Neutral Muthoot Finance Ltd for the Target Rs.3,720 by Motilal Oswal Financial Services Ltd

Earnings beat; gold tonnage and loan accounts decline QoQ Asset quality deteriorates, driven by RBI-directed borrower-level classification

* Muthoot Finance’s (MUTH) operating performance in 4QFY26 was driven by:

1) strong gold loan growth of ~50% YoY to ~INR1.54t

2) spread expansion of ~60bp QoQ to 12.5% as yields rose, aided by an increase in lending rates across select schemes

3) asset quality deterioration with ~75bp QoQ increase in GS3 to 2.4%, mainly driven by a shift from loanlevel NPA classification to borrower-level classification. This also led to higher provisioning and consequent credit costs in the quarter.

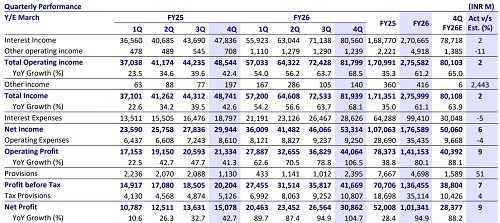

* 4QFY26 PAT grew 105% YoY and 16% QoQ to ~INR30.9b (~9% beat). This included one-off interest income of ~INR850m from ARC recoveries and auction-related proceeds. Yield improvement in the quarter was also driven by an increase in lending rates across select schemes. FY26 PAT grew 95% YoY to INR101.3b. Reported RoA/RoE remained strong at 7.95%/34%.

* Net total income grew 78% YoY to ~INR53.3b (~6% beat). Opex grew ~7% YoY to INR9.25b (inline), resulting in a cost-to-income ratio of ~17.4% (PY: 28.8% and PQ: 20.1%). PPOP grew 107% YoY to ~INR44b (~9% beat).

* Credit costs stood at ~INR2.4b (vs. MOFSLe of ~INR1.6b) and translated into annualized credit costs of ~62bp in 4QFY26 [PY: ~29bp and PQ: ~44bp].

* Gold tonnage declined ~4% QoQ to 196 tons. The customer base declined ~2% QoQ to ~6.41m. Gold loan LTV rose ~270bp QoQ to ~58.5%.

* MUTH guided for ~15% gold loan growth in FY27 and shared that the growth outlook would be reassessed in 2Q/3QFY27, depending on the business momentum. We model gold loan growth of ~25% in FY27.

* We raise our FY27E/FY28E EPS by ~3%/5% to factor in higher loan growth and higher blended yields. We model a standalone AUM/PAT CAGR of ~20%/15% over FY26-28E. We model RoA/RoE of 5.6%/25% by FY28E.

* MUTH now trades at 3x FY27E P/BV and 12x P/E and, in our view, has benefited from the tailwinds of:

1) A sharp rise in gold prices

2) An improvement in gold loan demand due to the earlier poor availability of unsecured credit. With its ability to deliver industry-leading gold loan growth and best-in-class profitability, MUTH is one of the best franchises for gold loans in the country. However, we see risks of market share losses for MUTH given the high competitive intensity and aggressive foray of multiple deep-pocketed AAA (or AA+ rated) NBFC franchises into gold loans. Reiterate our Neutral rating with a revised TP of INR3,720 (based on 2.5x Mar’28E P/BV).

Belstar: AUM rises 4% QoQ; GNPA rises ~60bp QoQ

* MUTH’s MFI subsidiary (Belstar) AUM grew 3% YoY and ~4% QoQ to ~INR82b. It reported PAT of ~INR1.3b during the quarter (vs. a PAT of INR509m in 3QFY26).

* GS3 in Belstar rose ~60bp QoQ to ~5.55% (PQ: 4.95%). The company opened 81 new gold loan branches in FY26 to diversify its loan mix.

Valuation and view

* MUTH reported a mixed performance during the quarter. While gold loan growth was strong, there was a QoQ decline in gold tonnage and active loan accounts. NIM expanded during the quarter, supported by higher yields, lower cost of funds, and lending rate hikes in select schemes. However, asset quality weakened due to the RBI-directed shift from loan-level to borrower-level classification, which led to higher provisions and consequent credit costs during the quarter.

* Given the increase in the customs duty on Gold (from 6% to 15%) and with further steps taken by the government to tighten gold imports, we expect gold prices to remain high. With a favorable demand outlook for gold loans, driven by still somewhat constrained availability of unsecured credit, the company is wellpositioned to maintain its healthy loan growth momentum. However, we see risks of market share losses for MUTH given the high competitive intensity and aggressive foray of multiple deep-pocketed AAA (or AA+ rated) NBFCs into gold loans. Reiterate our Neutral rating with a revised TP of INR3,720 (based on 2.5x Mar’28E BVPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412