Buy Northern Arc Capital Ltd for the Target Rs.390 by Motilal Oswal Financial Services Ltd

Strong quarter; strategic D2C expansion drives profitability

NIMs (calc.) expand ~30bp QoQ; asset quality improves and credit costs moderate

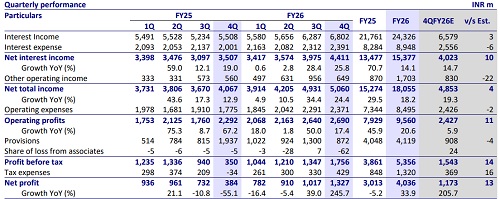

* Northern Arc’s (NACL) 4QFY26 PAT grew ~250% YoY (on a lower base) to ~INR1.3b (~13% beat). FY26 PAT grew ~34% YoY to INR4b. 4Q NII rose ~26% YoY to ~INR4.4b (10% beat). Other income grew ~16% YoY to ~INR649m.

* Opex rose ~34% YoY to ~INR2.4b (in line). PPoP grew ~17% YoY to INR2.7b (11% beat). FY26 PPoP grew ~21% YoY to INR9.6b. Credit costs in 4Q stood at ~INR872m (in line) with annualized credit costs of ~2.3% (PQ:~3.7%, PY:~6.3%).

* NACL’s AUM growth is being driven by the rising share of the higher-yielding D2C portfolio (improving from ~19% in FY21 to ~56% in FY26), supported by strong momentum in consumer finance and MSME lending. Expansion in physical distribution, addition of new lending partners, and high repeat customer engagement (~70%) have strengthened its sourcing capabilities and customer stickiness.

* In future, the company also expects incremental traction from products such as LAP and affordable housing, which can be distributed through its existing branch network. The credit solution platform continues to offer steady growth opportunities and a stable, risk-adjusted fee income stream, supported by a diversified partner ecosystem and strong franchise relationships.

* NACL continues to optimize its liability profile by diversifying funding sources and maintaining a balanced mix of fixed and floating-rate borrowings. Increased use of capital market instruments and offshore borrowings has reduced dependence on bank funding.

* Management indicated that incremental borrowing costs have moderated, with the overall cost of funds witnessing a sequential decline and expected to remain broadly stable at ~8.5-8.6%. Further, a rising share of the higheryielding D2C portfolio and stabilization in the rural finance segment are expected to support gradual improvement in margins over the medium term.

* NACL has structurally transitioned from an IR-led model to a D2C-led portfolio, resulting in improved yields and enhanced profitability. Disciplined risk management, supported by field-level oversight, FLDG arrangements, and CGFMU guarantees, should keep credit costs contained. In addition, fee income from fund management and placements continues to enhance revenue diversification, supporting earnings stability and stronger return metrics.

* NACL trades at 1x FY27E P/BV. We model an AUM/ PAT CAGR of ~21%/34% over FY26-28E, with RoA/RoE of ~3.2%/15% in FY28E. Reiterate our BUY rating with a TP of INR390, based on 1.2x FY28E P/BV.

Lending AUM grew ~22% YoY; D2C momentum accelerates

* Lending AUM grew 22% YoY/10% QoQ to INR166b. The D2C AUM in the mix improved to ~59% in Mar’26 (vs. ~56% in Dec’25). MSME AUM rose ~43% YoY to ~INR36.9b, while Consumer AUM grew ~50% YoY to ~INR50.9b, and Rural AUM declined ~8% YoY to INR10b.

* Fund AUM declined 2% YoY/ 4% QoQ to ~INR30.9b, while placements declined ~5% YoY to ~INR118b.

* The company has 57 digital partners and 368 originator partners. The branch network has grown to 432 branches (90 for MSME and 342 for Rural).

* We expect NACL to deliver AUM CAGR of ~21% over FY26-28E, largely supported by strong D2C growth.

Valuation and View

* NACL delivered a strong 4QFY26 performance, supported by healthy growth across all key operating parameters. Management remains confident of sustaining this momentum in FY27, aided by the recovery in the MFI segment and continued strong growth in the MSME and consumer finance businesses. The credit solutions business, which provides a steady fee income stream, along with a continued focus on asset quality and prudent risk management, places NACL on a strong footing to deliver sustainable long-term growth.

* NACL trades at 1x FY27E P/BV. We model an AUM/ PAT CAGR of ~21%/34% over FY26-28E, with RoA/RoE of ~3.2%/15% in FY28E. Reiterate our BUY rating on the stock with a TP of INR390, based on 1.2x FY28E P/BV.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412