Buy Hindalco Ltd For Target Rs. 770 by Motilal Oswal Financial Services Ltd

Capacity expansion to drive next leg of growth; HNDL wellplaced to capitalize

We attended Hindalco’s (HNDL) Investor Day held on April 01, 2025. Below are the key highlights from the meeting:

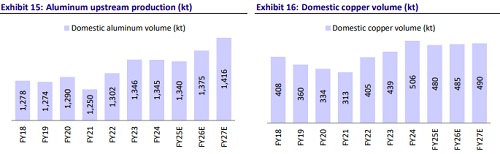

* HNDL and its subsidiary, Novelis, are investing ~USD10b in growth projects to significantly boost capacities. In India, HNDL is expanding its aluminum upstream (Aditya smelter 180 KT, alumina refinery 850 KT), downstream (FRP-170 KT, battery enclosures etc), and copper capacities (smelter 300 KT and recycling 50KT), with a total of USD5.2b currently under execution. Novelis is adding ~800KT globally, including USD4.1b in the Bay Minette facility (600 KT) and debottlenecking (175 KT), targeting completion by FY27 to meet rising demand in beverage packaging and automotive sectors. The company is also aggressively expanding its VAP portfolios to capitalize on emerging trends.

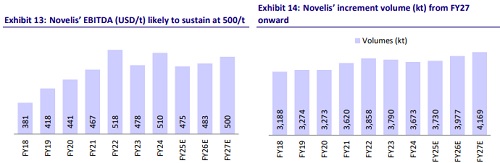

* Novelis is targeting adj. EBITDA of USD600/t in the long run, largely driven by operating leverage and an increase in recycled content to 75%. Margin expansions are expected to begin once the Bay Minette capacity ramps up. HNDL’s Indian business aims to enhance EBITDA through scale, efficiency, and recycling. Following the ramp-up, India’s EBITDA is expected to increase by USD200/t for aluminum upstream, USD100/t for downstream, USD120/t for copper, and USD50/t for specialty alumina over FY24, primarily driven by resource security and premiumization. Additionally, HNDL targets an energy mix of 70% captive coal and 30% RE by FY33.

* Industry demand is expected to remain strong, with India’s aluminum consumption expected to double to 11,373 KT by FY35 (8% CAGR) and copper demand to grow 2.5x to 2,540 KT, driven by high adoption in EVs, construction, and energy sectors. Globally, demand for Flat Rolled Products (FRP) is projected to post a 4% CAGR, reaching 37.7 MT by 2029, led by beverage packaging and automotive applications. Prices are expected to remain resilient, supported by robust demand (electrification, Paris Agreement), China’s 45 MTPA supply cap, and escalating costs, ensuring favorable LME price strength for HNDL’s operations.

Valuation and view: Reiterate BUY

* HNDL’s Indian operations are net debt-free, and the consolidated net debt/EBITDA stood at 1.33x as of Dec’24 vs. 1.43x in Dec’23. The announced/ongoing expansion is set to position HNDL as the global leader. Novelis has already secured long-term contracts from marquee customers for Bay Minette, ensuring future revenue visibility. With a larger scale and operational efficiency, margins are expected to expand over the medium to long term. We reiterate our BUY rating on HNDL with SOTP-based valuation, arriving at a TP of INR770.

* Key risks: 1) Delays in capex to put pressure on cash flow; 2) Rise in scrap prices impacting margins; 3) US tariffs lead to demand and supply disruptions

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412