Buy Maruti Suzuki Ltd for the Target Rs.17,406 by Motilal Oswal Financial Services Ltd

Market share revival key to drive a re-rating

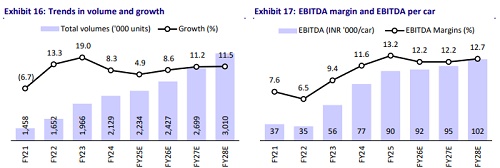

MSIL’s recent underperformance relative to the Auto index is likely to be driven by 1) near-term underperformance in wholesale and 2) disappointing 3Q performance. However, we believe these concerns seem to be overdone, given that retail demand for MSIL remains healthy, both in cars and UVs, and the same is reflected in its outperformance in retail sales post-GST cut. Further, its near term wholesale has been capped by capacity constraints, which is likely to be addressed from Apr’26 onwards as its new capacity comes on stream. We expect MSIL to outperform industry growth in FY27, aided by its healthy launch pipeline, which includes: 1) a new Brezza variant, 2) the recently launched Victoris and e-Vitara, and 3) at least one more new launch in FY27E. Further, its export momentum is likely to remain healthy as it works towards its medium-term target of 750,000–800,000 vehicles by FY31 – it has already surpassed its FY26 target in Feb26. Further, we expect the increase in input cost pressure to be offset by reducing discounts, improving mix, and normalizing pricing in cars. Overall, we factor in MSIL to post 16% earnings CAGR over FY25-28E. We reiterate our BUY rating on MSIL with a TP of INR17,406, valued at 26x Dec’27E EPS

Healthy launch pipeline and revival in cars to help revive market share

Car demand has picked up post the GST rate cut, and MSIL is emerging as a key beneficiary of the same. However, while the demand is strong, MSIL is constrained for capacity in the near term, which is likely to get addressed from Apr’26 onwards. Post that, we expect MSIL to outperform industry growth backed by its healthy launch pipeline, which includes: 1) benefits from the recently launched Victoris and e-Vitara, 2) the soon-to-be-launched Brezza upgrade, and 3) at least one more new launch in FY27E.

Exports to remain a key growth driver

Suzuki Japan is shifting more and more of its export market production from Japan to India. Further, the alliance between Toyota and Suzuki offers longterm growth opportunities, as Toyota’s global markets are now accessible to Maruti. Suzuki has made India its global production hub for the e-Vitara and the Victoris. Led by a strong demand momentum across multiple markets, MSIL has already surpassed its export target for FY26 of 400k units in Feb’26. It continues to work towards its medium-term target to export 750,000–800,000 vehicles by FY31. Given the tailwinds highlighted above, we expect MSIL to post 25% volume CAGR in exports over FY25-28E.

Market share recovery key to stock re-rating

MSIL has underperformed the Auto Index post GST rate cuts largely on concerns of a weaker than expected performance in 3Q. We believe these concerns are overstated, as we expect MSIL to outperform the industry in FY27 and beyond once its near-term capacity constraints are resolved, supported by its robust product launch pipeline. Overall, we factor in MSIL to post 16% earnings CAGR over FY25-28E, largely back-ended. We reiterate our BUY rating on MSIL with a TP of INR17,406, valued at 26x Dec’27E EPS.

Healthy new launch pipeline to help outperform from hereon

* Post the launch of the new Victoris in Sep25 and aided by GST rate cuts, MSIL has bounced back reasonably well. When we compare retail sales over AprAug’25, MSIL grew broadly in line with the industry. However, during SepFeb’26, while MSIL retails have grown 16.3% YoY, industry retails are up 15.1% YoY. This has led to a 170bp market share recovery over this period to 40.9%.

* However, its performance could have been better if not for the capacity constraints it currently faces as it is currently producing at peak capacity. With the capacity constraint issue to be addressed soon, we do expect MSIL’s UV segment to outperform the industry on the back of its healthy launch pipeline. We elaborate below on some of the recent and upcoming new launches.

Healthy demand for the new Victoris

* The Victoris was strategically launched through the Arena network which has almost 3,000+ touchpoints and has helped MSIL tap into Tier 2 and Tier 3 cities as well. It bridged the gap between the compact Brezza and the premium Grand Vitara, offering a "full-size" SUV experience at an aggressive entry price of INR1.05m. This entry price point is also the lowest in the segment, targeting the first-time SUV customers across urban and rural markets. The Victoris has a massive line-up of 21 variants across the price range of INR1.05m to INR1.99m.

* Further, Victoris does not compromise on the safety of the vehicle and offers a 5-star rating in both Bharat NCAP (BNCAP) and Global NCAP. The car provides 6 airbags as standard across the entire variant line-up, along with features such as ESP and hill hold, while providing features like a 360-degree camera and ADAS Level 2 in the upper trims.

* The success of the model can be gauged by the fact that it has already surpassed 50k unit sales in the first five months of its launch.

* Further, given the overlapping price points, we did expect the Victoris to cannibalize the Brezza at the lower end and the Grand Vitara at the upper end. However, Maruti has done very well by positioning this vehicle such that it leads to minimal cannibalization and drives a material increment in volumes post this launch. The GV, which was selling an average of 6.2k units per month prior to Victoris launch, has shot up to 8.6k units per month in the last few months, also aided by the GST rate cut benefit. We expect the Victoris to be a key growth driver for MSIL for FY27E.

Upcoming Brezza facelift

* We understand that MSIL is also expected to launch a Brezza facelift soon. According to media articles, the upcoming facelift is expected to be a significant overhaul rather than a simple cosmetic update. One of the most critical mechanical changes is likely to be the expected introduction of a turbo-petrol engine—either the 1.0- liter booster jet or a new 1.2-liter unit. MSIL already has a 1-liter booster jet engine in the Fronx currently. The big advantage of either of these engines in the Brezza would be the fact that it will qualify for the lower GST rate of 18% (vs. 40% rate currently, as the current model has a 1.5-liter engine). This will help position the product competitively in the market. It is important to highlight that Brezza had a relative competitive disadvantage post GST rate cuts. While the GST on competing models like Nexon and Venue reduced from 28% to 18%, the same on Brezza came down to 40% from 45%. MSIL has had to absorb this differential on this model in a bid to maintain its competitive positioning. Further, such has been Brezza’s standing in the market that, despite the relative disadvantage due to the higher duty, it is still selling almost 15k units per month in this fiscal.

* Thus, if the company were to launch a smaller engine under Brezza, which could help reduce its price point, it could materially help ramp up volumes for the model. We also understand that the 1-liter booster jet may not compromise power for the model materially (100hp vs. 103hp for the 1.5-liter engine). ? Some articles also allude to the presence of a new six-speed manual transmission, which may replace the existing five-speed unit to provide better highway cruising and fuel efficiency. There could also be a few cosmetic design changes, which will help align the Brezza with the design language seen in the recently launched Maruti Suzuki Victoris. ? Even on the interiors front, there are expectations of a dual-tone theme, a larger 10.25-inch touchscreen infotainment (up from the current nine-inch unit), ventilated front seats, and a powered driver's seat. The other key change expected is that, just like the Victoris, the new Brezza is also likely to have the underbody CNG tank layout, preserving the boot space, which had been a pain point for customers. ? While we await the exact details of this upgrade, we do expect this variant to help drive incremental volumes for MSIL going forward.

e-Vitara launched in the domestic market with Baas option for customers

The e-Vitara has been priced at INR1.59m for the Delta variant (49 khw battery) and moves up to INR1.97m for the top?end trim with the larger 61 kWh battery pack. MSIL has also launched the e-Vitara in the domestic market with a Battery?as?a? Service (BaaS) option designed to lower upfront costs and attract a broader set of EV buyers. Under the BaaS model, the e-Vitara’s base version is available at about INR 10.99?lakh (ex?showroom), with customers paying separately for battery usage at around INR3.99/km. Beyond this, MSIL has also provided a few incentives for EV adoption to customers, which include:

* A free 7.4kW AC charger, including free installation, worth Rs50k for the introductory period.

* The owner will also get a one-year of complimentary free charging across MSIL’s charging stations, available through the Maruti Suzuki 'e for me' app. The free charging facility is capped at 1,000 units or for one year, whichever comes first, at the 2,000 exclusive charging points across 1,100 cities. Both the above points would help drive away range anxiety fears for a customer.

* They have introduced an attractive buyback option, ensuring a 60% buyback amount after three years/45k kms or 50% buyback after four years/60k km. This would clearly help allay resale value fears of a customer.

* MSIL is also providing an eight year/1,60,000 km warranty on the battery pack and a three-year warranty on the vehicle. Additionally, a five-year extended warranty on the vehicle can be purchased at an additional cost.

We believe this is an excellent overall package from MSIL because it: 1) reduces the upfront cost for a customer, 2) largely takes care of charging needs, and 3) provides resale value assurance. Under MSIL’s strong distribution network and established brand connection, along with other attractive offers, this scheme is likely to resonate well with prospective EV customers. While MSIL is currently facing supply constraints, we expect the actual ramp-up for this model in the domestic market to commence from July onwards once its new facility comes on stream.

Valuation and view

Over the last six months, MSIL stock has actually declined 12% and has underperformed the Auto index by almost 9%. Part of the reason for its underperformance is likely to be driven by: 1) underperformance in wholesales over the last couple of months and 2) disappointing 3Q performance.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041