Accumulate Maruti Suzuki Ltd For Target Rs.14,550 by Prabhudas Liladhar Capital Ltd

Mixed Quarter with Strong Revenue Growth

Quick Pointers

* Dealer inventory at FY26-end was low at ~12days’ stock

* MSIL’s FY27 vol growth estimates at 10% YoY for its domestic PVs

* Capacity to reach 4mn units p.a. in the medium term

MSIL’s Q4FY26 operating revenue was above estimates, while margins faced pressure due to commodity inflation and new model expenses. MSIL projects its domestic PV volume to grow 10% YoY in FY27, above SIAM’s recent industry estimates of 5-7%, as the company tries to address order backlog by accelerating capacity expansion, along with robust exports and depreciating INR. Geopolitical risks and higher RM prices are expected to keep near-term margins under pressure, further aggravated by EV ramp-up, partially offset by better mix, price increases and operating leverage. Given recent correction in the stock, we feel it gives a good entry point to accumulate it. We estimate volume/realization CAGR of 6.2%/6.3% over FY26-28E, translating into revenue/EBITDA/PAT CAGR of 12.8%/14.2%/17.3%. We reiterate ‘Accumulate’ rating with TP of INR14,550 (previously INR15,200), valuing it at P/E of 23x FY28E EPS.

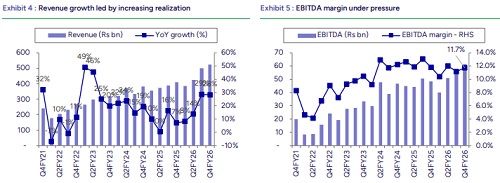

Standalone op revenue grew by 28.2% YoY to INR524.5bn: Realization was INR775.6k (+14.6% YoY/ +3.8% QoQ). Gross margin was 26.6% (-270bps YoY/-70bps QoQ), missing BBGe/PLe by -20bps/-70bps. EBITDA margin at 11.7% (-10bps YoY/+60bps QoQ) met BBGe. EBITDA was INR61.6bn (+27.1% YoY/+10.5% QoQ). Reported PAT was Rs35.9bn (-6.9% YoY/-5.4% QoQ). For FY26, op revenue was INR1,832.7bn (+19.9% YoY), EBITDA margin was 11.7% (-150bps YoY), and reported PAT stood at INR144.5bn (+1.0% YoY). It had ~49% share in PV exports from India in FY26.

EBIT margin expands 70bps QoQ to 8.8%: Favorable employee cost (100bps), discounts (50bps), forex impact (30bps) and fixed cost incidence due to inventory accretion (30bps) were partially offset by adverse RM price variations (80bps), new model expenses (60bps), and other expenses (20bps) due to some lumpiness and seasonality. PAT declined due to MTM impact of ~INR7.5bn on invested surplus from hardening of bond yields (~46bps), which reversed by ~35% couple of days ago.

Short-term pain: The management acknowledged the business environment may be impacted in the short term, but it should be temporary. MSIL is working closely with supply chain and logistics partners to mitigate potential disruptions arising from geopolitical tensions, with enhanced contingency planning in this dynamic situation where cost pressure persists. Being the market leader in PVs, it has multiple levers to record a healthy margin trajectory once these headwinds are over. GST 2.0 has brought about sustained long-term structural growth by expanding the potential customer base. Focus will be on higher utilization as demand continues to be good.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271