Neutral UPL Ltd for the Target Rs. 600 by Motilal Oswal Financial Services Ltd

Stong 4QFY26; industry headwinds appear to be normalizing Operating performance above our estimates

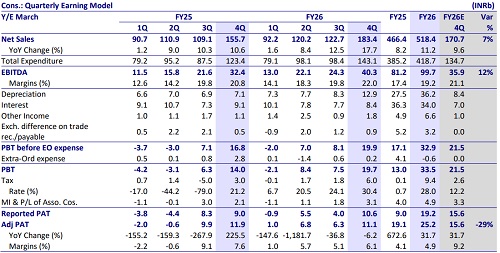

* UPL Ltd (UPLL) posted a strong 4Q operating performance, with EBITDA growing 24% YoY to INR40.3b. This was led by a strong EBITDA growth in UPL Corp (14%) and Advanta (31%).

* We believe the industry has largely moved past the prolonged destocking cycle, with demand trends and channel inventories gradually normalizing across major markets, leading to a steady recovery in volume growth across key regions. Backed by UPLL’s improving innovation pipeline, increasing contribution from differentiated and sustainable solutions, and continued deleveraging efforts, we expect UPLL to sustain profitable growth momentum into FY27.

* However, we cut our FY27/FY28 earnings estimates by 15%/13%, factoring in a higher effective tax rate in line with management guidance, along with increase in depreciation and finance costs. We reiterate our Neutral rating on the stock with a TP of INR600

Volume-led growth offsets pricing pressure

* UPLL reported revenue of INR183.4b (est. INR170.7b) in 4QFY26, up 18% YoY (growth led by overall volumes, partially offset by pricing pressure). EBITDA stood at INR40.3b (est INR35.9b), up 24% YoY. EBITDA margin stood at 22% (up 120bp). Adj PAT came at INR11.1b (est. INR15.6b) in 4QFY26, down 6% YoY (PAT is adjusted for exchange difference, extraordinary items such as VAT disallowance, and restructuring cost).

* For FY26, the company’s revenue/EBITDA/adj. PAT grew 11%/23%/32% to INR518b/INR99.7b/INR25.2b.

* Net debt stood at INR153b as of Mar’26 vs INR173b as of Mar’25 (repayment of USD850m in FY26).

* India’s revenue declined 9% YoY to INR12.7b, attributed to product discontinuation, which was partially offset by strong growth in the seeds business. North America’s revenue grew 23% YoY to INR33.2b, driven mainly by strong herbicide volumes. LATAM’srevenue grew 21% to INR61.3b, led by robust crop protection volumes in Brazil, particularly herbicides, along with strong field corn performance in Argentina. The European business grew 19% YoY to INR37.1b, driven largely by fungicide and NPP volumes across Mediterranean markets, supported by favorable FX movement, while the RoW business grew 19% to INR39b.

* Advanta’s revenue increased 23% YoY to INR22b, driven by strong demand for field corn (India, Latin America, Thailand, Indonesia, and Argentina) and sunflower (Argentina). In addition, post-harvest, the business witnessed growth in the US, Chile, and Africa. UPLL’s SAS revenue decline 10% YoY in 4QFY26, driven by a 10% decline in volumes. SUPERFORM’s revenue grew 10% YoY to INR22b.

* For FY26, Revenue/EBITDA /Adj.PAT grew 11%/23%/32% to INR518b/INR99.7b/INR25.2b (volume growth: 8%, price down: 3%, forex up: 6%).

* Net working capital days stood at 138 in FY26 vs. 113 days in FY25. Net debt stood at INR153b as of Mar’26 vs INR173b as of Mar’25 (repayment of USD850m in FY26). CFO declined 14% in FY26 to INR86.7b.

Valuation and view

* UPLL delivered a strong close to FY26, with broad-based growth across geographies and platforms, while pricing pressure in the global crop protection industry persists due to excess capacities in China and competitive market dynamics; we believe the industry has now largely stabilized, with channel inventories normalizing and volume recovery gradually improving across key regions.

* Although pricing recovery across the global crop protection industry remains limited, we believe UPLL’s increasing focus on differentiated products, sustainable agriculture solutions, specialty chemicals, and better capacity utilization mitigates the earnings volatility.

* However, we cut our FY27/FY28 earnings estimates by 15%/13%, factoring in a higher effective tax rate in line with management guidance, along with increase in depreciation and finance costs. We reiterate our Neutral rating on the stock with a TP of INR600

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Buy Raymond Lifestyle Ltd for the Target Rs 880 by Motilal Oswal Financial Services Ltd