Neutral Muthoot Finance Ltd for the Target Rs. 3,800 by Motilal Oswal Financial Services Ltd

Shining stronger; margin expansion and recoveries lift earnings

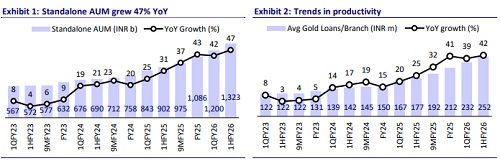

Stellar gold loan growth of ~45% YoY; calc. NIM expanded ~60bp QoQ

* Muthoot Finance’s (MUTH) strong operating performance in 2QFY26 was driven by: 1) strong gold loan growth of ~45% YoY to ~INR1.25t, 2) ~35bp QoQ improvement in GS3 to 2.25%, aided by NPA recoveries, 3) an increase in gold tonnage by ~5% YoY to 209 tons, and 4) spreads rose ~60bp QoQ to ~11.8%, driven by NPA recoveries and a decline in the CoF.

* MUTH’s 2QFY26 PAT grew 87% YoY and 15% QoQ to ~INR23.5b (~23% beat). This included a one-time interest income write-back of ~INR3-3.5b arising from the liquidation of deep/old NPA accounts. The yield improvement was driven partly by this one-off in interest income and partly by a higher share of high-yield gold loan disbursements over the past two quarters. PAT grew 88% YoY in 1HFY26 and is expected to grow ~48% YoY in 2HFY26. Reported RoA/RoE in 2QFY26 was strong at 7.2%/30%.

* Net total income grew 61% YoY to ~INR41.5b (~18% beat). Opex grew ~34% YoY to INR8.8b (in line), resulting in a cost-to-income ratio of ~21.3% (PY: 25.7% and PQ: 22.6%). PPOP grew 71% YoY to ~INR32.7b (~22% beat). Provisions stood at ~INR1.1b (vs. MOFSLe of ~INR1b) and translated into annualized credit costs of ~35bp (PY: ~100bp and PQ: ~15bp) in 2QFY26.

* Gold tonnage rose 5% YoY but remained flat QoQ. The customer base grew ~1.7% QoQ to ~6.57m. Gold loan LTV declined ~5pp QoQ to ~56.6%.

* MUTH upgraded its FY26 gold loan growth guidance to 30-35% (from 15% earlier), driven by favorable regulatory changes, higher gold prices, and rising demand amid tightening in unsecured lending segments. We model gold loan growth of ~38% in FY26E.

* We raise our FY26/FY27 EPS estimates by ~10% each to factor in higher loan growth and sustenance of current NIMs in the next fiscal as well. We model a standalone AUM/PAT CAGR of ~23%/29% over FY25-28E. We model an RoA/RoE of 5.3%/23% for FY28E.

* MUTH now trades at 3.1x FY27E P/BV and 14x P/E and, in our view, has benefited from the tailwinds of: 1) a sharp rise in gold prices and 2) an improvement in gold loan demand due to the industry-wide rationing in unsecured credit. MUTH is indeed one of the best franchises for gold loans in the country, as is evident from its ability to deliver industry-leading gold loan growth and best-in-class profitability. Reiterate our Neutral rating with a revised TP of INR3,800 (based on 3.2x Sep’27E P/BV).

Belstar: AUM flat sequentially; GNPA rises ~15bp QoQ

* MUTH’s MFI subsidiary, Belstar, reported a ~3% QoQ and 23% YoY decline in AUM to ~INR77b. Reported loss stood at ~INR1.3b during the quarter (vs. a loss of INR1.2b in 4QFY25).

* Asset quality improved, with GS3 declining ~55bp QoQ to ~4.45% (PQ: 5%).

* Belstar opened 23 new gold loan branches to diversify the portfolio. It has obtained IRDAI approval to act as a corporate agent for the distribution of insurance products.

Highlights from the management commentary

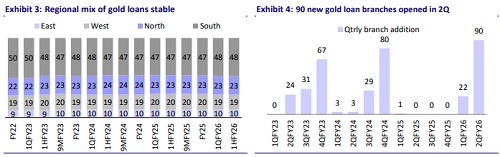

* The company aims to add 100-200 gold loan branches annually and has applied to the RBI for additional branch opening approvals to further improve its distribution.

* MUTH stated that while competition exists, the gold loan market remains sufficiently large to support growth for all players. The company believes there is ample room for all gold loan lenders, with gold loan demand expected to strengthen further.

* The company has a residual ARC pool of INR900m and also expects an additional recovery of ~INR300-400m.

* The Board of Directors approved an equity infusion of ~INR5b into Muthoot Money, a wholly-owned subsidiary of MUTH.

Valuation and view

* MUTH delivered a healthy all-round beat in the quarter, even after adjusting for the one-offs in interest income. Gold loan growth remained strong, while asset quality improved on the back of recoveries from the NPA pool. NIMs and spreads also expanded during the quarter, driven by higher yields and a decline in CoF.

* With a favorable demand outlook for gold loans, driven by the limited availability of unsecured credit, the company is well-positioned to maintain its healthy loan growth momentum. Reiterate our Neutral rating with a revised TP of INR3,800 (based on 3.2x Sep’27E BVPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412