Buy CreditAccess Grameen Ltd for the Target Rs.1,760 by Motilal Oswal Financial Services Ltd

Healthy quarter; operating performance continues to improve

NIM expands 30bp QoQ; asset quality improves and credit costs decline

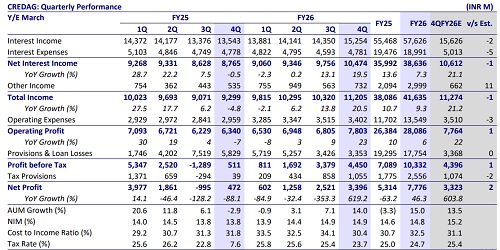

* CREDAG’s 4QFY26 PAT stood at INR3.4b (in line). FY26 PAT grew 46% YoY to INR7.8b. 4Q NII grew 19% YoY to ~INR10.5b (in line). 4Q PPOP rose ~23% YoY to INR7.8b (in line). FY26 PPoP grew 6% YoY to INR28b. Opex was up ~15% YoY at INR3.4b (in line). Cost-income ratio declined ~370bp QoQ to 30.4% (PQ: ~34% and PY: ~32%).

* Disbursements rose ~28% YoY/44% QoQ to ~INR83b. AUM grew 11% QoQ and ~14% YoY to ~INR296b. Management guided for AUM growth of 20- 25% in FY27, supported by steady growth in core MFI and faster expansion in non-MFI products. The company guided that its core group loan (GL) portfolio is expected to grow at ~10-12%, while most of the incremental growth is expected to come from non-MFI and individual finance products.

* Reported yields improved 20bp QoQ to 21.2% and CoF declined ~20bp QoQ to 9.2%. Reported NIM rose ~30bp QoQ to ~14.2%. Management indicated that the cost of funds has largely stabilized and should remain broadly range-bound, with the possibility of an uptick going forward. Consequently, the company expects NIMs in the range of ~12.8-13.2% in FY27. We model NIM (calc.) of 14.6%/14.5% in FY27/FY28 (vs. ~14.8% in FY26).

* Management noted that asset quality trends have largely stabilized with PAR accretion trends, collection efficiency, and PAR 1-90 metrics reverting closer to pre-crisis levels. Management expects credit costs of 3-4% in FY27. We model credit costs of 3.6%/3.5% in FY27E/FY28E (vs. 6.5% in FY26).

* CREDAG delivered a strong operational performance with improving borrower quality, normalization in collection trends, and continued traction in scaling its retail finance franchise. The company’s deep rural presence and ability to graduate existing MFI customers into higher-ticket individual loans provide strong visibility on sustainable growth and diversification.

* We raise our FY27/FY28 EPS estimates by 4% each to factor in higher AUM growth. We estimate a CAGR of 21%/55% in AUM/PAT over FY26-28E, leading to RoA/RoE of ~4.4%/18% in FY28. CREDAG trades at 2.6x FY27E P/BV and given its superior execution, we expect its premium valuations over its MFI peers to sustain. Reiterate our BUY rating with a revised TP of INR1,760 (based on 2.5x Mar’28E P/BV).

Valuation and view

* CREDAG has successfully navigated a period of industry-wide challenges, demonstrating remarkable resilience, and has reverted to its normalized operational efficiency. New stress formation has normalized, supported by robust internal processes, stable PAR bucket roll-forward rates, and improvement in the PAR 15+ accretion rate.

* With structural levers such as branch network expansion and strengthening collection efficiency across key geographies firmly in motion, it is wellpositioned to accelerate loan growth and profitability. CREDAG trades at 2.6x FY27E P/BV. With a strong capital position (Tier-1 of ~24%), it will embark on a strong loan growth trajectory in FY27 driven by improving asset quality trends. Reiterate our BUY rating with a revised TP of INR1,760 (based on 2.5x Mar’28E P/BV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412