Buy Lodha Developers Ltd for the Target Rs. 1,888 by Motilal Oswal Financial Services Ltd

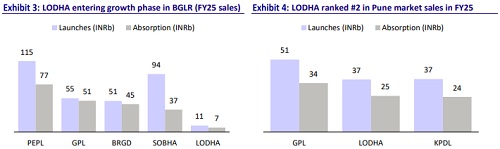

MMR powerhouse, Pune scaler, Bengaluru riser, NCR newcomer

LODHA’s presales are expected to clock a 22% CAGR, supported by healthy collections and debt at comfortable levels of 0.25x by the end of 1HFY26, despite aggressive BD additions of INR250b. Pune is scaling up at a healthy pace and is expected to deliver 40% YoY growth in sales. The company has also completed its pilot phase in Bengaluru and entered the growth phase, expecting a 12% market share by the end of the decade. In addition, it is in the process of initiating a pilot in the NCR. LODHA is further expanding its commercial and industrial portfolio to drive strong rentals. Palava is also set to scale up its sales by 20% YoY, supported by the Airoli-Katai tunnel nearing completion by the end of FY26 and other ongoing infrastructural developments. The company’s steady pace of project acquisitions enhances long-term visibility, while its disciplined and timely execution ensures that this momentum is effectively translated into sustained performance. We reiterate our BUY rating with a TP of INR1,888, which implies a 58% potential upside.

Set to deliver record presales of INR60b each in 3Q-4QFY26

* Since FY21-25, LODHA has delivered a consistent 31% CAGR in presales. In FY25, presales grew 22% YoY to INR176.3b, surpassing guidance. In 1HFY26, LODHA reported presales of INR90.2b, up 8% YoY, achieving ~43% of its annual presales guidance of INR210b.

* This was due to slower launches in the first half. For the remainder of FY26, the company plans to launch 11 new projects (9.6msf with a GDV of INR133b) across Pune, Bengaluru, and MMR, along with five new-phase launches (3.7msf with a GDV of INR37b). The new launches will be in MMR (eight projects), Pune (three projects), and Bengaluru (four projects).

* On the back of these launches and LODHA’s continued sales momentum, the company is set to achieve its highest-ever quarterly presales of INR60b each in 3Q-4QFY26, posting a 33% and 25% YoY growth, respectively. 2HFY26 will play a major role in helping the company maintain average quarterly presales of INR50b from FY26 onwards.

* Building on its strong presence in MMR, Pune, and now Bengaluru, it is set to achieve a 22% presales CAGR over FY25-28E, reaching INR317b in FY28E, backed by a strong launch pipeline and healthy execution capabilities.

* Unlike other peers, LODHA, while not launch-dependent, continues to actively introduce new projects/phases and enter new markets. In 1HFY26, it acquired projects with a GDV of INR250b across MMR, Pune, and Bengaluru, with MMR contributing the highest GDV of INR141b. LODHA has also entered the growth phase in Bengaluru and aims to initiate a pilot in NCR by FY27.

*Additionally, Palava township’s visibility and accessibility are expected to improve significantly with the planned opening of the Airoli–Katai tunnel by the end of FY26, along with other infrastructure enhancements. This enhanced connectivity is likely to drive higher footfall and strengthen customer confidence, driving an anticipated 20% increase in sales.

Valuation and view: On track for sustained growth; reiterate BUY

* The company has delivered steady performance across its key parameters, and as it prepares to capitalize on strong growth and consolidation opportunities, we expect this consistent operational performance to continue.

* At Palava, LODHA has a development potential of 600msf. However, we assume that a portion of this would be monetized through industrial land sales. We value 250msf of residential land to be monetized at INR637b over the next three decades.

* We use a DCF-based method for the ex-Palava residential segment and arrive at a value of ~INR549b, assuming a WACC of 11.1%. Reiterate BUY with a TP of INR1,888.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412