Neutral NSDL Ltd for the Target Rs.1,000by Motilal Oswal Financial Services Ltd

Strong growth led by banking services segment

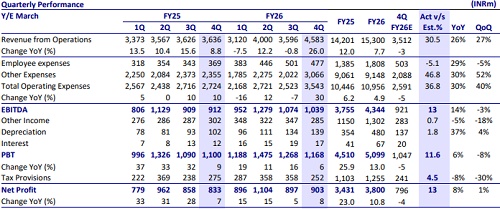

* NSDL’s operating revenue rose by 26% YoY/27% QoQ to INR4.6b (31% beat), primarily driven by strong growth of 49% YoY/56% QoQ in the Banking Services segment. For FY26, total revenue grew by 8% YoY to INR15.3b.

* Operating expenses rose 30%YoY/40% QOQ to INR3.5b. Employee costs grew 29% YoY but declined 5% QoQ, while other expenses rose 30% YoY/52% QoQ. EBITDA rose 14% YoY but declined 3% QoQ to INR1b (13% beat), resulting in EBITDA margin of 22.7% vs. 25.1% in 4QFY25 and 29.9% in 3QFY26. For FY26, EBITDA grew 16% YoY to INR4.3b.

* 4Q PAT rose 8% YoY but remained flat QoQ at ~INR903m (13% beat) due to higher-than-expected revenue growth. PAT margins came in at 19.7% vs. 22.9% in 4QFY25 and 24.9% in 3QFY26. For FY26, PAT grew 11% YoY to INR3.8b.

* Employee additions peaked in FY26; going forward, hiring is expected to moderate with a sharper focus on automation and productivity, while tech cost run-rate is likely to remain broadly stable in the near term, with moderation expected from FY28 onward.

* We have raised our earnings estimates for FY27/FY28 by 4%/3% to factor in higher banking revenue and lower cost growth. We expect NSDL to post a revenue/EBITDA/PAT CAGR of 11%/13%/15% over FY26-28E. We reiterate our Neutral rating on the stock with a one-year TP of INR1,000 (premised on a P/E multiple of 40x on FY28E earnings).

Share of banking mix in total revenue improves

* On the revenue front, banking services income grew 49% YoY/56% QoQ to INR2.7b, with share in revenue mix rising to 58% from 49% in 4QFY25/48% in 3QFY26, while depository revenue remained flat YoY/QoQ to INR1.7b with share in mix at 37% vs. 46% in 4QFY25.

* Within depository revenue, the share of recurring income rose to 57.2% from 42.8% in 4QFY25/54.3% in 3QFY26 at INR976m, up 52% YoY/6% QoQ.

* In the non-recurring portion, corporate action fee (incl. IPO) fell 52% YoY/ 37% QoQ (due to lower corporate actions in 4Q), e-voting charges were down 9% YoY/flat QoQ, settlement charges largely were flat YoY/down 7% QoQ, pledge fee rose 13.5% YoY/8.8% QoQ, and other transaction charges were down 20% YoY/up 27% QoQ.

* Under the subsidiaries, the NPBL segment revenue jumped 49% YoY/56% QoQ to INR2.7b, led by strong focus on high-quality account sourcing, leading to CASA float crossing INR5b and transactions crossing 4.3m, and strong growth in UPI-based services with volumes growing 6.3x YoY, which contributed to fee income growth.

* NDML revenue rose 14% YoY/8% QoQ in 4Q to INR211m. The insurance repository business contributed ~INR55-60m to the NDML’s revenue.

* Other income declined 5% YoY/18% QoQ (in line) to INR285m, led by MTM impact.

* Total expenses rose 30% YoY/40% QoQ to INR3.5b, with CIR at 77.3% vs. 74.9% in 4QFY25 and 70.1% in 3QFY26. Employee costs for the quarter rose 29% YoY but declined 5% QoQ to INR477m, while other expenses rose 30% YoY/52% QoQ to INR3.1b.

* While employee hiring is expected to moderate going forward with a sharper focus on automation and productivity improvements—leading to moderation in employee costs, other expenses are expected to remain broadly stable at the current levels.

* Total demat accounts stood at 44.4m vs. 39.5m in 4QFY25, with share rising to 15.4% from 9% in 4QFY25. Net additions during the quarter were at 1.2m vs. 0.7m in 4QFY25.

Key takeaways from the management commentary

* Continued onboarding of fintech brokers, including a Pune-based player that started contributing toward 4Q end, alongside a large DP migration from a competitor, is expected to support incremental account additions going forward.

* Under NDML, the insurance repository business is being demerged into a separate entity in line with IRDAI regulations.

* Launched the Women Demat Plan in Apr’26, offering a three-year waiver on settlement fees for new women demat accounts, expected to aid incremental sourcing; a similar earlier initiative (Yuva Plan) contributed ~21% of incremental additions.

Valuation and view

* With the share of recurring fees rising to ~50.4% of FY26 depository income, imparting greater stability to the annuity-led business model, and increasing contribution from banking services, alongside controlled cost growth, NSDL is well positioned to benefit from operating leverage, supporting improvement in profitability. Steady momentum in demat account additions and successful onboarding of new fintech partners remain key monitorables for future growth.

* We have raised our earnings estimates for FY27/FY28 by 4%/3% to factor in higher banking revenue and lower cost growth. We expect NSDL to post a revenue/EBITDA/PAT CAGR of 11%/13%/15% over FY26-28E.

* We reiterate our Neutral rating on the stock with a one-year TP of INR1,000 (premised on a P/E multiple of 40x on FY28E earnings).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412