Add Maruti Suzuki India Ltd for Target Rs.14,600 by Choice Institutional Equities

Q4FY26 Performance Highlights: MSIL reported its highest-ever quarterly sales of 667,209 units, up 11.8% YoY, driven by strong domestic demand and record exports of 137,215 units. EBITDA margin improved, from 11.2% to 11.7% QoQ, while PAT declined 6.9% YoY to ~INR 36 Bn, impacted by INR 7.5 Bn MTM loss.

GST-led Demand Revival: The PV industry declined 0.4% in H1FY26 but rebounded sharply with 16.7% growth in H2FY26, supported by GST cuts to 18% on small cars. MSIL remains a key beneficiary, with first-time buyers rising from 42% in H1FY26 to 51% in Q4FY26, indicating structural demand recovery. The company concluded the quarter with a strong order backlog of ~190,000 units, including ~130,000 small cars, while dealer inventory stayed low at ~12 days, highlighting unmet demand due to capacity constraints.

Strong Product Momentum: Dzire maintained leadership with 12.6% domestic share, growing 38.8% YoY in FY26, while Swift and Baleno delivered a modest growth. SUV traction remained strong, with Victorius sales at 75,611 units and EV entry eVitara reaching 3,652 units in FY26

Capacity Expansion and Capex Push: MSIL is undertaking aggressive expansion, adding ~500,000 units of capacity through Kharkhoda and Gujarat plants, with the total capacity targeted at ~4 million units by FY31E. Annual capex stands at ~INR 100 Bn, supporting long-term growth

Exports Driving Growth: Exports share increased, from 15% in Q1FY25 to 20% in Q4FY26, with MSIL contributing 49% of India’s PV exports. The company targets ~0.75 million exports by FY31E, supported by global platforms, such as eVitara across ~100 markets

We expect MSIL to deliver steady growth driven by GST benefits, new launches and exports, supporting volume and revenue visibility. However, due to weaker Q4FY26 earnings, commodity pressures and geopolitical risks, we cur our EPS estimates by ~5%/6% EPS cuts for FY27/FY28E. We reduce TP to INR 14,600 ( earlier: INR 16,200) due to margin pressure, rising competition and macro uncertainty, valuing the stock at 25x FY28E P/E, while maintaining our ADD rating

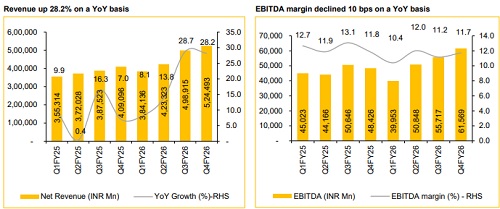

Q4FY26 Result: Top line, EBITDA better; while PAT underperformed

* Net Revenue (Incl. OOI) was up 28.2% YoY and up 5.1% QoQ to INR 5,24,493 Mn (vs CIE est. at INR 4,97,655 Mn), led by 11.8% YoY growth in volume and 15.3% YoY growth in ASP

* EBITDA was up 27.1% YoY and up 10.5% QoQ to INR 61,569 Mn (vs CIE est. at INR 57,728 Mn). EBITDA margin was down 10 bps YoY and up 57 bps QoQ to 11.7% (vs CIE est. at 11.6%)

* PAT was down 6.9% YoY and down 5.4% QoQ to INR 35,905 Mn (vs CIE est. at INR 40,795 Mn)

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131