Neutral Lupin Ltd for the Target Rs.2,520 by Motilal Oswal Financial Services Ltd

Broad-based growth drives earnings; strong finish in FY26 Earnings to be constrained for FY27/FY28; reiterate Neutral

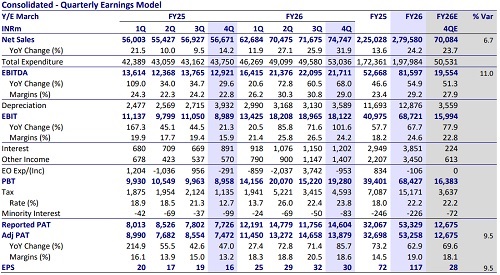

* Lupin (LPC) delivered another quarter of strong performance with a 7%/11%/10% beat on revenue/EBITDA/PAT for the quarter. Increased traction in niche products in the US, coupled with broad-based growth across key geographies, led to the growth momentum in 4QFY26 as well.

* Effectively, FY26 would be the third straight year of strong growth in earnings (380%, 73%, and 63% YoY for FY24, FY25, and FY26, respectively).

* The US surpassed USD1.3b in sales, the highest annual sales ever, due to limited competition products like g-Tolvaptan, g-Mirabegron, and g-Risperdal Consta.

* LPC outperformed the domestic formulation prescription (Rx) market by 1.1x, with cardiology, respiratory, and pain growing much higher than the industry.

* LPC exhibited strong execution in LATAM as well as ROW markets in FY26.

* We raise our earnings estimate by 4%/3% for FY27/FY28, factoring in

1) better-than-industry growth in Rx and emerging markets

2) the addition of sales from Visufarma

3) scale-up of the biosimilar business. We value LPC at 22x 12M forward earnings to arrive at our TP of INR2,520.

* While LPC ended FY26 on a strong note, we estimate earnings to remain stable over FY26-28 due to competition expected in certain niche products in the US market. The current valuation provides limited upside. Hence, we reiterate our Neutral rating on the stock.

LPC ends FY26 on a strong note with healthy margin-led growth

* LPC's 4QFY26 revenue grew 31.9% YoY to INR74.7b. (our est. INR70.1b).

* Gross Margin (GM) expanded 500bp YoY to 75.2%.

* EBITDA margin expanded 620bp YoY to 29% (our est: 27.9%), largely due to better GM.

* As a result, EBITDA grew 68% YoY to INR21.7b (vs our est: INR19.6b).

* Adj. PAT grew 85.7% YoY to INR13.9b (our est: INR12.7b).

* For FY26, Revenue/EBITDA/PAT grew 24%/51%/70% YoY.

Broad-based growth across geographies

* US sales grew 57% YoY to INR34b (up 48% YoY in CC to USD371m; 46% of sales).

* Domestic formulation (DF) sales grew 11.5% YoY to INR19.1b (26% of sales).

* Other developed market sales grew 7.1% YoY to INR8.5b (11% of sales).

* Emerging market sales grew 49.2% YoY to INR 9.9b (13% of sales).

* API sales increased 7.6% YoY to INR2.5b (4% of sales).

* LPC received three ANDA approvals and launched three products in 4QFY26.

* Launched three brands across therapies in India during the quarter.

* R&D for the 4Q/FY26 was INR5.9b/INR20.6b (8%/7.5%).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412