Buy Tata Consumer Products Ltd for the Target Rs. 1,450 by Motilal Oswal Financial Services Ltd

Growth momentum picks up with margin expansion Operating performance beats estimates

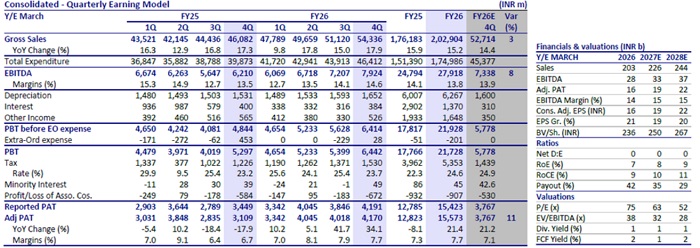

* Tata Consumer Products (TATACONS) reported ~34% YoY growth in EBIT in 4QFY26, led by strong 88% YoY growth in India branded business EBIT, which was supported by operating leverage (decrease in other expense as a percentage of sales by 230bp). International beverages business EBIT declined 4% YoY and non-branded business EBIT declined 33% YoY. In 4Q, salt/tea reported a volume growth of 13%/4% YoY, and Sampann grew 69% YoY.

* We expect TATACONS to maintain a healthy overall growth momentum going forward, with the India beverages business expected to witness a gradual margin recovery, aided by stable tea prices. The India foods segment is expected to continue delivering strong growth, led by Tata Sampann, expansion in the salt portfolio, and premium offerings. International business profitability is also likely to improve with the normalization of coffee costs and continued scale-up in RTD beverages. Capital Foods, Organic India, and health & wellness categories are expected to further support revenue growth and margin expansion over the medium term.

* We largely maintain our FY27/FY28 earnings estimates and reiterate BUY with an SoTP-based TP of INR1,450.

Performance driven by traction in the branded and growth portfolios

* TATACONS reported revenue of INR54.3b (est. in line), rising 18% YoY. EBITDA margin expanded 110bp YoY to 14.6% (est. 13.9%), led by a decrease in other expenses as a % of sales by 230bp at 18.7% v/s 21% in 4QFY25. EBITDA grew 28% YoY to INR7.9b (est. INR7.3b). Adj. PAT rose 34% to INR4.2b (est. INR3.8b).

* Indian branded business grew by 13% YoY to INR33b, led by revenue growth of 4%/24% YoY in Indian branded beverage business/India food business to INR16.1b/INR17.1b. EBIT grew by 88% YoY to INR4.5b.

* RTD segment (NourishCo) revenue rose ~23% YoY to ~INR2.6b, while volumes recorded a moderate growth of 23%. Growth businesses (including RTD, Capital Foods, and Organic India) reported strong growth of 33% YoY, led by robust growth in Tata Sampann (up 69%). Organic India and Capital Foods grew 8% YoY on a combined basis.

* International branded beverages revenue grew 19% YoY to ~INR14.2b, EBIT grew 3% YoY to INR1.7b, and EBIT margins contracted ~250bp YoY to 10.7%. Non-branded business revenue increased 43% YoY to ~INR7.1b, while EBIT declined 33% YoY to INR745m.

* For the full year, revenue/EBITDA/Adj. PAT grew 15%/13%/21% to INR202b/INR27.9b/INR15.6b.

* At Mar’26, net cash stood at INR29.8b vs INR INR12.6b. CFO grew 18% YoY to INR24.2b.

Valuation and view

* We expect TATACONS’ growth momentum to further strengthen, driven by improving GTM execution, rising traction in quick commerce/e-commerce, and continued scale-up in high-growth businesses such as Tata Sampann, RTD beverages, Capital Foods, and Organic India.

* The company’s operating margin is expected to expand over the years with easing coffee costs, benign tea prices, portfolio premiumization, innovation-led launches, and increasing contribution from higher-margin growth businesses and health & wellness categories.

* We expect TATACONS to clock a CAGR of 10%/15%/19% in revenue/EBITDA/PAT during FY26-28. Reiterate BUY with an SoTP-based TP of INR1,450.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)