Neutral Senco Gold Ltd for the Target Rs.375 by Motilal Oswal Financial Services Ltd

Healthy revenue delivery; margin volatility continues

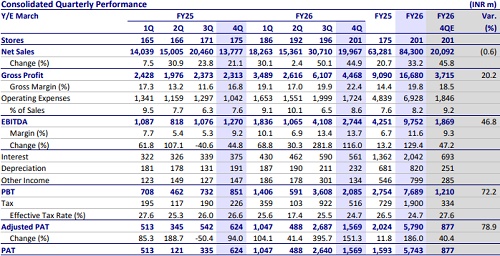

* Senco Gold (SENCO) delivered a consolidated revenue growth of 45% YoY to INR20b, (peers >50%). SSSG stood at 34% (24% in FY26), aided by wedding demand, gifting trends, and a higher old-gold exchange mix (50% of revenue). However, amid elevated gold prices, gold volumes declined 6% in FY26. Management highlighted that demand momentum sustained in 1Q, and expects to deliver ~20% revenue growth in FY27.

* The company opened five stores (+15% YoY) during the quarter, bringing the total store count to 201 (102 COCO, 85 FOCO, 12 Sennes, and 2 Dubai). It plans to open 18-20 stores in FY27.

* GM expanded sharply by 560bp YoY to 22.4% (vs. est. 18.5%; 19.9% in 3QFY26). Inventory gains were ~4.5% in 4Q and ~3.5% in FY26, which led to a sharp beat in our estimates. The company has reduced inventory to 40-50% in FY26 vs 95% in FY25. EBITDA margin expanded 450bp YoY to 13.7% (est. 9.3%, 13.4% in 3QFY26). Management has guided for EBITDA margin to be maintained at 7.5-7.8%. We model 7.5% for FY27/28 (close to the average of FY23-25).

* Given the inconsistencies in operating performance and low hedging ratios, we remain cautious on SENCO’s operating margin performance going ahead. We reiterate our Neutral rating with a TP of INR375 (15x Mar’28).

Key takeaways from the management commentary

* The company has maintained a hedging ratio of around 40-50% to manage gold price volatility, liquidity risks, and margin-related uncertainties during the quarter.

* Coins and bullion currently contribute around 5-6% of overall sales.

* In 4QFY26, EBITDA margin was 13.7%, with a normalized margin of 8–8.5% and the remainder driven by inventory/realization gains.

* The company has guided for ~20% revenue growth in FY27 while maintaining EBITDA margin guidance of 7.5-7.8%. PAT margin guidance was maintained at 4- 4.5%

Valuation and view

* With a beat on gross margin, we increase our EPS estimates by 9% for FY27 and 8% for FY28.

* SENCO’s gross margins have historically been volatile, reflecting the company’s low level of hedging and resultant inventory gains. Management has guided for EBITDA margin to be maintained at 7.5-7.8%. However, we model 7.5% for FY27/28 (close to the average of FY23-25).

* We model revenue and EBITDA CAGR of 14% and -8% over FY26-28. We reiterate our Neutral rating with a TP of INR375 (15x Mar’28).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412