Neutral Union Bank of India Ltd for the Target Rs. 180 by Motilal Oswal Financial Services Ltd

NIMslower vs estimates; earnings beat led by recoveries

Creates one-off standard asset provisions of INR7b

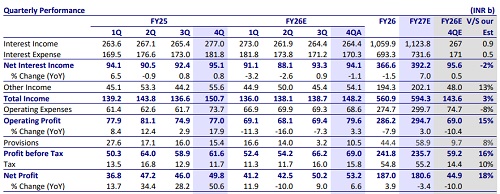

* Union Bank of India (UNBK) reported 4QFY26 PAT of INR53.2b (up 7% YoY/up 6% QoQ, 18% beat), led by NPA recoveries and lower opex. This was partly offset by lower NII and higher-than-expected provisions.

* NII declined 1.1% YoY/rose 0.8% QoQ to INR94.1b (2% miss) amid lower NIMs (down 12bp QoQ to 2.64% vs. MOFSLe of 2.72%). NIM contraction was majorly attributed to the transmission of the repo rate cut.

* Loan book grew 10.5% YoY/6.3% QoQ to INR10.5t. Management expects growth to sustain at 13-14%, while CD ratio shall remain comfortable at ~82-83%.

* Fresh slippages rose 13% QoQ to INR21b vs INR18.5b in 3QFY26. GNPA/NNPA ratio improved 24bp/3bp QoQ to 2.82%/0.48%. PCR stood stable QoQ at 83.3%.

* We fine-tune our estimates and project FY27E RoA/RoE at 1.1%/13.9%. We expect loans to expand at a 10.5% CAGR over FY26-28. We reiterate our Neutral rating on the stock with a TP of INR180 (1.0x Sep’27E ABV).

LCR declines to 114%; CD ratio stable at 80.6%

* UNBK reported 4QFY26 PAT of INR53.2b (6% QoQ, 18% beat). NII declined 1.1% YoY/rose 0.8% QoQ, while NIMs contracted 12bp QoQ to 2.64% (MOFSLe of 2.72%).

* Other income grew 19% QoQ (down 2.6% YoY) to INR54.1b amid strong recoveries from NPAs and modest treasury profits in 4Q. The bank’s AFS reserve declined INR8b (with outstanding AFS reserve at -INR10b).

* Opex declined 7% YoY/down 0.9% QoQ (8% lower than MOFSLe), largely due to changes in the discounting rate vs last year. C/I ratio, thus, declined to 46.3% (vs 49.9% in 3Q). PPoP improved 3.3% YoY (up 14.6% QoQ) to INR79.5b (15% beat on MOFSLe).

* Advances growth stood strong after a lackluster 1H growth (up 10.5% YoY/6.3% QoQ), led by strong growth in corporate (up 9.3% QoQ) and steady growth in the RAM segment (up 12.6% YoY/ 3.7% QoQ). Within retail, growth was led by VF (up 7.9% QoQ) as well as steady growth in housing (up 2.9% QoQ).

* Deposits grew 2.7% YoY/6.9% QoQ to INR13.1t amid a sharp increase in CA deposits. The CA book grew 24.1% QoQ (down 2.7% YoY), and the SA book grew 10.6% YoY/8.2% QoQ, leading the CASA ratio to improve to 35.2% (up 125bp QoQ). CD ratio declined marginally to 80.6% (down 43bp QoQ).

* Fresh slippages increased 13% QoQ to INR21b, while healthy recoveries and upgrades led to an improvement in the GNPA/NNPA ratio by 24bp/3bp QoQ to 2.82%/0.48%. PCR ratio stood stable at 83.3%.

* The bank reported higher credit costs at 0.16% vs 0.09% in 3QFY26 amid the creation of standard asset provisions of INR7b in 4Q.

Highlights from the management commentary

* The bank aims to defend NIMs despite some yield volatility in 4Q, while NIM contraction was primarily driven by a 25bp rate cut.

* AFS reserve declined ~INR8b, with an outstanding balance of negative INR10b.

* Recovery pool remains strong at ~INR450-460b; recovery momentum is expected to continue in FY27, similar to FY26.

* Growth strategy remains focused on balancing profitability and improving RoA.

* Loan book mix: ~54% linked to EBLR and ~36% to MCLR.

Valuation and view

UNBK reported a modest quarter, with NIM contraction weighing on performance; however, stronger other income supported an earnings beat, even as credit costs were elevated due to the creation of standard asset provisions. Loan growth improved following a subdued 1H, while deposit growth also rebounded in a seasonally strong quarter, with the bank remaining cautious on bulk deposits. Management has guided for loan growth of 12–14%, with a continued focus on margin-accretive expansion. Margins came in below expectations, largely impacted by repo rate transmission following the Dec’25 rate cut. The bank has built a standard asset provision buffer of ~INR30b (including ~INR7b created in 4Q), while the estimated ECL transition impact stands at ~INR42–43b. Asset quality continued to improve overall, although slippages were marginally higher in 4Q. We fine-tune our estimates and project FY27E RoA/RoE at 1.1%/13.9%. We expect loans to expand at a 10.5% CAGR over FY26-28. We reiterate our Neutral rating on the stock with a TP of INR180 (1.0x Sep’27E ABV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412