Buy Aditya Birla Sun Life AMC Ltd for the Target Rs.1,230 by Motilal Oswal Financial Services Ltd

Revenue in line; 9% miss on PAT due to negative other income

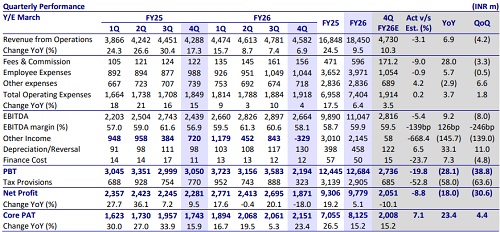

* Aditya Birla Sun Life AMC (ABSL)’s operating revenue grew 7% YoY but declined 4% QoQ to ~INR4.6b (in line). The yields on management fees for the quarter stood at 42.1bp vs. 44.9bp in 4QFY25 and 43.1bp in 3QFY26. For FY26, revenue grew 10% YoY to INR18.5b.

* Total opex grew 4% YoY to INR1.9b (in line), reflecting a cost-to-income ratio of 41.9% in 4QFY26 vs. 43.1% in 4QFY25. EBITDA grew 9% YoY but declined 8% QoQ to INR2.7b (5% miss), reflecting an EBITDA margin of 58.1% (vs. 56.9% in 4QFY25 and MOFSLe of 59.5%).

* ABSL‘s PAT came in at INR1.9b, declining 18% YoY/ 31% QoQ. The 9% PAT miss was mainly led by negative other income, while core PAT came in at INR2.2b (+23% YoY). For FY26, PAT grew 5% YoY to INR9.8b.

* Management highlighted that regulatory changes effective Apr’26 could have a gross impact of ~3-4bp on equity yields. However, this impact is expected to be largely offset through recalibration of commission structures and cost optimization initiatives, thereby limiting the net impact on profitability to a marginal ~1-2bp or lower.

* We broadly retain our FY27/FY28 earnings estimates, incorporating slower AUM growth. This slower growth is expected to weigh on revenue, partly offset by stable cost structures. We reiterate our BUY rating on the stock with a TP of INR1,230, based on 36x FY28E core P/E.

Flat sequential growth in AUM led by volatile market sentiments

* Overall MF QAAUM grew 14% YoY but was flat QoQ at INR4.4t driven by 8%/49%/15%/64% YoY growth in equity/hybrid/debt/ETF QAAUM while index QAAUM remained flat YoY.

* Overall average AUM grew 17% YoY to INR4.7t in 4QFY26, with the asset mix comprising domestic equity at 42%, debt at 36%, liquid at 14%, and alternate & offshore assets at 8%.

* Total alternate AUM at INR381b grew more than 60% YoY (INR239b in 4QFY25). PMS/AIF QAAUM, including the ESIC mandate, grew by 187% YoY to INR326b (supported by institutional mandates including ESIC), while Offshore AUM declined by 60% YoY. The company plans to launch ABSL Global Emerging Market Equity Fund Series 2.

* Passive QAAUM stood at INR411b as of Mar’26, growing 25% YoY with an ETF AUM at INR129b (up 68% YoY). The FoF AUM came in at INR60b, and the Index AUM stood at INR222b. The company has a passive product suite of 54 products and has serviced 11m folios.

* SIP contribution rose 11% YoY to INR12b for Mar’26, with SIP accounts declining to ~4.05m from ~4.2m in Mar’25. Notably, 95% of total accounts are older than five years, and 90% are older than 10 years.

* In terms of channel mix, the direct channel continued to dominate the overall asset sourcing mix with a 46% share, followed by MFDs (31%), national distributors (16%), and banks (7%). However, in equity AUM, MFDs contributed 52% to the distribution mix.

* Investor folios rose to 11m (+3% YoY), while the number of MFDs rose ~10.4k in FY26, reaching more than 93.7k+.

* Opex, as a percentage of QAAUM, stood at 17.6bp in 4QFY26 vs. 19.4bp in 4QFY25 (est. 17.4bp). Overall cost growth is likely to remain controlled despite investments in talent and alternate businesses, reflecting continued operational discipline.

* Employee costs grew 6% YoY to INR1,044m (in line). ESOP costs are likely to rise by ~INR80–100m per quarter for FY27 due to a new scheme launched in 4Q. Apart from ESOPs, incremental employee cost impact is limited, with only normal run-rate increases expected (any additional hirings would be especially in the passive/ETF business). Other expenses declined 3% YoY to INR718m (4.2% higher than estimated).

* Other income dropped to negative INR329m, led by MTM impact in 4Q.

Key takeaways from the management commentary

* The AMC has seen improvement in flows on a QoQ basis, supported by better product acceptance and increasing approvals from banking distribution channels. Key product categories driving flows include arbitrage funds (early part of the year), flexi-cap, multi-asset, multi-cap, balanced advantage, and thematic funds (Gen X), with recent traction in small and mid-cap funds.

* During the market volatility, the SIP cancellations were higher in total, but ABSL was still at a better position than the industry levels. Management emphasized strong investor education efforts to discourage SIP stoppages, reinforcing longterm investing discipline.

* On the flows side, management indicated that Apr’26 has started on a more stable footing, with volatility easing and markets showing early signs of recovery, which is helping improve investor sentiment and flows.

Valuation and view

* ABSL’s mutual fund business is witnessing strong and broad-based growth, aided by improved fund performance across equity and fixed income segments, a steady rise in SIP traction, and continued expansion of its distribution network. Strategic initiatives to strengthen market share, along with enhanced product offerings and operational efficiencies, are driving business momentum.

* The company’s focus on innovation, including the launch of a separate SIF platform and increasing focus on the growth of the non-MF segment via innovative product launches, positions it well for sustainable growth.

* We have largely retained our FY27/FY28 earnings estimates, incorporating slower AUM growth that is expected to weigh on revenues, partly offset by stable cost structures. We maintain our BUY rating with a target price of INR 1,230, based on a valuation of 36x FY28E core P/E.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412