Buy Piramal Pharma Ltd for the Target Rs.190 by Motilal Oswal Financial Services Ltd

Operationally below est.; ends FY26 on a weak note

FY27 recovery depends on CDMO conversion and CHG scale-up

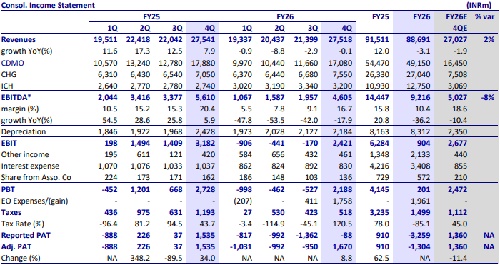

* Piramal Pharma (PIRPHARM) posted in-line revenue for 4QFY26. The EBITDA was lower than expected (an 8% miss), primarily due to a product mix change. A lower tax rate led to higher-than-expected earnings in 4Q.

* The deceleration in the CDMO segment has been lower in 4QFY26 vs. 2Q/3Q. Ex-inventory destocking for a certain on-patent molecule, the CDMO segment has experienced growth in 4QFY26/FY26. Notably, PIRPHARM has garnered USD64m in sales in the ADC segment for FY26.

* Complex hospital generics (CHG) sales growth has improved YoY in 4Q. In addition to maintaining leadership in Inhalation Anesthesia (IA) products, PIRPHARM has initiated manufacturing from a lower-cost Digwal facility for ROW markets, thus improving profitability to some extent going forward.

* In addition to strong traction in the online channel for the India consumer product (ICP) segment, PIRPHARM is widening its presence through the offline channel as well.

* We cut our PAT estimates for FY27/FY28 by 52%/39%, factoring in 1) increased opex due to the Middle East crisis, 2) higher interest outgo on account of increased debt (for acquisition and working capital needs), and 3) improved outlook for the CDMO segment.

* We value PIRPHARM on an SoTP basis (19x EV/EBITDA for the CDMO segment, 11x EV/EBITDA for CHG and 13x EV/EBITDA for ICP) to arrive at our TP of INR190. FY26 was a year of weak performance due to inventory destocking for a product by a customer and intensified competition in the CHG segment. However, we expect PIRPHARM to deliver better growth in FY27 with a revival in biotech funding and adding products/lowering the cost of manufacturing in the CHG segment. Reiterate BUY.

Margins contract; lower tax supports earnings beat despite flat revenue

* PIRPHARM’s revenues remained stable YoY to INR27.5b for the quarter (our est: INR27b)

* Gross margin contracted 370bp YoY to 61.6%. ? EBITDA margin contracted at 370bp YoY to 16.7%, largely due to a dip in gross margin.

* EBITDA declined 18% YoY to INR4.6b (our est: INR5b).

* An exceptional gain of INR1.8b, mainly due to the annual assessment of an impairment charge of INR1.8b, was recognized in accordance with the principles of IND AS 36 Impairment of Assets. This gain is with respect to a certain intangible asset under development in the company.

* Adj. PAT stood at INR1.7b vs. our estimate of INR1.4b, driven by comparatively lower taxes for the quarter.

* For FY26, PIRPHARM posted a 3%/36% decline in revenue/EBITDA to INR88.7b/INR9.2b. Adj. Loss for FY26 was INR1.3b vs. PAT of INR910m in FY25.

CHG and ICH growth offsets CDMO weakness; mix shifts toward non-CDMO segments on a YoY basis

* The CDMO segment’s (62% of total sales) revenue dipped 4% YoY to INR17b.

* The Complex Hospital Generics segment’s (CHG; 27% of total sales) revenue grew 7% YoY to INR7.6b.

* The India Consumer Healthcare segment’s (ICH; 11% of total sales) revenue grew 17% YoY to INR3.2b.

Highlights from the management commentary

* Management guided for early to mid-teens revenue growth in FY27, with EBITDA expected to grow faster and PAT to grow meaningfully. This guidance excludes revival in business from a patent product, which was subject to inventory destocking in FY26.

* Revenue is expected to be 2H-weighted, with growth building progressively from 2Q onwards.

* FY27 capex is expected at ~USD120-135m (vs ~USD94m in FY26, below USD100- 125m guidance), with spillover from FY26; largely directed towards Lexington expansion, excluding spend on Kenalog or similar acquisitions.

* Net debt/EBITDA is expected to remain range-bound at ~3.6x through FY27, with interim fluctuations driven by profitability and capex.

* The CDMO growth outlook remains supported (ex key product) by improved biotech funding in 2H, higher RFP activity, increased order bookings, and better win rates, aiding normalization.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412