Buy V-Mart Retail Ltd for the Target Rs.900 by Motilal Oswal Financial Services Ltd

Strong end to FY26; impact of raw material inflation key near-term monitorable

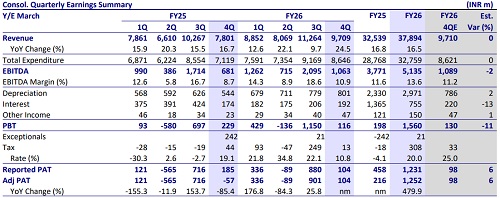

* VMART delivered a strong 4QFY26 with ~25% YoY revenue growth on the back of a sharp acceleration in blended SSSG to 12% (vs. flat in 3QFY26).

* Pre-IND AS EBITDA grew 5.2x YoY as margin expanded ~250bp YoY, driven by operating leverage, partly offset by elevated inventory provisioning and higher A&P spends (both were muted in 9MFY26).

* Management indicated that the demand environment remains stable and the company has been taking several steps to cushion the challenges posed by raw material inflation and their availability (secured most of the supplies till Dec’26) without necessitating a significant price hike.

* Medium-term guidance has been retained at ~13-15% annual area additions, with SSSG target of 5-8%.

* We moderate our FY27 gross margin estimate by ~50bp and, as a result, cut our FY27-28E pre-INDAS EBITDA estimates by 6-7%.

* We now model a CAGR of 17%/23%/27% in revenue/Pre-IND AS EBITDA/ adj. PAT over FY26-28E, supported by ~14% CAGR in store additions, mid-single-digit SSSG, and operating leverage benefits.

* We reiterate BUY with a revised TP of INR900, based on 20x FY28E EV/Pre-IND AS EBITDA. Despite the recent run-up, valuations remain undemanding at ~15x FY28E EV/pre-IND AS EBITDA (vs. ~29x for VMM).

Strong 4Q with 12% SSSG and ~250bp pre-IND AS EBITDA margin expansion

* 4QFY26 revenue grew 24.5% YoY (already disclosed) to INR9.7b, driven by 12% blended SSSG and ~16% YoY store additions.

* V-Mart opened 29 new stores (25 in V-Mart and four in Unlimited) and closed six stores (five in V-Mart and one in Unlimited) during 4Q, bringing the total store count to 577 (80 net additions in FY26).

* Gross profit grew 21% YoY to INR3.1b (in line), as gross margins contracted ~95bp YoY to 32.1% (~60bp miss), driven by higher inventory provision (~220bp, up 210bp QoQ and YoY).

* Employee expenses grew 3% YoY to INR1b (9% lower vs. estimates).

* Other expenses grew ~14% YoY to INR1.05b (7% higher than our estimate), driven by 27% YoY increase in A&P spends (up ~5bp YoY).

* Resultantly, reported EBITDA stood at INR1.06b (+56% YoY, in line), with margins expanding ~220bp YoY to 10.9% (~25bp miss).

* Pre-IND AS EBITDA grew 5.2x YoY to INR325m, with margins expanding ~250bp YoY to 3.3% (in line).

* Depreciation increased 47% YoY (in line) due to accelerated store additions, while interest cost rose ~11% YoY (13% below our estimate).

* V-Mart’s adjusted PAT stood at INR104m (vs. our estimate of INR98m and losses YoY), led by higher EBITDA and lower finance costs.

Valuation and view

* The improved productivity of VMART/Unlimited stores and lower losses in the online segment have led to an improvement in VMART’s overall profitability (pre-IND AS margins up ~180bp YoY to 6.2% in FY26).

* However, VMART still lags value fashion peers on profitability, which provides room for further margin expansion.

* VMART remains a key beneficiary of the unorganized-to-organized retail shift and the massive growth opportunity in value fashion. However, raw material inflation due to the West Asia conflict and its impact on demand/margins remains a key near-term monitorable.

* We moderate our FY27 gross margin estimate by ~50bp and as a result cut our FY27-28E pre-INDAS EBITDA estimates by 6-7%.

* We now model a CAGR of 17%/23%/27% in revenue/Pre-IND AS EBITDA/adj. PAT over FY26-28E, supported by ~14% CAGR in store additions, mid-single-digit SSSG, and operating leverage benefits.

* V-Mart has run up from its recent lows, but still trades at undemanding ~15x FY28 EV/pre–IND AS EBITDA (vs. ~29x for VMM). We believe risk-reward remains attractive with mid-to-high teen growth visibility and headroom for margin expansion.

* We reiterate BUY with a revised TP of INR900 (earlier 945), based on ~20x FY28E EV/Pre-IND AS EBITDA (implies ~10.75x reported EBITDA). VMART remains one of our top picks in retail space

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412