Neutral Aditya Birla Lifestyle Brands Ltd for the Target Rs120 by Motilal Oswal Financial Services Ltd

Emerging brands drive growth; Lifestyle retail LTL modest

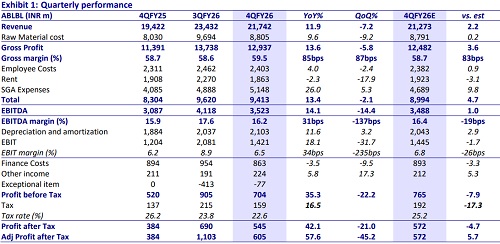

* ABLBL reported 12% YoY revenue growth (vs. ~15% for Arvind Fashion), supported by robust ~18% YoY growth in Emerging brands. Lifestyle brands' revenue grew ~11% YoY, boosted by certain one-off PLI benefits, even as the retail LTL remained modest at ~4%.

* Improvement in gross margin (up ~85bp YoY) was partly offset by higher other expenses (up 26% YoY), which drove an in-line ~14% YoY EBITDA growth and ~30bp YoY margin expansion to 16.2%.

* Management is targeting ~8-9% annual network expansion and ~8% retail LTL on a sustainable basis. Further, it expects Van Heusen Innerwear to achieve break-even in 3QFY27 and sustained profitability from FY28 onwards.

* We fine-tune our estimates for FY27-28E EBITDA and build in a CAGR of 9%/11%/24% in revenue/EBITDA/adj. PAT over FY26-28E.

* We reiterate our Neutral rating with a revised TP of INR120, premised on ~20x FY28E pre-Ind AS EV/EBITDA

Robust growth and improved profitability in emerging brands

* Revenue at INR21.7b grew 12% YoY (vs. our estimate of 10% YoY), though weaker than ~15% YoY reported by Arvind Fashions.

* Lifestyle Brands’ revenue grew 11% YoY, driven by a recovery in e-com and departmental stores, even as retail LTL was modest at ~4%.

* Emerging brands delivered an 18% YoY growth, driven by a 30% YoY growth in Reebok.

* The company’s presence expanded to 3,348 brand stores (~33 net store additions in 4Q and ~95 net for FY26).

* Gross profit rose ~14% YoY to INR12.9b (vs. our est. INR12.5b) as gross margin expanded ~85bp YoY to 59.5%, likely driven by lower discounting.

* Other expenses spiked 26% YoY, likely due to higher A&P spending, while employee (up 4% YoY) and rental expenses (down 2% YoY) were contained.

* Reported EBITDA at INR3.5b grew ~14% YoY (in line) as EBITDA margin expanded by ~30bp YoY to 16.2% (20bp miss).

* Depreciation grew 12% YoY, while interest cost declined ~4% YoY.

* Adj. PAT at INR605m jumped ~58% YoY (~6% above our estimate)

Valuation and view

* ABLBL’s lifestyle brands have achieved scale along with healthy profitability, while the company is focused on scaling up its emerging brands such as American Eagle (denim), Reebok (footwear), and Van Heusen Innerwear (innerwear and athleisure), providing a compelling retail play with a balanced growth and profitability profile with strong cash generation and robust return ratios.

* Management targets to double revenue (~12% CAGR) over FY24-30 through the company's sustained high-single-digit, like-to-like growth and an accelerated store rollout.

* However, we believe that given the widespread presence of lifestyle brands across EBOs, MBOs, LFS, and online channels and rising D2C competition, sustained double-digit growth could prove challenging.

* We fine-tune our FY27-28 estimates and model a CAGR of 9%/11%/24% in revenue/EBITDA/adj. PAT over FY26-28E.

* We reiterate our Neutral rating with a revised TP of INR120 (earlier INR115), premised on ~20x FY28E pre-Ind AS EV/EBITDA. We prefer Arvind Fashions over ABLBL for its superior growth profile and improved profitability.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412