Buy GAIL (India) Ltd For Target Rs.190 by Prabhudas Liladhar Capital Ltd

Near-term pressure; medium term recovery intact

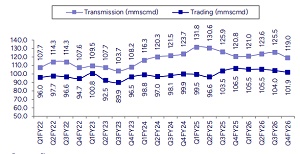

Transmission volumes declined to 119.0mmscmd in Q4FY26 from 125.5/120.8mmscmd in Q3FY26/Q4FY25 Underlying run-rate remained healthy (~129mmscmd during JanFeb’26); however, supply disruptions weighed on average Q4 volumes. Standalone reported EBITDA stood at INR11.5bn (PLe: INR20.6bn; BBGe: INR24.7bn; -56.6%/- 64.2% QoQ/YoY), primarily due to weak performance in the Trading and Transmission segments, along with continued losses in petchem business. Reported PAT stood at INR12.6bn (PLe: INR10.0bn; BBGe: INR12.5bn; -21.2%/-38.4% QoQ/YoY), impacted by higher interest expense. Lower depreciation partially supported earnings following an increase in the useful life of certain gas, LPG and petchem pipelines. GAIL expects transmission volumes of 115mmscmd under a prolonged West Asia disruption scenario and 119mmscmd assuming normalization by mid-July. In Trading, GAIL expects PBT of INR40bn under a prolonged disruption scenario, improving to INR45bn if normalization occurs by mid-Q2FY27. We build in Transmission volumes of 115mmscmd and estimate Trading PBT of INR31bn in FY27. We maintain our BUY rating, supported by mediumterm volume recovery and a favourable gas demand outlook. Stock is currently trading at 14.5x/10.7x EPS. We value the stock at 11.0x FY28E EPS and add INR40/share for investments at a 25% holding company discount, arriving at a TP of INR190/share (earlier: INR170/share)

Transmission volume declined QoQ:

Transmission volume declined -5.1% QoQ/-1.5%YoY to 119.0mmscmd vs 125.5/120.8mmscmd in Q3FY26/Q4FY25). Sequential impact was largely due to supply disruption, where transmission volumes were impacted by 30mmscmd in Mar’26 vs Feb’26. FY26 volumes stood at 122.3mmscmd (guidance 124- 125mmscmd), vs 127.3mmscmd in FY25. Underlying run-rate remained healthy (Jan-Feb: ~129mmscmd) However, March volumes fell sharply to 99.7mmscmd due to supply disruptions, dragging Q4 average volumes to 119mmscmd. Excluding crisis-related impacts, transmission volumes were tracking at ~124–125mmscmd, near the guidance.

Gas Trading under pressure:

Trading volume declined -2.0%/-4.4% QoQ/YoY to 101.9mmscmd due to West Asia disruption. Trading EBIT declined to a loss of INR1.5bn vs INR8.5bn in Q3FY26 and INR12.0bn in Q4FY25. Earnings were impacted by Rs6.8bn provision towards dues receivable from NFCL and ~Rs6.0bn adverse foreign exchange impact.

Q4FY26 EBITDA under pressure, but Adj. PAT up QoQ –

Reported EBITDA and PAT declined 56.6% and 21.2% QoQ to INR11.5bn and INR12.6bn respectively. Adj. EBITDA and Adj. PAT stood at INR18.2bn and INR18.0bn respectively, down 31.2% and up 12.5% respectively

GAIL Gas Ltd:

GGL added 191k new PNG connections and 88 CNG stations in FY26.Total PNG connections reached 1.3mn with 745 CNG stations operational. FY26 revenue rose to Rs126.8bn (vs Rs122.3bn in FY25); however PBT/PAT declined 3%/2% YoY to Rs6.0bn/Rs4.4bn. Q4 PBT/PAT increased 11%/10% QoQ to Rs1.6bn/Rs1.2bn. Targeting addition of 275 CNG stations and 400k PNG connections over next two years.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271