Buy GAIL Ltd for the Target Rs 184 by Motilal Oswal Financial Services Ltd

Weak marketing performance drags 4Q EBITDA

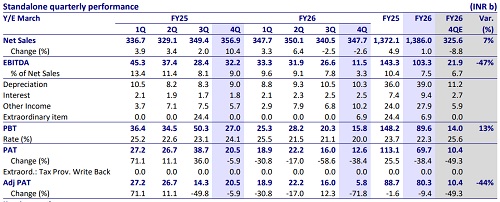

In 4QFY26, GAIL’s standalone EBITDA declined 47% below our estimate to INR11.5b, primarily due to weak performance in the marketing segment. Reported EBIT was broadly in line with estimates, with gas transmission/LPG transmission EBIT beating our estimates by 48%/28%, respectively. However, the marketing segment reported an operating loss of INR1.5b (vs est. EBIT of INR4.4b), impacted by an INR6.7b receivable provision that was not considered as exceptional. The transmission and petchem segment’s performance was aided by an INR6.9b depreciation reversal (considered exceptional). Reported PAT came in 21% above our estimate at INR12.6b, driven by significantly higher other income, while adjusted PAT stood 44% below our estimate at INR5.8b.

* Things we liked about the result:

1) Natural gas transmission/marketing volumes were strong at 119/102mmscmd in 4QFY26, beating our estimates by 8%/20%, while GAIL clocked ~129mmscmd gas transmission volumes during Jan-Feb’26.

2) Management guided FY27 gas transmission volumes of ~115mmscmd if the West Asia crisis persists through the year, with potential upside to ~119mmscmd if the situation normalizes by mid-Jul’26.

3) GAIL Gas reported PAT of INR4.4b in FY26. The company added 88 CNG stations during the year and plans to add 275 more over the next two years (including JVs).

4) The allocation of ~0.8mmscmd natural gas to the LHC segment from 3rd Apr’26 is expected to improve utilization and profitability, subject to the continuity of gas allocation.

* Key investor concerns:

1) The petchem segment remained weak, reporting an EBITDA loss of INR3.9b amid weak realizations and elevated gas costs. We expect 1HFY27 performance to remain weak, given the elevated feedstock costs and feedstock supply-side uncertainties.

2) The marketing segment reported an EBIT loss of INR1.5b in 4QFY26 due to INR6b vesselrelated forex liabilities and INR6.7b receivable provisions. Management expects FY27 marketing EBIT of INR40b+ under the current disruption scenario, with an upside to INR45b+ if geopolitical tensions ease by midJul’26.

Valuation and view

* We reiterate our BUY rating on GAIL with our SoTP-based TP of INR184. Over FY26-28, we estimate a 27% CAGR in PAT, driven by:

* An increase in natural gas transmission volumes to 132mmscmd in FY28 from 122mmscmd in FY26

* Healthy profitability in the trading segment, with guided PBT of at least INR40b in FY26/FY27.

* We expect RoE to stabilize at ~12.7% in FY28, with a healthy FCF generation of INR90b over FY27-28, which we believe can support its valuations

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412