBK reported a mixed quarter with healthy margins and controlled opex and provisions; however, treasury loss and moderation in NIM guidance have resulted in a slight cut in our earnings. Loan growth was steady, driven by retail (gold loans), thus supporting yields. CoF declined by 9bp as the bank has increased its focus towards retail deposits (cheaper vs. bulk, despite the deposit rate hike in Dec’25). CBK endeavors to perform better than its loan growth guidance of 11-12%. Asset quality for the bank continues to be steady, while slippages saw some seasonality in 4Q. The bank has stated that its ECL transition impact was INR100b and the impact on CRAR was up to 100bp, while CBK maintains its guidance of 1% RoA despite the transition impact. We cut our earnings by 6%/4% for FY27E/FY28E, primarily due to lower NIM and other income assumptions, partly offset by a reduction in provisioning estimates. We expect CBK to deliver an RoA/RoE of 0.91%/16.2% in FY27E. We reiterate our BUY rating with a revised TP of INR160 (based on 1.2x Sep’27E ABV + INR12 for subsidiaries).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412