Buy Titan Company Ltd for the Target Rs.5,300 by Motilal Oswal Financial Services Ltd

Robust India profitability; miss on international front

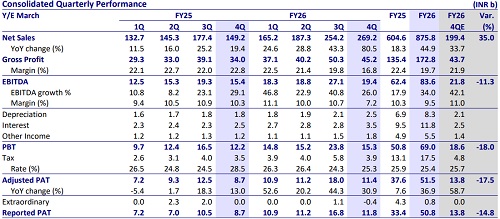

* Titan (TTAN) delivered yet another strong quarter, with 4Q consolidated revenue growing 81% YoY. Standalone jewelry sales (excl. bullion) rose 45% YoY, driven by broad-based consumer interest in the category despite record-high gold prices.

* Studded share of domestic jewelry (incl. CaratLane) stood at 31% vs. 34% in base amid volatile gold prices in the quarter. The domestic jewelry segment posted 50% LFL growth (Tanishq, Mia and Zoya). Buyer growth improved notably to 8% in 4Q (flat in FY26), and average ticket size jumped 40% YoY. Initiatives such as the gold exchange program grew in strong double digits and increased the availability of lightweight jewelry, aided by affordability and healthy footfall.

* Standalone jewelry EBIT margin (excl. bullion) contracted 140bp YoY to 10.5% (est. 11.1%) due to higher gold coin mix and marketing spend. Standalone EBIT grew 29% YoY (41% for domestic brands) vs. our est. of 27%. CaratLane’s EBIT margin expanded 130bp to 8.3% but was lower than expected due to lower revenue growth and continued investment in campaigns (FY26 EBIT margin at ~10%). Management said that sustaining jewelry EBIT margins around 11-11.5% becomes challenging if gold prices continue to rise as it affects the product mix. However, management aims to sustain healthy EBIT growth going ahead.

* Watch division revenue grew 8% YoY (below) and EBIT rose 7.5% YoY (11.7% margin). Eye care revenue rose 18% YoY and EBIT increased by 11% (9.3% margin).

* We remain constructive on jewelry segment growth for top players, and we believe TTAN, with its initiatives like the exchange program would remain competitive. While 4Q profitability was impacted by international business losses and higher spends in CaratLane, we expect healthy domestic demand momentum to continue. Apart from industry formalization, stability in gold prices can further improve margin visibility for TTAN. We model a CAGR of 15% in sales, 20% in EBITDA, and 24% in APAT over FY26-28E. We reiterate our BUY rating on the stock with a TP of INR5,300, based on 60x Mar’28E EPS. TTAN remains one of our top picks in the space.

India jewelry EBIT growth at 29%; PAT miss due to international losses

* Strong revenue growth continues:

TTAN’s consolidated revenue grew by a strong 81% YoY to INR269.2b (est. INR199.4b), including bullion sales of INR62b (up ~7x YoY). Consolidated jewelry sales grew 89% YoY to INR249.9b (est. 180b); excl. Bullion, sales grew 53% to INR187.5b. Watches sales grew 8% YoY to INR12b (est. INR13b), while eye care sales grew 18% YoY to INR2.3b (est. INR2.2b).

* LFL growth at ~50%:

Standalone sales (excl. bullion) grew 45% to INR163b (est. INR152). Domestic jewelry (Tanishq, Mia and Zoya) posted 50% LFL growth, and all brands, including CaratLane, reported 47% LFL growth. Secondary sales grew 54% YoY amid broad-based consumer interest in the category despite recordhigh gold prices. CaratLane’s revenue grew 22%, primarily led by healthy double-digit increase in ASPs. TTAN added 32 jewelry stores (135 last 12 months), taking the total to 1,226 stores. In 4Q, it added 12 Tanishq store, six CaratLane stores and 14 Mia stores.

* Mix impact on GM:

Consol. gross margins contracted 600bp YoY to 16.8%, impacted by increased gold coin sales, lower studded jewelry margins (due to higher gold content value), and higher bullion sales. Ad spends increased by 23% YoY, other expense increased by 38% YoY and employee cost rose 48% YoY. Consolidated EBITDA margin declined 300bp YoY to 7.2% (est. 11%); the miss was largely on account of high bullion sales.

* Standalone jewelry EBIT (ex-bullion) growth at 29%:

Domestic business (Tanishq, Mia, Zoya, CaratLane) EBIT rose 41% YoY to INR19b. Standalone EBIT (ex-bullion) grew 29% YoY (est. 27%) to INR17.1b, while EBIT margin contracted 140bp YoY to 10.5% (est. 11.1%, 3QFY26 10.6%) on poor mix. CaratLane’s EBIT margin expanded 130bp YoY to 8.3%. Watches EBIT margin remained flat YoY at 11.7% (est. 12.1%). Eye Care margin was down 60bp YoY at 9.3% (est. 9.6%).

* Strong growth in profitability:

Consolidated EBITDA grew 26% YoY to INR19.4b (INR 21.8b). PBT was up 25% YoY at INR15.3b (est. INR18.6b). Adj. PAT rose 31% YoY to INR11.4b (est. INR13.8b).

* In FY26, net sales, EBITDA and APAT grew by 45%, 34% and 37%, respectively.

Valuation and view

* We maintain our EPS estimates for FY27 and FY28.

* TTAN, with its superior competitive positioning (in sourcing, studded ratio, youth-centric focus, and reinvestment strategy), continues to outperform other branded players. Its brand recall and business moat are not easily replicable; therefore, Tanishq’s competitive edge will remain strong in the category.

* The store count reached 3,473 as of Mar’26, and the expansion story remains intact. The non-jewelry business is also scaling up well and will contribute to growth in the medium term.

* Apart from industry formalization, stability in gold prices can further improve margin visibility for TTAN. Overall, we remain constructive on jewelry industry growth for top players, and TTAN, being the bellwether with superior historical execution track record, will benefit the most. We model a CAGR of 15% in sales, 20% in EBITDA, and 24% in APAT over FY26-28E. We reiterate our BUY rating on the stock with a TP of INR5,300, based on 60x Mar’28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412