Buy Sagility Ltd for the Target Rs.57 by Motilal Oswal Financial Services Ltd

Strong FY26; FY27 to be a year of normalization

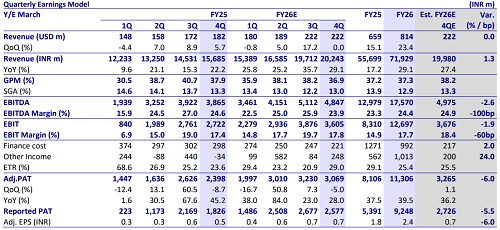

* Sagility’s 4QFY26 revenue rose 25.8% YoY in constant currency (CC), in line with expectations. EBIT margin stood at 17.8%, and adj. PAT came in at INR3.1b (up 28.0% YoY), below our estimate of INR3.3b due to a higher tax rate and margin-related impact.

* During FY26, Sagility’s revenue/EBITDA/adj. PAT grew 29.1%/35.4%/39.5% YoY in INR terms. Management guided for low double-digit CC revenue growth in FY27 and EBITDA margin of 24-25%. Margins are expected to trend toward the upper end of the range. We value the stock at 20x FY28E EPS to arrive at our TP of INR57. We reiterate our BUY rating on the stock.

Our view: US healthcare cost pressure remains a structural tailwind

* Healthy FY26 growth; FY27 to be a normal year: Sagility posted 23.6% YoY CC growth in FY26 on the back of continued expansion within existing clients and increasing contribution from new clients acquired in FY26.

* We estimate revenue growth of ~11.4% YoY CC in FY27 and EBITDA margin of 24.3% in FY27 and expect growth to accelerate in FY28.

* Margin to remain range-bound: EBITDA margin at 25.9% was within the guided range. Focusing on outcome-based engagements helps de-link revenue from transaction- or headcount-based pricing, thus improving margin resilience. However, we do not expect any meaningful margin expansion in the near term, given the pricing and cost pressure faced by the US-based health insurance companies. Overall, we expect margins to remain range-bound and model a ~24-25% EBITDA margin for FY27-28, considering likely margin risk.

* Deal TCV: Commercial momentum remained healthy, with USD30.7m of potential steady-state ACV signed during 4QFY26 through expansion and new statements of work across 18 existing clients and clients added during FY26. Full-year ACV wins were ~USD130m.

* Client concentration is continuously improving, with the top three clients now contributing less than 60% of revenue, while the number of clients generating more than USD20m annually increased to nine in FY26 from four in FY23.

Valuation and View:

We believe FY27 will be a year of growth normalization considering a high base of FY26. We expect business to grow in normalized lower double digits and margin to remain in the current range only. We believe the new logo addition, cross-selling, and synergy from Broadpath will drive its revenue/EBITDA/PAT CAGR of 19%/20%/24% over FY25-28. Consequently, we reiterate our BUY rating on the stock with a TP of INR57 (based on 20x on FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412