Buy Bharti Hexacom Ltd for the Target Rs.1,860 by Motilal Oswal Financial Services Ltd

Muted 4Q in mobility; growth accelerates in Homes

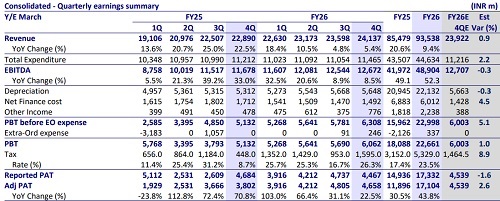

* Bharti Hexacom (BHL) reported a steady 4Q, with ~1% QoQ growth in customer wireless revenue (vs. 0.6% QoQ for Bharti-India wireless) and ~2% QoQ wireless EBITDA growth due to two fewer days QoQ.

* Growth accelerated in Homes and offices with ~21%/21%/28% QoQ growth in subscriber base/revenue/EBITDA driven by ramp-up in home broadband (HBB) and launch of IPTV.

* Similar to Bharti, capex surged~72% QoQ to INR5.9b, leading to a modest ~3% YoY growth in FY26 capex to INR15.2b.

* FCF generation was modest in 4QFY26 due to seasonally higher working capital requirements and AGR payouts. However, FY26 FCF remained robust at INR21.3b (vs. INR20.3b YoY), which led to ~INR16.5b YoY reduction in net debt (excl. leases) to INR20.3b (leverage down to 0.46x).

* BHL announced a dividend of INR18/share (vs. INR10/share YoY), and in the absence of investments in adjacencies (compared to Bharti), we expect dividend payouts to take precedence.

* BHL provides a pure-play exposure to BHARTI’s fast-growing wireless and HBB segments in circles with lower data and HBB penetration.

* Further, there are lower capital misallocation concerns with BHL (vs. BHARTI), which, along with a better return ratio, drives BHL to trade at an implied premium (~17% currently) to BHARTI’s India business, in our view.

* We ascribe a DCF-based FY28E EV/EBITDA of 13.5x to BHL (which is at ~15% premium to our multiple for Bharti’s India wireless business). We reiterate our BUY rating with a revised TP of INR 1,860 (vs. INR1,910).

Reported capex surges; FCF moderates QoQ due to seasonal working capital build-up

* Overall 4Q revenue at INR24.1b (+5% YoY) grew 2.3% QoQ, with customer revenue rising ~1.8% QoQ to INR22.8b.

* The growth in wireless business remained muted due to two fewer days QoQ, with ARPU moderating to INR252 (+4% YoY, in line).

* The launch of IPTV and acceleration in HBB net adds (+21% QoQ) drove robust ~21%/~28% QoQ growth in Homes & Offices revenue/EBITDA.

* Reported EBITDA grew ~1% QoQ to INR12.7b (+9.5% YoY, in line), while reported EBITDAaL grew 2.7% QoQ to INR11.6b, with pre-IND AS EBITDA margin rising ~25bp QoQ to 47.9%. Incremental pre-IND AS EBITDA margin stood at ~58% (vs. ~62% in 3Q).

* PAT at INR4.7b declined 3% QoQ (down 1% YoY) due primarily to a lower tax rate in the base quarter.

* Overall, 4Q capex surged 72% QoQ to INR5.9b (up 38% YoY), with FY26 capex broadly stable YoY at INR15.2b.

* Free cash flow (after leases and interest payments) moderated QoQ to INR1.5b (vs. INR6.6b QoQ), driven by seasonal working capital build-up (INR5.1b change QoQ) and higher interest payments (~INR1.3b higher QoQ) likely due to AGR dues repayment.

* FY26 FCF, however, remained robust at INR21.3b (vs. INR20.3b YoY).

* Net debt (ex-leases) declined ~INR1.3b QoQ (sharp INR16.5b YoY), with leverage declining further to 0.46x (vs. 0.98x YoY).

Valuation and view

* BHL provides a pure-play exposure to BHARTI’s fast-growing wireless and HBB segments in circles with lower data and HBB penetration.

* Further, there are lower capital misallocation concerns with BHL (vs. BHARTI), which, along with a better return ratio, drives BHL to trade at an implied premium (~17% on our estimates) to BHARTI’s India business, in our view.

* Our FY27E EBITDA and EPS are broadly unchanged, while we raise our FY28E estimates by 5% each, driven by acceleration in Home broadband subscriber additions. We model a ~14%/19% CAGR in BHL’s overall revenue/EBITDA over FY26-28E, driven by ~15% tariff hike in 2QFY27, ramp-up of FWA offerings, and continued market share gains.

* We ascribe a DCF-based FY28E EV/EBITDA of 13x to BHL (which is at ~10% premium to our multiple for Bharti’s India wireless business). We reiterate our Buy rating on BHL, with a revised TP of INR1,860 (earlier INR1,910). The LT riskreward remains favorable (bull case: INR2,325; bear case: INR1,420)

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)