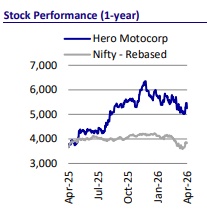

Buy Hero Motocorp Ltd for the Target Rs. 6,205 by Motilal Oswal Financial Services Ltd

Sharp rise in input costs remains a key concern

* We interacted with the management of Hero MotoCorp (HMCL) to discuss demand trends in the domestic 2W market and the outlook ahead amid ongoing geopolitical headwinds. Some positive triggers driving the company’s outperformance include: 1) a strong pick-up in Splendor sales post GST; 2) a revival in the 125cc motorcycle market share over the last few months, aided by the launches of Glamor and the new Xtreme125R; 3) a healthy ramp-up in scooters across both ICE and EV segments; and 4) a strong pick-up in exports. While these tailwinds remain supportive, input costs have started rising sharply in the recent past, and the company is likely to see some near-term margin pressure, despite the two price hikes taken in Q4.

* We expect HMCL to deliver a volume CAGR of ~7% over FY25-28, driven by rural recovery and a ramp-up in scooters and exports. This, in turn, is likely to drive 11% CAGR in revenue/EBITDA/PAT over FY25-28. We reiterate our BUY rating with a TP of INR6,205 (based on 18x FY28E EPS + INR91/419 for Hero FinCorp/Ather after a 20% Holdco discount).

Demand remains healthy in 4Q with a positive outlook ahead

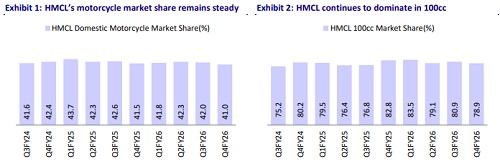

Demand has held up well in 4Q across 2W segments. Notably, retail demand in March for HMCL outpaced production, leading to a reduction in dealer stock levels by the end of the month. Splendor, which has not seen any material price reduction before, witnessed a marked pick-up in demand following GST rate cuts. Further, HMCL has recovered some lost share in the 125cc segment post the launch of the new Glamor and Xtreme 125R (with dual-channel ABS). The company’s upgraded scooters (both ICEs and EVs) have been well accepted, enabling it to gain market share in this segment. Given the seasonally strong nature of 1Q for 2Ws and the momentum from recent launches, we expect growth to sustain in the near term.

Macro headwinds to hurt margins in the near term

HMCL is effectively managing gas availability challenges and supporting its supply chain, resulting in no production disruption so far. However, the company is witnessing increasing pressure from rising input costs, with most key raw materials seeing sharp price increases over the past few months. To offset this, HMCL has already implemented two price hikes in 4Q and may require additional hikes going forward. Thus, margins are likely to remain under pressure in the near term until the full impact of input cost inflation is mitigated.

Valuation and view

We expect HMCL to deliver a volume CAGR of ~7% over FY25-28, driven by rural recovery and a ramp-up in scooters and exports. This is likely to drive an 11% CAGR in revenue/EBITDA/PAT over FY25-28E. We reiterate our BUY rating with a TP of INR6,205 (based on 18x FY28E EPS + INR91/419 for Hero FinCorp/Ather after a 20% Holdco discount).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041