Buy Rubicon Ltd for the Target Rs. 740 by Motilal Oswal Financial Services Ltd

Gains in the gale

* Rubicon Research is a fast-growing research and development-driven pharmaceutical manufacturing company with a focus on regulated markets (particularly the US).

* Notably, over the past decade, Rubicon has built a sustainable moat through a) full spectrum capabilities across multiple dosage forms (oral solids, oral liquids, Nasal Sprays, Topicals) with a track record of successful specialty projects (170 scientist pool); b) building supporting manufacturing capacities with a consistent compliance track record of supplying to US markets; and c) focusing on commercial success.

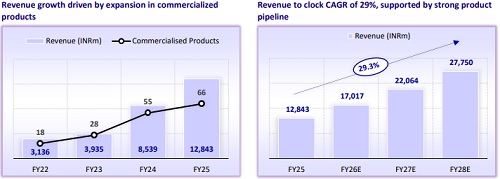

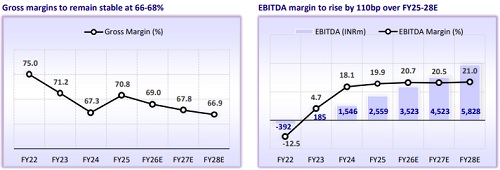

* Over FY22-25, Rubicon’s revenue has increased at a CAGR of 60% to INR12.8b. From an operational loss of INR392m in FY22, it has posted EBITDA of INR2.5b in FY25 with a margin of 19.9%. Effectively, from a net loss of INR671m in FY22, it has reported PAT of INR1.3b in FY25. Accordingly, Rubicon delivered ROE of 29% in FY25.

* Over FY25-28, we estimate a CAGR of 29%/32%/43% in revenue/ EBITDA/PAT to INR27.8b/INR5.8b/INR3.9b, driven by a) new launches in generics, including nasal sprays; b) enhanced focus on prescription-led business in CNS therapy; c) stable R&D productivity; and d) curated approach toward supply chain management to maintain high commercialization rate/minimize supply failure.

* Considering a strong earnings CAGR of 43% over FY25-28 and 30%+ RoE (adj. for recent fresh issue), we believe Rubicon should command a premium valuation. Rubicon scores well-ahead of peers in pharma space on ROE*earnings CAGR matrix (pls refer Exhibit 50). Hence, we assign 35x (30% premium to sector multiple of 27x) 12M forward earnings to arrive at a TP of INR740. Initiate with BUY.

Rubicon scales despite US generics headwinds

* After enjoying prosperous US generics business opportunities over CY05-15, Indian pharma companies have faced multiple challenges since then, such as a) consolidation of PBMs/buyers, b) faster ANDA approvals increasing competition, and c) rising adverse inspection outcomes prolonging incremental approvals.

* Against this backdrop, Rubicon has achieved a commendable scale-up in business (from INR390m revenue in FY15 to INR12.8b in FY25), backed by a curated approach to R&D, product approvals, efficient manufacturing and sound compliance.

Scaled up portfolio with faster launches; 70 commercialized by Jun’25

* Rubicon has considerably scaled up its commercial product base from 18 in FY22 to 70 by Jun’25. It achieved a strong commercialization rate of 86.4% (conversion from approval to launches) as of Q1’FY26, reflecting efficient product launches.

* Rubicon’s current product portfolio spans four dosage forms -- oral solids (OS), oral liquids (OL), nasal sprays, and topicals. Revenue from OS increased at a 57% CAGR to INR11b over FY22-25. OL revenue scaled up from INR43m in FY22 to INR1.3b in FY25. OS/OL revenue grew 7%/25% YoY to INR3b/INR355m in 1QFY26. After product launches in FY24, Nasal spray dosage revenue was INR124m/INR80m in FY25/1QFY26.

* R&D spending of INR2.8b over FY24-1QFY26 indicates that Rubicon will sustain its product filing momentum going forward, providing increased certainty to revenue growth prospects over FY25-28. Notably, it has filed six ANDAs and received approval for six ANDAs in 1QFY26.

Nasal sprays – Promising growth driver

* Nasal sprays’ contribution to Rubicon’s revenue has been increasing, 2.3%/1.0%/0.4% over 1QFY26/FY25/FY24, supported by the approval of the Ambernath nasal spray manufacturing facility in May’24.

* Nasal spray US generics industry is poised to be the fastest-growing formulations, projected to clock 9.5% CAGR over CY25-30, led by innovations in nasal drug delivery technologies and a growing patient preference for non-invasive, rapidacting treatments.

* Nasal spray approvals remain relatively limited, with only a few companies securing ANDA approvals over the past five years. Rubicon distinguishes itself by obtaining four of the 25 nasal spray approvals granted over CY23-Jun’25.

* Among recent approvals, Fluticasone Propionate nasal spray, a corticosteroid used for allergic rhinitis, holds an estimated market size of USD1b, with nasal sprays contributing USD482m. Notably, Rubicon is the fourth generic company to receive approval, with the first two firms receiving approval in CY07/CY12. Ipratropium Bromide, an anticholinergic for rhinitis relief, has a total market size of USD247m in FY25, with nasal sprays accounting for USD65m. There are five generic companies having ANDA approval for this product, including Rubicon.

From ANDAs to Rx brands: Rubicon’s CNS playbook

* Rubicon is implementing efforts toward building prescription-led business in CNS space. Rubicon has three branded products - Equetro, Raldesy, and Lopressor OS, which do not have any other AB-rated generics as of Jul’25.

* Raldesy is the first FDA-approved oral liquid formulation of Trazodone Hydrochloride, offering a novel dosage option in the antidepressant category.

* Equetro is the only FDA-approved carbamazepine formulation indicated as a mood stabilizer for bipolar I disorder.

* Lopressor OS, a liquid formulation of metoprolol tartrate, addresses the need for flexible dosing in conditions such as hypertension, heart failure, and post-MI care.

* In addition to enhanced offerings, we expect increased focus on marketing to drive better business prospects in this segment for Rubicon.

Enhanced focus on R&D; superior productivity

* Rubicon’s R&D spending stands at 11% of revenue, significantly higher than the industry median of 6%, highlighting its strategy of building a broad product portfolio rather than relying on a narrow range.

* The company demonstrated strong efficiency in converting R&D investments into revenue, with one of the highest R&D turnovers among peers, measured as US revenues relative to R&D spending from two years ago.

* With FY25 US revenue nearly 6x its FY22-23 R&D expenditure, Rubicon’s disciplined product selection and development approach is delivering solid results.

* Note: While some peers allocate R&D spending toward other geographies as well, we understand that the primary focus is on the US market, which aligns with our comparison of R&D to US sales.

Amid rising USFDA scrutiny, Rubicon’s record stays unblemished

* While India remains a cornerstone of global generic drug supply, the sector continues to face intensified regulatory scrutiny from the USFDA.

* India’s share of non-US inspections increased significantly, from 5% in CY21 to 33% in 1HCY25, with 486 inspections conducted during CY23-24 and 40 facilities receiving OAI classifications.

* Rubicon’s unblemished compliance record serves as a key differentiator. It has faced 10 USFDA inspections till date at its manufacturing site. It has never received an OAI classification, underscoring its disciplined quality systems, strong governance practices, and deep-rooted culture of regulatory integrity.

Valuation and view: Initiate coverage with BUY rating

* The business models in the US pharma market have been evolving, considering limited buyers and a large number of global manufacturers supplying medicines. Companies like Sun Pharma have scaled up NCE-led prescription business, while other generic companies are building a complex to develop/manufacture products to overcome competitive pressures. This has led to a significant increase in R&D spending. With USFDA approval timelines being unpredictable, the return on investment and investor interest in this space are limited.

* We believe Rubicon is creating a robust business model with a multi-disciplinary, data-driven, RoI-centric product selection framework. The consistent compliance track record provides a strong backbone for superior growth in earnings and return ratios.

* We model a 29% revenue CAGR, 110bp margin expansion, and 43% PAT CAGR over FY25-28 under our base case scenario. We also assign a 35x 12M forward earnings multiple to arrive at our TP of INR740, implying a potential upside of 22%.

* The bull case scenario builds in 32% revenue CAGR with 220bp margin expansion, and 50% PAT CAGR over FY25-28, aided by a higher commercialization rate, a steady flow of product approvals, continued regulatory compliance, and a supportive market environment. This would lead to a TP of INR930, based on 38x 12M forward earnings multiple, implying a potential upside of 54%.

* The bear case scenario assumes 26% revenue CAGR with 50bp margin expansion due to a less favorable market, delays in product development, slower commercialization, and operational setbacks due to regulatory challenges. These factors would result in a TP of INR550, based on the 29x 12M forward earnings multiple, implying a potential downside of 10%. We initiate coverage on the stock with a BUY rating.

Key risks

* Adverse policy changes affect pricing. Regulatory aspects may impact business performance.

* Adverse classification of inspections may prolong growth prospects of the company.

* Changes in regulatory guidelines for product approval may delay the business opportunity for Rubicon.

* Geopolitical conflicts involving major suppliers, including China, the US, or Europe, could disrupt supply chains and weigh on revenue growth.

* Lower-than-expected market share gains in commercialized products may affect the operating leverage of the company.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412