Buy Hero MotoCorp Ltd for the Target Rs. 6,000 by Choice Institutional Equities

Strong performance driven by core strength and rural revival:

reported strong Q4FY26 and FY26 performance driven by broad-based growth, improved margin, healthy demand traction and disciplined execution across core segments. Tailwinds from the marriage season and upcoming pay commission development are likely to support entry-level demand, while new launches in the 125cc segment and steady ASP growth of ~3% QoQ in Q4FY26 aid mix improvement. Dealer inventory has corrected to ~5 weeks in Q4FY26, indicating a healthy retail traction; the management is expecting a gradual recovery in rural demand, which will further support volumes going forward.

Scooters and EVs gaining momentum with capacity ramp-up:

Scooter segment continues to outperform with ~48% YoY growth in Q4FY26 led by Destini and Xoom, while EV volumes scaled ~2.5x YoY in FY26 driven by VIDA portfolio. Capacity expansion remains a key focus, with Destini capacity up ~50%, Xoom capacity doubling and EV capacity ramping up, from ~15k to ~25k units per month, with further doubling planned in FY27E. This is supported by ~INR 15,000 Mn capex planned for FY27E; the management is expecting strong growth momentum in scooters and EVs to continue, driven by new launches and improved availability.

View and valuation: We marginally revise our FY27/28E EPS estimate and maintain our target price at INR 6,000. We value the company at 18x (maintained) P/E multiple (at implied PEG of 1.7x) on FY28E EPS. We upgrade the stock rating from ‘ADD’ to ‘BUY’, considering the stock price correction owing to the West Asia crises and strong visibility across entry-level motorcycles, scooters, EVs, exports and launches, enhancing medium-term earnings growth.We expect HMCL to deliver steady growth supported by motorcycles, scooters, EVs and exports, although near-term margin may remain constrained by commodity headwinds, with gradual improvement driven by cost control and operating leverage

Q4FY26: Result largely in line with estimate

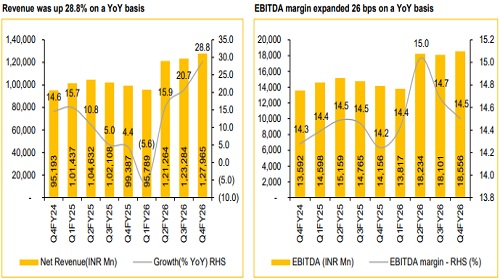

* Revenue was up 28.8% YoY and up 3.8% QoQ to INR 1,27,965 Mn (vs CIE est. at INR 1,23,310 Mn) led by 24.2% YoY growth in volume and 3.7% YoY growth in ASP

* EBITDA was up 31.1% YoY and up 2.5% QoQ to INR 18,556 Mn (vs CIE est. at INR 18,003 Mn). EBITDA margin was up 26 bps YoY and down 18 bps QoQ to 14.5% (vs CIE est. at 14.6%) * APAT was up 29.6% YoY and down 2.6% QoQ to INR 14,011 Mn (vs CIE est. at INR 14,205 Mn)

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131