Buy LTM Ltd for the Target Rs. 5,400 by Motilal Oswal Financial Services Ltd

In a better spot

Growth better placed vs. peers; BFSI recovery key

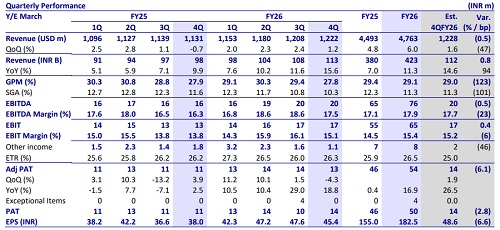

* LTM reported revenue of USD1.2b in 4QFY26, up 1.2% QoQ in constant currency (CC) vs. our estimate of 1.5% QoQ CC growth. EBIT margin at 15.1% was in line with our estimate of 15.2%. Adj. PAT came in at INR13.4b, down 4.3% QoQ/up 18.8% YoY below our estimate of INR14b.

* In INR terms, revenue/EBIT/adj. PAT grew 11.3%/18.2%/16.9% YoY in FY26. In 1QFY27, we expect revenue/EBIT/adj. PAT to grow 17.2%/27.9%/20% YoY. Free cash flow stood at 78% of net profit in FY26. FY26 RoE came in at 21.3% (vs. 23.3%/24.4%/26.1% in FY25/FY24/FY23). We maintain BUY with a TP of INR5,400 (valuing at 23x FY28E EPS), implying ~19% upside.

Our view: Front-ended productivity hits place it better vs. peers

* Good quarter, but elusive on growth acceleration: 4Q was healthy with revenue of USD1.22b (+1.2% QoQ, +8.1% YoY) and FY26 revenue growth was ~6% YoY. LTM reported strong deal wins with TCV of USD1.7b in 4Q and USD6.6b in FY26 (+10% YoY), along with a robust pipeline. The impact of AI-led productivity has been largely front-loaded in key top accounts, which should reduce near-term disruption.

* Overall, LTM appears better placed vs. peers on execution and pipeline visibility, though we still model a measured revenue growth trajectory of ~7-8% over FY27-28. We believe this is a better outcome vs peers; however, we remain watchful in the next couple of quarters as a slower-thanexpected recovery in the top BFS account poses risks to these estimates.

* Top BFSI account recovery to take longer after reset in 4Q: The top BFSI account saw a steeper decline in 4Q (-4.9% QoQ) due to a deliberate productivity reset. While management indicated that it was likely the bottom, the recovery would be gradual and slower than the pace of decline. This implies a continued drag from the top account in the near term, even as the rest of BFSI segment remains healthy and growing.

* Hi-Tech back on growth: The Technology, Media & Comms vertical saw a stronger-than-expected recovery in 4Q, driven by a faster ramp-up of certain cloud and transformation programs (especially in top accounts). While management cautioned against extrapolating the strong uptick, near-term momentum appears to have improved after a weak phase.

* Margins – focus on balanced growth, gradual expansion: FY26 margins improved ~90bp YoY (15.4%), supported by cost programs. 4Q saw a ~100bp QoQ dip due to wage hikes and productivity commitments. We believe margin expansion could be restricted to 50bp in the next couple of years as pricing pressure and competitive intensity dominate, but productivity passthroughs for major accounts are behind and there are potential upsides.

* Ambition to double revenue in five years – high growth aspiration, but execution risk remains: Management aims to double revenue over the next five years, implying a ~15% CAGR, likely supported by a mix of organic growth and inorganic contributions. While this signals a clear intent to operate at a structurally higher growth plane vs. large-cap peers, we remain wary given the steep ramp-up required from current growth levels and the dependence on successful AI monetization and M&A execution. The ambition is notable, but the path to delivery remains less defined at this stage.

Valuation and changes to our estimates

* We believe LTM’s estimated EPS CAGR of 14% for the next two years remains meaningfully better than that of large-caps; productivity pain for key accounts is behind, and this could be positive vs. peers in the next couple of years. While growth acceleration remains measured at ~7-8% over FY27-FY28 and the recovery in the top BFSI account recovery is likely to be gradual, strong deal wins and a robust pipeline provide visibility. We cut our estimates by 2-3% for FY27/FY28. We value the company at 23x FY28E EPS, implying a TP of INR5,400 and ~19% upside. Reiterate BUY.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)