Accumulate Union Bank of India Ltd For Target Rs.190 by Prabhudas Liladhar Capital Ltd

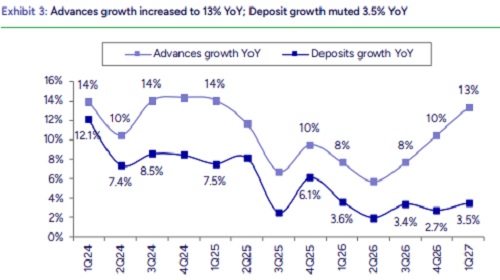

Deposit growth a key monitorable

UNBK saw a decent quarter as core PPoP was a 4.6% beat driven by higher NII due to better reported NIM that increased by 16bps QoQ to 2.8%. Utilization of surplus cash and increase in LDR by 300bps QoQ led to better NIM. As deposit growth resumes and liquidity normalizes, NIM may moderate which we have factored. While loan growth for FY27 was guided at 1% above industry, we estimate loan CAGR of 10.5% over FY26- 28E as we are watchful of deposit growth that has been muted (3.5% YoY in Q1’27). One-time ECL hit would be INR 60bn; sustainable impact is being evaluated. We keep multiple at 1.0x on Mar’28 ABV; cut TP to INR 190 from INR 200. Retain ‘ACCUMULATE’

Decent quarter; higher core PAT due to better NII/NIM:

NII was a beat at INR 100.4bn (PLe INR 95.3bn) due to better NIM (calc.) which was 2.79% (PLe 2.62%); reported NIM was up 16bps QoQ to 2.80 %. Loan and deposit growth were broadly in-line at 13.3%/3.5% YoY. CASA ratio was stable at 35.1%. Other inc. was lower at INR 46bn (PLe INR 48.2bn) due to lower TWO recovery; fee was 4% higher. Opex at INR 66.4bn largely in-line with higher staff cost offset by lower other opex. Core PPoP at INR 70bn was 4.6% above PLe. Asset quality was steady; GNPA was a tad lower at 2.65% (Ple 2.7%) due to higher write-offs. Slippage was INR 21.6bn (PLe INR 22.1bn); recoveries were lower at INR 11.9bn (PLe INR 15.5bn). Provisions were lesser at INR 9.8bn (PLe Rs11.6bn). Core PAT was ~10% above PLe at INR 45.7bn.

Loan growth was mainly led by SME/corporate:

Loan growth was healthy at 1.8% QoQ led by SME (+3.9%) and corporate (+1.7%); retail grew by +1.4%. Agri was flat QoQ due to gold loan transition. ECLGS disbursal was INR100bn to eligible pool of INR 150bn. Loan growth for FY27 was guided at 1% above industry; deposit growth is expected to trail loans by ~200bps. Bank suggested that there is no significant headroom on LDR (83.6% in Q1’27). We are conservatively factoring loan/deposit CAGR of 10.5%/8.6% over FY26-28E. The bank has mobilized USD 105mn of FCNR deposits so far and it expects to raise USD 1.5-2bn totally.

NIM improved QoQ; ECL impact under evaluation:

Reported NIM improved by 16bps QoQ due to utilisation of surplus liquidity; bank expects further improvement in NIM; we increase NIM for FY27/28E by 5bps to ~2.6%. Management estimates a one-time incremental ECL impact of ~INR 60bn while it is still evaluating the impact of sustained increase in provisions.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271