Buy Larsen & Toubro Ltd for the Target Rs. 4,500 by Motilal Oswal Financial Services Ltd

CMD meeting takeaways

We recently interacted with Mr. S. N. Subrahmanyan, Chairman and MD of Larsen & Toubro (LT), to get insights into the company’s long-term growth strategy for domestic and international geographies, capital allocation and future focus areas. LT is optimistic about the Middle East region and expects ordering to grow in the midteens over the next five years from this region. Sector diversification and country diversification within the Middle East help LT tide over the volatility in oil prices. With private and government capex ramping up in select areas, LT overall hopes to maintain mid-teen growth in order inflows in the medium to long term. Management remains focused on its capital allocation strategy and expects to hive off non-core assets soon and keep investing in new-age areas over the next five years. We maintain our estimates and BUY rating on LT with an SoTP-based TP of INR4,500, based on 28x two-year forward earnings.

Key investment thesis

Middle East to remain a growth area for LT

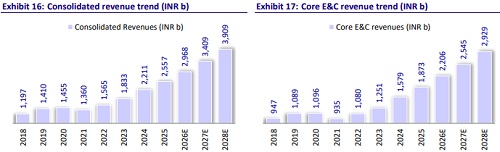

LT management is optimistic about the opportunities in the Middle East and expects LT to benefit from continued ordering growth of 10-15% for the next five years from this region. The company has learnt from its past mistakes and now has 1) diversified its country base in the Middle East such as Saudi Arabia, Kuwait and Qatar, 2) diversified its project mix across hydrocarbon – onshore as well as offshore, gas-related projects, renewables, and transmission, and 3) good control over the supply chain network as well as labor supply. With international projects now forming nearly 49% of the order book, LT has welldefined clauses in the contracts if the payments get delayed from these projects. In our estimates, we have baked in an 11% CAGR in core E&C order inflows over FY25-28E.

Domestic capex is selective but growing

Domestic ordering for LT has remained largely flat over FY23-25, since there have been a limited number of large-sized projects from the government during the same period and since LT has maintained its selective stance in light of higher competition. The company is eyeing projects across thermal, nuclear, hydroelectric, renewable, urban infra, buildings and factories, state irrigation projects, and defense in the domestic segment. On the private capex side, LT is witnessing traction from areas like metals and mining, real estate, electronic manufacturing, refineries, thermal power, bigger projects from the Reliance Group, etc. These segments will continue to drive capex activity in the private sector, with big and chunkier projects expected in thermal and metals and mining. We expect a 5% CAGR in domestic order inflows over FY25-28.

Optimistic about thermal BTG-related opportunities

The company is optimistic about thermal BTG opportunities and has already bagged two large projects: 1) NTPC order worth more than INR150b in Madhya Pradesh and Bihar, and 2) Adani Power order worth INR260b to set up 8x800MW thermal power units. The company is also in discussions with other large players in thermal power. With a large opportunity pipeline of 35-40GW of ordering over the next five years and with the BTG market largely being a two-player market, LT expects to benefit from incremental orders on an ongoing basis in thermal power. LT is also in discussions with Torrent Power for the upcoming thermal power opportunities.

Participation in defense programs

LT has formed a consortium with Bharat Electronics (BEL) for the AMCA program of the Indian Air Force. The consortium’s scope of work includes development of the prototype airframe, jigs and fixtures, system integration, and flight certification for the next-generation stealth fighter. The shortlisting of eligible bidders is expected by 3QFY26, followed by the issue of the RFP in 4QFY26, and award of the prototype contract by 4QFY27. Besides AMCA, the company is expecting orders for guns, land systems, naval ships, etc. LT has also secured a contract from the Indian Army to indigenously produce BvS10 Sindhu vehicles at its Hazira Armoured Systems Complex with design and technical support from BAE Systems. Unlike global models where a single player owns a platform, India encourages multi-party bidding for the same order, which dilutes scale, continuity, and R&D payoff for private players like LT. The company expected revenue of ~INR100b from the defense segment in FY26.

Risk mitigation strategies for ultra-mega projects

Risks exist from areas such as 1) slowdown in capex spending and hence delayed payments, 2) commodity prices since these projects are fixed-price in nature, and 3) supply chain issues in procuring raw materials, labor issues, etc. LT has addressed these issues by maintaining a strong control over supply chain through rigorous vendor pre-qualification and a diversified labor base. The company has a balanced product mix sectors and geographies and targets multilateral-funded projects that offer greater stability and lower counterparty risks. The company’s diverse global subsidiary base adds complexity to governance and performance monitoring. To manage this, LT has maintained a centralized oversight mechanism, conducts regular performance and compliance reviews, and has placed senior management on key subsidiary boards to ensure tighter control, alignment and timely intervention.

Focusing on capital allocation and non-core divestment stays

Management remains focused on overall capital allocation across new-age areas as well as on divestment of non-core assets. The divestment of Hyderabad metro is expected to be completed by Mar’26. Under the arrangement, the entire debt of INR130b of Hyderabad Metro would be taken over by SPV floated by Telangana govt, and LT will receive an equity of INR20b vs. its adjusted equity of INR10b (INR75b actual equity adjusted with accumulated losses of INR65b in Hyderabad Metro). The company is also evaluating the divestment of Nabha Power project. LT remains committed to investing in 1) expanding data center capacities, 2) electrolysers, 3) semi-conductor design (fabless) and industrial electronics, and 4) real estate as it plans to list its real estate division in a year. Overall, over the next five years, LT expects to invest a total of INR1t in all these areas.

Financial Outlook

We expect a CAGR of 11% in core EPC order inflows over FY25-28. With a strong track record of execution, we expect a 16% CAGR in core EPC revenue over the same period, with core EPC margin assumption of 8.5-8.9% for FY26-28. We thus expect a CAGR of 19%/22% in core EBITDA/PAT over FY25-28.

Valuation and view

At the current price, for core E&C, LT is trading at 31x/26x/21x P/E on FY26/27/28E earnings. We maintain our estimates and continue to value the company at 28x P/E on two-year forward earnings for core business and 25% holding company discount for subsidiaries. We maintain BUY with an unchanged TP of INR4,500.

Key risks and concerns

A slowdown in order inflows, geopolitical issues, delays in the completion of mega and ultra-mega projects, a sharp rise in commodity prices, an increase in working capital, and increased competition are a few downside risks to our estimates.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412