Neutral Havells India Ltd for the Target Rs.1,340 by Motilal Oswal Financial Services Ltd

Strong C&W momentum; ECD and Lloyd remain subdued

Recovery expected with the pick-up in summer demand

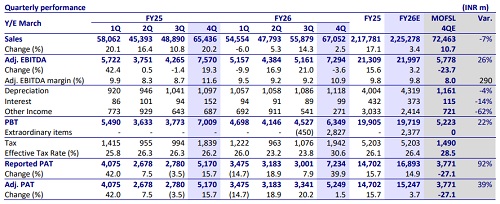

* Havells India’s (HAVL) 4QFY26 earnings were above our estimate due to higher margins in the cable & wire (C&W) and lighting segments. Consol. EBITDA declined ~4% YoY to INR7.3b (+26% vs. our estimate). OPM dipped 70bp YoY to 10.9% (+2.9pp vs. our estimate). PAT (adjusted for INR2.5b recognized under other income for gains recognized in Goldi Solar and INR297.8m under the group’s share of profit from investments) rose ~2% YoY to INR5.3b (+39% vs. our estimate).

* Management indicated that inventory gains along with year-end adjustments supported strong margin recovery in the C&W and Lighting segments. Momentum in industrial and infrastructure-linked segments remain strong, while consumer-facing categories remained relatively subdued due to persistent cost pressures. Demand for colling products have recently picked up, and remains optimistic towards revival of summer demand. However it refriend from giving any growth guidance due to evolving macro conditions. Focus would remain on improving efficiency, brand building, innovation and distribution expansion.

* We retain our EPS estimates for FY27/FY28. HAVL trades at 50x/40x FY27E/ FY28E EPS. We reiterate our Neutral rating with a TP of INR1,340 (based on 40x FY28E EPS).

C&W margin up 2.3pp YoY to ~14%, ECD margin down 2.2pp to 10.9%

* HAVL’s consolidated revenue/EBITDA/PAT stood at INR67.1b/INR7.3b/INR5.2b (+2%/-4%/+2% YoY and -7%/+26%/+39% vs. our estimate). Gross margin stood at ~31% (-70bp YoY). OPM declined 70bp YoY to 10.9%. OPM (ex-Lloyd) stood at 14.3% (up 36bp YoY; 2.2pp above our estimate). Ad spending stood at 2.6% of revenue vs. 2.2%/2.8% in 4QFY25/3QFY26.

* Segmental highlights: 1) HAVL’s revenue (excl. Lloyd) increased ~12% YoY to INR51.8b. C&W’s revenue grew ~14% YoY to INR24.7b, and EBIT margin increased 2.3pp YoY to ~14%. The Switchgear revenue grew ~6% YoY to INR7.4b, while EBIT margin declined 2.5pp YoY to ~23%. The Lighting revenue increased ~2% YoY to INR4.5b, while the EBIT margin increased 4.9pp YoY to ~21%. The ECD revenue declined ~2% YoY to INR9.8b, and EBIT margin declined 2.2pp YoY to ~10%. 2) Lloyd’s revenue declined ~19% YoY to INR15.2b. Operating loss was INR272m vs. an EBIT of INR1.1b in 4QFY25.

* For FY26, its revenue/EBITDA/PAT stood at INR225.3b/INR22.0b/ INR15.2b (+3%/+3%/+4% YoY). OPM remained flat YoY at 9.8%. OCF stood at INR15.7b v/s INR15.2b, while capex stood at INR14.2b v/s INR7.5b in FY25. FCF stood at INR1.6b v/s INR7.7b in FY25.

Key highlights from the management commentary

* Demand for the industrial segment was very strong, which offset the decline in domestic wires. Overall volume growth was ~6% YoY. It has been operating at a high capacity utilization in the cable segment.

* Within cooling products, the price increase initially happened due to BEE rating changes. Demand was subdued in the first half of Apr’26, and hence, inventory was higher. However, there has been an improvement in summer intensity in most of the regions, which has led to a pick-up in demand.

* Most of the growth in the ‘other’ segment has been driven by the solar business. The company is expanding its capacities in both the solar sector and industrial cables. There are ample opportunities for growth in this segment, and it is actively broadening its product portfolio.

Valuation and view

* HAVL's 4QFY26 performance was above our estimates, primarily due to betterthan-estimated performance in C&W and lighting segments. In contrast, Lloyd and ECD remained weak. Cooling products have seen demand pick up in the past few days due to rising summer intensity, but this will be closely monitored. Further, higher competitive intensity and inflated prices could affect demand.

* We expect HAVL to report a revenue/EBITDA/PAT CAGR of ~14%/19%/18% over FY26-28E. We estimate a CAGR of ~15-20% in C&W/ECD/Lloyd (each) and ~10% in others (mainly driven by the solar business) and ~6-8% in switchgear and lighting segments. We estimate its OPM to expand to 10.6% in FY28 from 9.8% in FY26. The company’s RoIC is expected to improve to ~24% by FY28 from ~20% in FY26. Its RoE is likely to be ~18% in FY28 vs. ~16% in FY26E.

* HAVL trades fairly at 50x/40x FY27E/FY28E EPS. We reiterate our Neutral rating with a TP of INR1,340, based on 40x FY28E EPS. Quarterly performance (INR m) Y/E March FY25 FY26

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412