Buy DLF Ltd for the Target Rs.775 by Motilal Oswal Financial Services Ltd

Rental portfolio scaling up well Pre-sales expected to remain rangebound

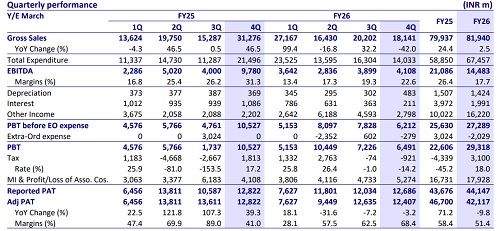

DLF Ltd’s (DLFU) 4QFY26 bookings grew 95% YoY to INR39.7b, whereas FY26 pre-sales declined 5% YoY to INR201.4b. During the year, it witnessed strong responses in three key projects - DLF Privana North recorded > INR110b in bookings, The Dahlias recorded INR48b, and Westpark, Mumbai recorded INR23b (almost fully sold out). It has a launch pipeline of INR200b for FY27, comprising major launches in DLF City (~INR80-90b potential), Arbour Senior Living, Westpark P-2 (0.8msf), and the Goa project, apart from continued inventory sales in The Dahlias. We expect pre-sales growth to be muted at 5% CAGR to INR222b in FY26-28E.

Strong growth in the annuity portfolio

* DCCDL’s rental income in 4QFY26 increased 17% YoY to INR14.3b, driven by steady growth across the portfolio. Overall occupancy in the operational office portfolio was at 95% (98% non-SEZ/89% - SEZ), while occupancy at retail assets stood at 97%. In FY26, DCCDL’s rental income increased 16% YoY to INR55.3b. Atrium Place JV with Hines is now fully leased, with occupancy certificates received for three towers and the final tower OC expected in 2QFY27.

* Execution at the following retail developments is progressing well - Midtown Plaza (97% leased; operational), Summit Plaza (~97% leased; opening expected by Jul-26), and Promenade Goa (~50% pre-leased; mall completion targeted by Aug-26). DLFU expects existing assets to deliver ~10-11% rental growth in FY27, excluding incremental contribution from new assets. The current operational portfolio of 49.6msf is expected to ramp up to ~76msf in the coming years, with rental income expected to reach INR100b over the medium term. We build in INR78b/INR85b rental income in FY27/28E, respectively

Strong cash generation; balance sheet remains sturdy

Residential collections declined 3% YoY to INR31.6b in 4QFY26, although they grew by 15% YoY to INR131b in FY26. Moreover, the company generated surplus cash worth INR77.5b (+25% YoY), which led to an improvement in its net cash position to INR142b in FY26. In the DCCDL portfolio, net debt increased to INR182b from INR170b in 3QFY26, with a net debt-to-GAV ratio of 0.19x. Cost of debt marginally declined to 7.1% in the quarter from 7.2% in 3QFY26.

Valuation and view

* We value DLFU at its NAV and currently do not assign a growth premium to this since the potential of its sizable landbank is already getting captured in our estimates. Further, delta to valuations would be via new project additions in MMR and/or other markets. Hence, we believe the company’s valuation at 0% NAV premium is justified. We value the commercial portfolio at 7.5% cap rate.

* We have a BUY rating with a TP of INR775

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412