Hold Mangalore Refinery & Petrochemicals Ltd For Target Rs.150 by Prabhudas Liladhar Capital Ltd

Higher crude costs, SAED weigh on margins

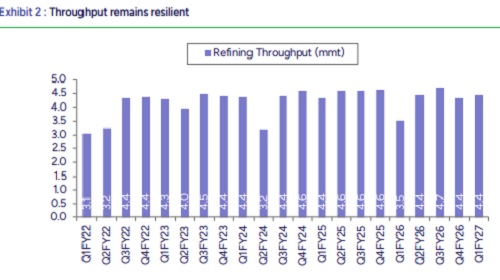

MRPL's Q1FY27 EBITDA missed street estimates, primarily due to higher cost of sales driven by elevated crude prices following the West Asia conflict. EBITDA stood at INR13.2bn (PLe: INR10.9bn; BBGe: INR15.2bn) vs INR17.8bn in Q4FY26. Adj. PAT (ex exceptional income from prior-period product price revisions) improved to INR5.6bn (PLe: INR3.6bn; BBGe: INR6.9bn) from INR1.2bn in Q4FY26 and a loss of INR2.7bn in Q1FY26, supported by the lower effective tax rate following the transition to the new tax regime. Throughput increased 1.8% QoQ/25.9% YoY to 4.4mmt, while implied GRM stood at USD8.3/bbl in Q1FY27 vs the reported GRM of USD11.2/bbl in Q4FY26, reflecting the impact of the Special Additional Excise Duty (SAED). Going forward, we estimate GRMs of USD7.8/7.4/bbl and throughput of 17.7/18.0mmt for FY27E/FY28E, respectively. We maintain our 'Hold' rating with a revised target price of INR150 (earlier INR142), based on 6.0x FY28E EV/EBITDA, as near-term earnings remain exposed to SAED. We continue to assign an option value of INR23/share to the chemicals project, which remains a few years away from commercialization.

Throughput improved QoQ: Throughput increased 1.8% QoQ and 25.9% YoY to 4.4mmt. The increase was driven by higher refining runs as refiners sought to capitalize on elevated crack spreads amid the West Asia conflict. However, GRM realizations were partly capped by the implementation of the Special Additional Excise Duty (SAED), aimed at ensuring adequate domestic fuel supplies.

Implied GRM reflects SAED impact: In the absence of a reported GRM, we estimate the implied GRM at ~USD8.3/bbl for Q1FY27. This compares with the reported GRM of USD11.2/bbl in Q4FY26, suggesting the impact of SAED imposed by the Government of India amid elevated global crack spreads. Reported GRM in Q1FY26 stood at USD3.9/bbl.

EBITDA declined QoQ: EBITDA declined to INR13.2bn in Q1FY27 from INR17.8bn in Q4FY26, primarily due to higher cost of sales. Implied crude procurement costs increased to USD116.1/bbl from USD70.4/bbl in Q4FY26 and USD74.2/bbl in Q1FY26, reflecting elevated crude prices amid the West Asia conflict.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271